- Subscribe

- Premium

- C-Suite

- Insiders

- M&A

- Gurus

- Spinoffs

- Buybacks

- More

This is our third update about new merger arbitrage related positions at funds that tend to have concentrated positions in their portfolio. You can find our first update here and our Q4 2023 update here.

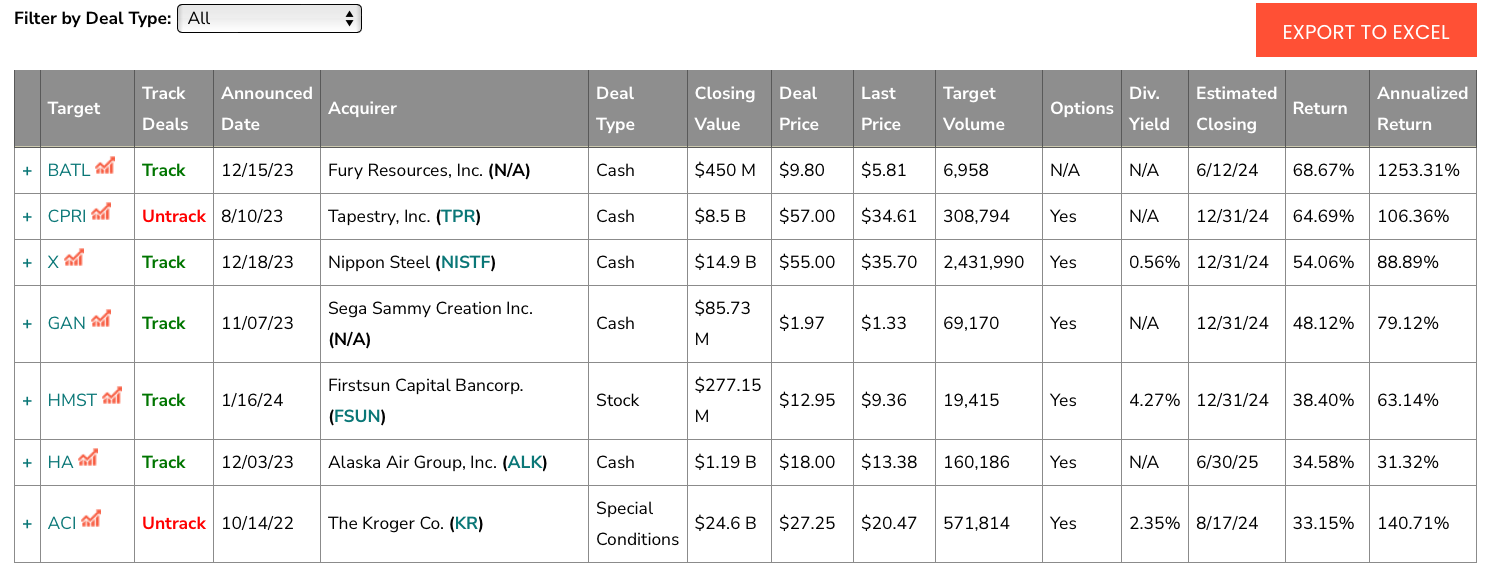

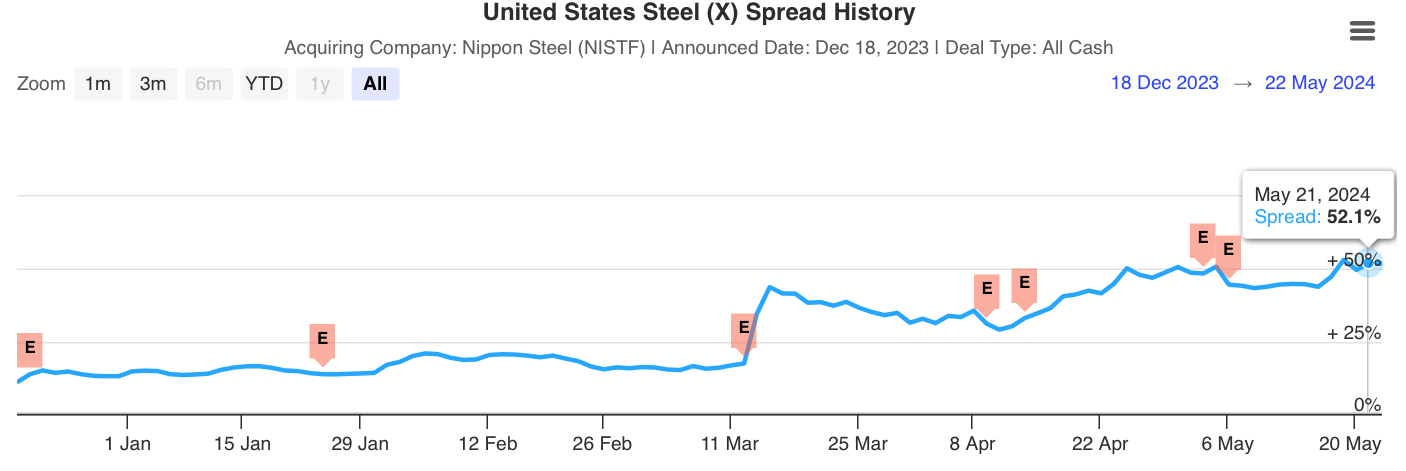

There are currently 78 active M&A situations in the U.S. ranging from highly risks deals like the acquisition of Capri (CPRI) by Tapestry (TPR) that is trading at a spread (potential profit) of almost 65% to the management-led take private of Astra Space (ASTR) in a tiny $15 million deal, which is trading at a negative spread of 22%.

The concentrated funds I like to track prefer to pick and choose among those situations and tend to concentrate more than 50% of their portfolio in their top 10 positions. To reiterate what we wrote about 13F filings in our first article:

“Investment firms with over $100 million in assets are required to file form 13F with the SEC within 45 days after the end of each quarter. This filing provides a small window into the fund manager’s portfolio and is a great source for new investment ideas. You also end up with information that is potentially stale and as many investors have come to find out, you can’t just follow someone else into an idea without doing your own deep due diligence. The Gurus section of InsideArbitrage includes curated lists of professional investors and fund managers categorized based on their investment style.

We are currently tracking 49 event-driven funds of various sizes. There are firms with just 3 positions in their 13F portfolio and others with thousands of positions. This does not mean the former has their entire portfolio is just 3 positions as they may have exposure to other positions, including private companies, which don’t have to be reported on the 13F form.”

I am going to focus on some of the new additions across the seven funds I am tracking. I used to track eight funds but one of them terminated their registration with the SEC in February. The common theme appears to be participating in pre-deal or rumoured deal situations and increased use of options to either protect downside or juice returns on the upside.

There were several other new positions but three funds or less started those positions or the deal had already closed by the time the 13-F filings were released.

It is worth mentioning that Chevron’s $60 billion all stock acquisition of Hess (HES) was a new position for two funds and they joined four others that already had a position. Exxon’s acquisition of Pioneer Natural Resources (PXD) closed this month and was a position for all seven funds, including four that added to that position in Q1 2024.

Two funds purchased put options on Capri (CPRI) and one added to their position. Over the last two quarters six funds had started a position in Tapri’s (TPR) embattled acquisition of Capri for $57 per share in cash.

After reviewing these portfolios and their new additions I am inclined to take a closer look at Fusion Pharmaceuticals (FUSN), Axonics (AXNX) and Juniper Networks (JNPR).

Disclaimer: I currently hold long positions in Spirit Airlines (SAVE), Bristol-Myers Squibb (BMY), Cerevel (CERE) and Capri (CPRI). Please do your own due diligence before buying or selling any securities mentioned in this article. We do not warrant the completeness or accuracy of the content or data provided in this article.