- Subscribe

- Premium

- C-Suite

- Insiders

- M&A

- Gurus

- Spinoffs

- Buybacks

- More

Technology and innovation often drive sea change in companies and entire industries. We are currently seeing this with artificial intelligence with all its amazing opportunities and significant investments thanks to the hype cycle that inevitably follows.

In the 1950s the biggest recreational craze was bowling. The number of bowling lanes doubled to over 100,000 and the stocks of companies like AMF and Brunswick doubled between 1957 and 1958. What was the driving force behind this sudden interest in bowling?

The innovation came from the automatic pinsetter machines that eliminated the need for a pinboy to go back and forth between lanes and reset the pins. At the top of the bubble in bowling related companies, Brunswick’s stocks had gone up by 1,600%.

While we are not seeing the kind of innovation in bowling like we saw in the 1950’s, we are seeing a rise of “eatertainment” options.

When Top Gun: Maverick came out a couple of years ago, my family was excited to go check out the latest Tom Cruise blockbuster on the big screen and we picked a newly reimagined local mall to watch the movie. The movie theatre had large recliners and you could get both food and drinks delivered to your seat. We were pleasantly surprised when certain scenes utilized the two side walls as screens and you got to see the Super Hornet jets start from the left screen, enter the main screen and then exit the frame from the right screen.

This article is not about the the international luxury cinema chain Cinepolis or about the 270-degree ScreenX technology that made the viewing experience memorable but another venue situated right next to Cinepolis called Pinstripes (PNST), which follows the new mold of “eatertainment”, where dining is combined with an activity. Think Topgolf (MODG), which combines food and golf, SPIN for food and ping-pong and Dave & Buster’s (PLAY), the mall-based destination for arcade gaming and dining.

I’ve been to all three eatertainment venues and they provide a good option for an evening out with family, friends and colleagues.

Pinstripes (PNST), in a similar mold, combines bowling and bocce with bistro dining in an upscale venue that is only currently found in 16 locations across the United States.

Their only Northern California location happens to be at my local family-owned mall that decided to shut down an entire section for years in anticipation of Sears’ bankruptcy and redeveloped it with an experiential bent that included Cinepolis, Pinstripes and a tea garden restaurant among other retailers like West Elm and Apple.

I checked in with a few friends that had tried Pinstripes and the overall response was positive. Two of them were there for corporate events and the others visited the location with friends, family and colleagues.

Having recently purchased stock of the company, I wanted to go check out our local Pinstripes location for myself.

I stopped by the mall on a Tuesday evening with family for a couple of games of bowling and a bite to eat and the place was packed.

Pinstripes started its journey by opening its first location in the Illinois in 2007 and growing the company to 16 locations across 9 states, with four more under construction. The company plans to expand to more than 150 domestic locations over the next few years.

SPAC Merger:

When driving down the 101 freeway to Redwood City, I noticed Pinstripes advertise its listing on the NYSE on a digital billboard. I was aware of the company but didn’t realize it had gone public by merging with the SPAC Banyan Acquisition Corporation on December 29, 2023. The stock closed its first day of trading on January 2, 2024 at $13.31 per share before beginning its rapid decline to current levels.

Most companies that go public through a SPAC suffer a similar fate and SPAC business combinations have been fertile hunting grounds for short sellers.

I have a chapter dedicated to SPACs or “special purpose acquisition companies” in my first book The Event-Driven Edge in Investing that is scheduled to come out next month. SPACs are created by sponsors who raise a bunch of money first from investors and then go looking for an operating business to acquire and merge into the SPAC.

We were short WeWork through put options and I discussed the performance of companies that go public the SPAC route in our January 2022 mid-month update called SPAC Attack. I wrote the following about SPACs in that update:

“We track SPAC IPOs and business combinations on Inside Arbitrage here and here. A couple of weeks ago, I decided to download the list of all completed business combinations to see how they had performed after they had merged with an operating company. I suspected that given the bubble in various asset classes and a dwindling supply of high quality private business to acquire, the post-merger performance was probably not good.

I was completely surprised by the results. Performance was significantly worse than I expected.

The group of 159 post-merger SPACs I looked at collectively lost more than 36% and only 12 out of the 159 had positive returns. I was aware that my (Twitter) friend Ross Greenspan had written a paper on the history of SPACs and I reached to him to see if I could get a copy.

His paper titled Money for Nothing, Shares for Free: A Brief History of the SPAC is a fascinating read. I was not aware that both Burger King and American Apparel had gone public through SPACs. More importantly, I noticed on page 24 that the results I was seeing from analyzing Inside Arbitrage SPAC data were confirmed by another longer study that found “the average four-year buy-and-hold return for second-generation SPACs was a grim negative 51.9%”.

I am certain that if I look at the data again, the results are going to be significantly worse. Some of the reasons companies that went public by merging with a SPAC did so badly was because many of them were nothing more than pre-revenue science projects with overtly rosy projections of how the future would unfold or were very young companies not ready for prime time just yet.

Coming out of the 2000 dot com bubble, small cap stocks outperformed their large cap brethren for the better part of two decades. For the decade starting in January 2000, small cap stocks represented by the Russell 2000 outperformed the S&P 500 by more than 40%.

While returns were low single digits per year, they did better than the S&P 500’s loss decade of -24% performance. The next decade, this outperformance of small cap stocks continued for another eight and a half years before reversing. Since 2019 large cap stocks have significantly outperformed small cap stocks to the tune of over 42% as you can see from the chart below.

The reasons for this outperformance are myriad but one hypothesis is that companies like Stripe, Uber and Airbnb that would have normally gone public much earlier in their lives, decided to remain private for much longer. They had access to significant private capital in an era of very low interest rates and tremendous access to liquidity.

On the one hand you have companies that jumped the gun and decided to go public too soon through a SPAC and on the other hand there are companies like Stripe at valuations approaching $60 billion that are still private.

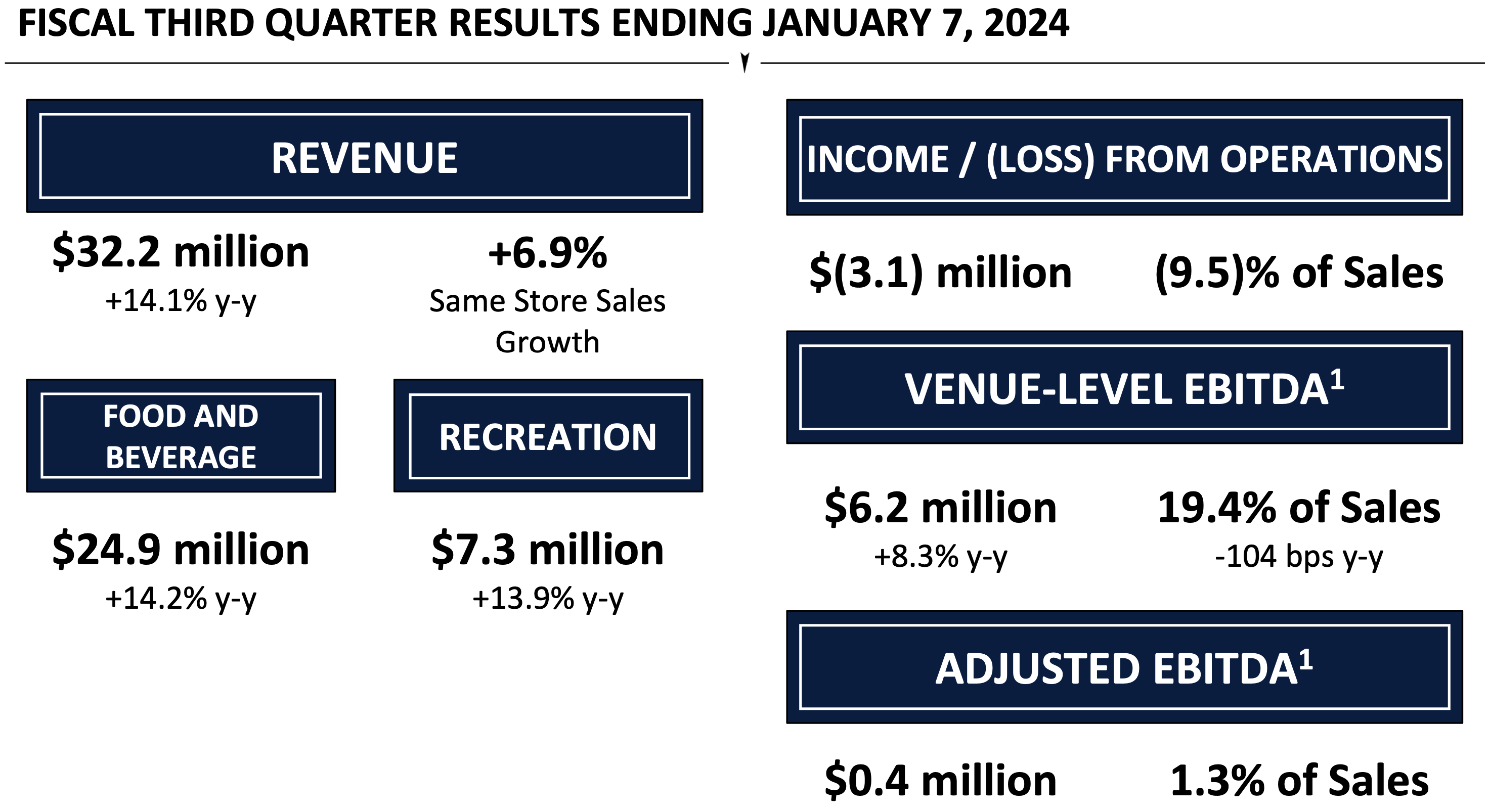

Despite its decision to go public through a SPAC, Pinstripes has a real and proven business model with same store sales growth and positive venue-level EBITDA.

Management Team:

Pinstripes was founded in 2006 by Dale Schwartz and he still helms the company as the CEO working closely with COO Chris Soukup since the company’s founding. After an early stint in Morgan Stanley’s M&A division and a few years with a leveraged buyout firm, Mr. Schwartz’s experience was mostly in the pharmaceutical industry. He has a Bachelor’s degree from Colgate University and a MBA from the Harvard Business School. Mr. Soukop’s 35 years of experience in the restaurants industry complements Mr. Schwartz’s entrepreneurial spirit.

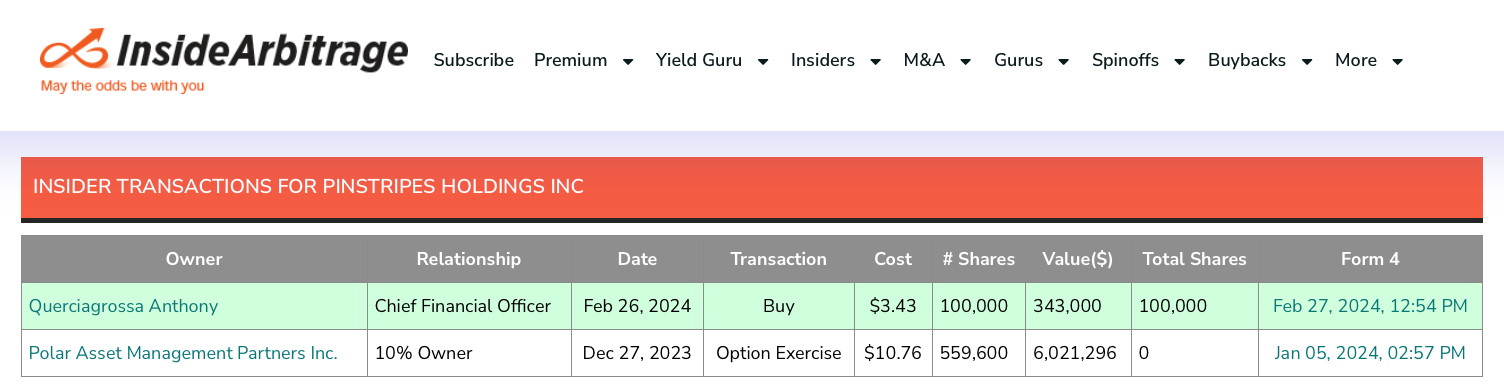

The CFO Tony Querciagrossa joined the compay in September 2023 after the SPAC business combination was announced. He started his career at GE before serving in the roles of CFO or President at various companies.

Insider Purchase:

I wasn’t drawn to Pinstripes just because I had heard from friends who went bowling there or saw their billboard ad calling out their NYSE listing. It was an insider purchase by the CFO Tony Querciagrossa in February that made me take a closer look.

Normally I tend to avoid micro-cap companies with a market cap below $300 million and all the more so, if it went public by merging with a SPAC. But the Peter Lynch kind of vibes I got from Pinstripes were hard to ignore. Invest in what you know and in companies that are ready to ride the growth curve after proving their business model at a few locations was a mantra that worked out very well for Mr. Lynch.

The fact that the venue-level economics were good and that growth was coming as much from same store sales as the addition of new locations made me take a closer look.

Comparative Analysis:

For certain companies, I tend to build a 5 or 10 year financial model with certain growth and operating assumptions and feed the results into a discounted cash flow model. I did this recently for the cloud software company Freshworks (FRSH) and decided not to invest.

Pinstripes is not one of those companies.

The road from 16 locations to over 150 locations is going to be bumpy with a lot of execution risks. We will discuss risks in the next section but to get some sense of how the company is valued on a comparative basis, I decided to see how companies like Bowlero (BOWL), Dave & Buster’s (PLAY) and Topgolf Callaway Brands (MODG).

In many ways Bowlero is the closest comparison to Pinstripes because it is a bowling alley operator that also has dining options. Bowlero went public by merging into a SPAC, saw the inevitable SPAC related crash and then rebounded from there. They were also smart enough to buy back their warrants for pennies on the dollar and I will not be surprised to see Pinstripes do the same thing. More on that later.

The comparison with Bowlero however ends there as Bowlero has 350 locations, has an enterprise value of $4.69 billion (a lot of net debt on that balance sheet) and also owns the Professional Bowlers Association (PBA).

Dave & Buster’s is a little larger than Bowlero with an enterprise value of $5.48 billion and Topgolf Callaway is larger still with an enterprise value of $6.64 billion. Topgolf Callaway is not a pure play “eatertainment” comparison because the golf club manufacturing company Callaway Golf Company acquired Topgolf for $2.5 billion in 2021 including $555 of debt on Topgolf’s balance sheet.

Callaway had initially invested in Topgolf in 2006 and had a 14% stake in the company at the time of acquisition. Topgolf only had 63 locations at the time the acquisition was announced but they tend to have massive footprints.

Topgolf’s revenue in 2019 was $1.1 billion. Even if we were to assume healthy growth of 30% in 2020, Callaway paid 1.75 times Topgolf’s revenue in 2020 for the acquisition. Interestingly enough Dave & Busters trades at 2.53 sales and Bowlero trades for 4.31 times sales. I am using trailing twelve month Enterprise Value/Sales numbers and not Price/Sales numbers because of the significant amount of net debt each of these companies carries.

Pinstripes has a market cap of $138 million and an enterprise value of $272 million including warrants related liabilities, debt and $90.23 million of operating leases.

Trailing twelve months revenue was approximately $111 million, implying the company is trading at 2.47 times sales, well below Bowlero’s valuation and in-line with Dave & Buster’s but with significant growth runway ahead of it.

I am using numbers as of March 1, 2024, which is when I wrote about Pinstripes for our March 2024 Special Situations newsletter. The stock is trading at about the same price right now and so the numbers should mostly still be the same.

Risks:

There is little doubt that this is one of the riskiest opportunities I have come across in a long time and also one with the potential to become a ten bagger. This is a tiny microcap stock that is going to be difficult to get into, difficult to get out of and likely quite volatile.

While the management team has been in place for a while and clearly the CEO and COO like to work together (reminds me of one of the keys to success discussed in the book The Outsiders by William Thorndike) they do not have the experience scaling a company from 16 locations to over 150 locations. There will be significant execution risk on that journey.

There are also financing risks and how the company chooses to raise capital in the future, especially if the stock price does not recover. Shareholders will see dilution for years to come.

When the company went public, it raised $50 million in debt from Oaktree Capital. The loan not only has a high interest rate (12.5% plus an additional 7.5%) but also grants Oaktree warrants priced at one cent if the company attempts to prepay the loan before the 2028 due date. The number of warrants granted increases based on how much Pinstripes’ stock drops in the months after it goes public. I would highly recommend checking out the conditions of this onerous loan in this 8-K filed with the SEC on December 19, 2023.

The other key risk that probably concerns the market is that consumer spending at a Pinstripes is the very definition of discretionary spending. In case of a deep recession or a spike in the unemployment rate, spending on “eatertainment” will likely be the first to get hit.

Normally the warrants (PNST.WS) expiring on 9/30/2028 that are trading for $0.35 would have been a good way to get exposure and limit risk. However as we have seen with Bowlero, it is very likely that the company might buy back the warrants at a small premium.

Conclusion:

There are a lot of things I like a lot about Pinstripes including a founder at the helm, a long runway for growth, the CFO insider purchase and double digit revenue growth.

The company offers a clear value proposition for consumers and is positioned in select upscale malls. The risks cannot be understated either and so I started a smaller than normal position in my personal portfolio.

Disclaimer: For educational purposes only. Please do your own due diligence before buying or selling any securities mentioned in this article. We do not warrant the completeness or accuracy of the content or data provided in this article.