- Subscribe

- Premium

- C-Suite

- Insiders

- M&A

- Gurus

- Spinoffs

- Buybacks

- More

Investing processes are unique to each individual and investment firm. While some rely on investment checklists (I once built one with nearly 80 data points), others might rely on calculating the potential intrinsic value using a discounted cash flow (DCF) model and yet others might focus on the qualitative aspects of the business (management, industry, macro, etc.). Some investors might choose an event-driven strategy like merger arbitrage or stock spinoffs and others might only use technical analysis. I personally use a combination of idea generation from event-driven strategies, building a DCF model when required, peer comparison and writing about the business. Writing helps crystallize my thought process and makes me dive deeper into the qualitative aspects of the business than I would have otherwise.

Once a potential investment is identified through the investment process of your choice, you have to then figure out how it fits into the portfolio.

After all this work is done in selecting an investment, it is not surprising that once you buy the company, objectivity sometimes flies out the window. We often get anchored to the price at which we bought the company. Instead of looking for dissenting opinions, we seek information that feeds our confirmation bias. When having coffee with my neighbor last week, we were talking about markets and I mentioned to him that markets do an excellent job of keeping us humble. Just when I think I have done the work and understand an investment, something goes wrong either on account of an external factor outside my control or through an error of omission on my part. The market humiliates the best of us frequently enough to keep this game interesting.

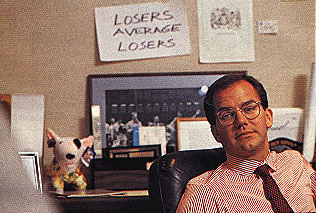

Whether it is Paul Tudor Jones putting up the sign “Losers Average Losers” on the wall behind his desk or Jesse Livermore warning us not to average down in Reminiscences of a Stock Operator by Edwin Lefèvre, this advice is hard for most investors to follow. We are conditioned to look for bargains in life and fall into the trap of, “if it was good at $30 per share, it is a screaming buy at $15”. Unfortunately a big drop in price doesn’t necessarily translate into the need to back up the truck, fill the boat or sell the farm to buy more. More often than not, it points to an error of omission in your analysis, changing industry conditions or a shift in market leadership/style (from growth to value for example).

Whether it is Paul Tudor Jones putting up the sign “Losers Average Losers” on the wall behind his desk or Jesse Livermore warning us not to average down in Reminiscences of a Stock Operator by Edwin Lefèvre, this advice is hard for most investors to follow. We are conditioned to look for bargains in life and fall into the trap of, “if it was good at $30 per share, it is a screaming buy at $15”. Unfortunately a big drop in price doesn’t necessarily translate into the need to back up the truck, fill the boat or sell the farm to buy more. More often than not, it points to an error of omission in your analysis, changing industry conditions or a shift in market leadership/style (from growth to value for example).

Value investors and company insiders often get anchored to old prices based on my observations following insider buying for more than a decade. I am often reminded of Bill Miller averaging all the way down on housing stocks during the Great Recession of 2007-2009. Warren Buffett did not make the same mistake and did not average down, even as the Irish banks he invested in lost nearly 90% of their value.

Instead of averaging down, we should consider averaging up on investments that are working. It is remarkable, how consistent good businesses and management teams are, at executing and creating value for their shareholders. If you find a good business, it does not have to be a one and done deal. Investing by averaging up through a new purchase or by reinvesting dividends through a DRIP plan can work wonders. This strategy is similar to what venture capitalists are required to do as their portfolio companies perform well and raise more money through new investment rounds. Their investment process forces them to average up and concentrate their investments. I have shifted my investment process to average up instead of averaging down over the last few years and could not be more thankful with the results.

There are always exceptions to every rule and I wrote the following when discussing the online education company Coursera (COUR) in our May 2021 Special Situations newsletter,

I think Coursera is going to have a volatile few years as it navigates macro environmental factors like the COVID-19 pandemic and chooses to expand its market share but is likely to do very well in the long run. An intermediate drop of 30% or more is not entirely unlikely and I have seen this happen to many of the growth or value stocks I own before they went on to post large gains.

I prefer not to average down on stocks, but in this case, given the volatility of the stock in recent weeks and the stretched valuation of the market as a whole, it may be prudent to build a position gradually. Buying more over time is fine as long as that decision is made a priori or in response to general market conditions and not simply because the stock has declined and now appears even more attractive than your analysis initially suggested. The latter may point to a flaw in the initial analysis or business conditions that are probably deteriorating.

Investment processes are dynamic and we are (hopefully) always learning from our mistakes. Given current market conditions, the coming months and years are likely to be challenging for equity investors and having a strong process to lean on should help outcomes.