December 2021 Mid-Month Update: Doubling Down on Magnachip

December 15, 2021

This is the third post in a new series that we publish mid-month for InsideArbitrage Premium and InsideArbitrage Plus subscribers. These posts will contain updates related to the model portfolio (if any) or a new quick idea. This month we are going to focus on a busted deal that looks attractive despite the deal failure. In our last mid-month article titled A Time For Caution, we highlighted the need to start scaling back long exposure and/or hedging parts of the portfolio. We wrote the following last month,

While attempting to time the market may be futile, it may be prudent to adjust the risk profile of the portfolio while the exits are still open and either scale back positions or add protection through put options. I have started scaling back positions in my personal portfolio and will be buying put options on an ETF that is the poster child of this bubble. I am also going to sell half our position in the flooring products company Mohawk Industries (MHK) from the model portfolio and register a gain of 102.14% on the position since we wrote about it for the May 2020 newsletter. While I still like the company, with input costs rising, supply chain issues and the housing frenzy cooling off thanks to higher interest rates, the prospects for the company have dimmed a little.

We have been positioning ourselves for a challenging market by focusing on a potential “deal in the works” (Healthcare Trust of America) in the October mid-month update, a merger arbitrage position (Magnachip Semiconductor) in the November 2021 newsletter, and a company that would benefit from volatility (Virtu Financial) in the December 2021 newsletter. Market action during the last four weeks and especially in certain sectors of the market aligns with our view.

We wrote briefly about insider buying in DocuSign (DOCU) last weekend and I decided to build a model looking out the next five years to see if the company could grow into its current valuation. The company would have to execute perfectly on the trifecta of maintaining high growth (>30% revenue growth year-over-year), bringing down operating expenses from 81% of revenue to 55% of revenue, and keeping shareholder dilution from stock-based compensation to 5% or below. In other words, you need very generous inputs in your model to begin to justify the current valuation and this is despite a greater than 40% drop in the stock price. I experienced something similar when modeling another company as described in the article Insider Weekends: Satya Nadella Sells Half His Microsoft Shares three weeks ago,

While Asana has a long runway ahead of it, I think valuations across the SaaS sector are extremely stretched. Several years ago, I had built a model for a SaaS company in my portfolio and the price has generally stayed somewhere between my base case and bull case scenarios. However in recent months, the stock has trended well above my bull case. It does not matter how I attempt to value the company, valuation looks extremely stretched. I know it is no longer fashionable to attempt to value a company on traditional metrics but when it becomes hard to value the company at a reasonable multiple even looking out a decade, something is not quite right.

In a market environment like this, lower risk merger arbitrage positions might be a good place to park some capital and generate yield. Deals with large spreads reflect the market’s skepticism about the deal closing and that skepticism is warranted, given increased regulatory risks as we saw with the acquisition of Magnachip Semiconductor (MX). The deal was officially terminated on Dec 13th after the company failed to receive regulatory approval in the U.S. We wrote the following about the situation in our November newsletter,

There are always exceptions to rules and this month’s spotlight idea is an exception to my rule of not investing in deals with large spreads. I have been watching the spread on the $1.4 billion acquisition of Magnachip Semiconductor (MX) by Chinese private equity firm Wise Road Capital with interest. The deal was announced on March 26, 2021 with Wise Road agreeing to pay $29 per share in cash for MX after winning a bidding war involving more than half a dozen suitors. The battle for MX did not end after the signing of the definitive merger agreement with Wise Road. Cornucopia Investment Partners made an unsolicited bid on July 11, 2021 to acquire Magnachip for $35 per share in cash. This offer was subsequently withdrawn because of the change in the regulatory environment in the U.S.

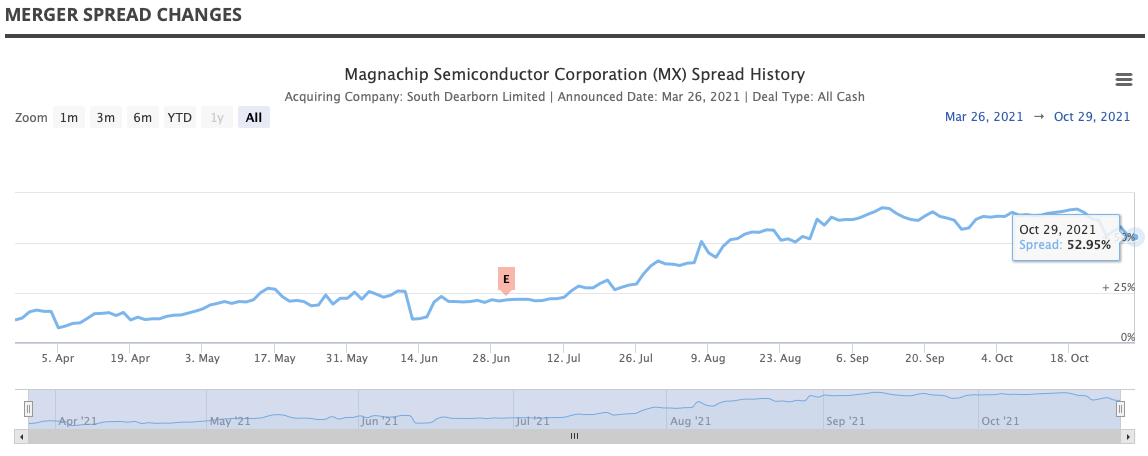

Despite receiving approval from China’s antitrust regulator in late June, the deal has been in regulatory limbo as both the Korean Ministry of Trade, Industry and Energy (MOTIE) and the Committee on Foreign Investment in the United States (CFIUS) are taking a closer look at the deal. This is reflected in the deal spread chart where the spread kept increasing to the point where the stock is now trading very close to the pre-deal price as you can see below.

Magnachip Spread Change Chart

Magnachip’s “unaffected” closing price on March 2, 2021 was $18.83. The stock is currently already trading very close to this pre-deal price and if the stock drops below this price on Monday, it could present an interesting opportunity. If the deal goes through, arbitrageurs stand to make almost $10 per share in two to three months assuming both MOTIE and CFIUS don’t raise further objections.

If the deal fails, Wise Road has to pay MX a termination fee of $105.3 million, which could be reduced to $84.3 million if the deal does not receive South Korean regulatory approval or $70.2 million if it fails to receive U.S. regulatory approval. If the deal fails because MX accepts another offer, then it has to pay Wise Road a termination fee of $42.1 million. Assuming the failure is on account of regulatory issues, MX shareholders would get anywhere from $1.50 to $1.80 per share in termination fees.

There are a couple of ways this plays out. If the deal goes through (I assign a 33% probability of it going through), the upside is north of $10 per share. If the deal does not go through, you end up owning MX for $17 plus change after adjusting for the termination fee. If there is forced selling by arbitraguers after the deal fails, MX might be available at even more attractive prices. We saw this with Willis Tower Watson (WLTW) where the stock dipped to the $200 level after the acquisiton by AON failed and then went on to gain more than 20% in the ensuing three months.

A company that had more than half a dozen suitors and that saw an offer of $35 per share even after the merger was announced is clearly valuable to both strategic buyers and financial sponsors. Looking beyond the bidding war, if the company earns the $1.26 per share the street is expecting for 2022, the stock is trading at a forward 2022 P/E of just 15. The company has a strong balance sheet with $276 million in cash and no debt. A termination fee would help shore up the balance sheet even more. This is a situation where if the deal goes through you win immediately and if it fails, the probability of doing well in the long-term is high.

Magnachip’s stock was weak in recent days on speculation that the deal might not go through but the day after the deal was officially terminated, the stock managed to register a gain of 4.27% to $17.84. The forced selling by arbitrageurs that we normally see after a deal fails didn’t materialize in this case. What we have is a $802 million market cap company with $272 million in net cash on the balance sheet, before receiving the $70 million termination fee. Since we wrote about the company, analyst estimates for 2022 earnings have been revised upwards to $1.40 per share and the company is now trading at a forward P/E of 12.74 and a forward EV/EBITDA under 8.

The company adopted a limited duration shareholder rights plan (a poison pill) to give it time to figure out how to return value to shareholders, and ward off a potential hostile bid given the level of interest the company garnered the first time around. I don’t see how regulatory risks could change for a new suitor and I think the play here is to hold a high quality company that focuses on double digit revenue growth and free cash flow generation. Given the company’s cash position, a special dividend might not be out of the question.

When we started a position in the company last month, we wrote the following in the November newsletter,

I am going to purchase MX at half the standard position size for both the model portfolio and my personal portfolio. If the deal fails, I will add to the position to get it to the standard position size.

With the collapse of the deal announced earlier this week, I am going to add to our position after this mid-month update is published and bring it up to a full size position in both the model portfolio and my personal portfolio.

Voluntary Disclosure: I hold long positions in Mohawk Industries (MHK), Healthcare Trust of America (HTA), Magnachip Semiconductor (MX) and Virtu Financial (VIRT)

We use cookies to ensure that we give you the best experience on our website. If you continue to use this site we will assume that you are happy with it.Ok