- Subscribe

- Premium

- C-Suite

- Insiders

- M&A

- Gurus

- Spinoffs

- Buybacks

- More

I was reflecting on the performance of my portfolio during the last several years and realized that beyond opportunistic trades both on the long and short sides during the early days of COVID-19 and the use of the merger arbitrage strategy, a large part of it was driven by companies like Vertex Pharmaceuticals (VRTX), Netflix (NFLX) and Meta (META).

These were companies that had temporarily fallen out of favor and provided an attractive opportunity. The key assumption was that the issues or perceived problems they were facing were indeed temporary and for a brief period of time during their regime change from growth to value, they were trading below intrinsic value. If you get that key assumption wrong, you end up with melting ice cube companies like BlackBerry (the old Research in Motion) where there were structural issues once the iPhone was released by Apple (AAPL) and the problems were not temporary in nature.

In an article titled A Season For Every Strategy I wrote the following about being open to adopting different investing styles:

All of this brings me to the question of whether we can start thinking of investing as a seasonal activity instead of a tribal activity where we remain mentally agile to surf the waves that are presented to us rather than the wait for extended periods of time for the perfect wave that fits our style. Can we don our value investor hats after big market declines (2000-2003, 2007-2009, March 2020 and the last six months) and then take it off after the opportunity has passed, realizing that the likelihood of running into value traps is higher once the market stabilizes? Can we subscribe to a season of GARP and event-driven strategies as we look to the future to see what the next season brings? Leaving behind our tribes and opening ourselves up to a different set of values/ideologies is very difficult to do and maybe therein lies the opportunity to achieve superior outcomes.

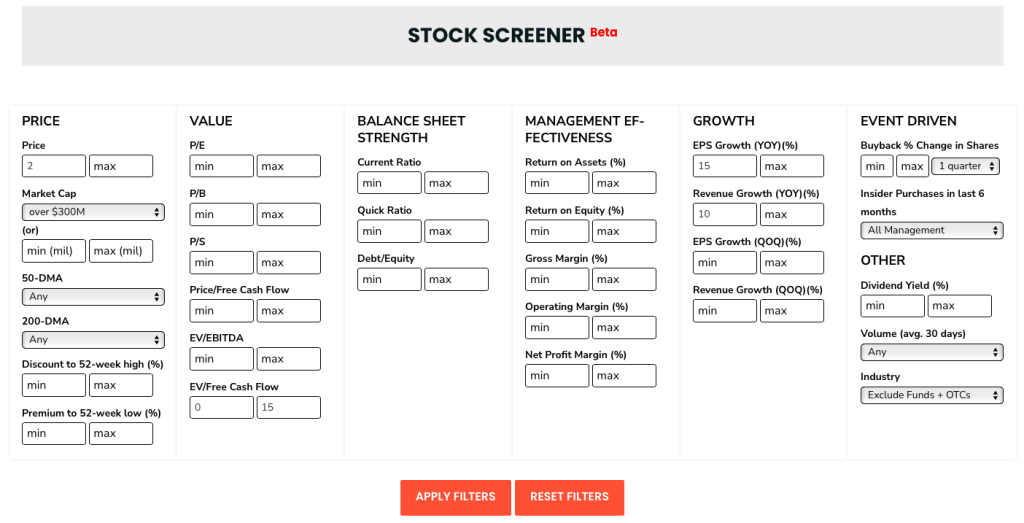

Growth at a reasonable price or GARP has worked well over the last year and I decided to run a GARP screen using our new screening tool to see what kinds of companies it would surface for further research.

The criteria I used were:

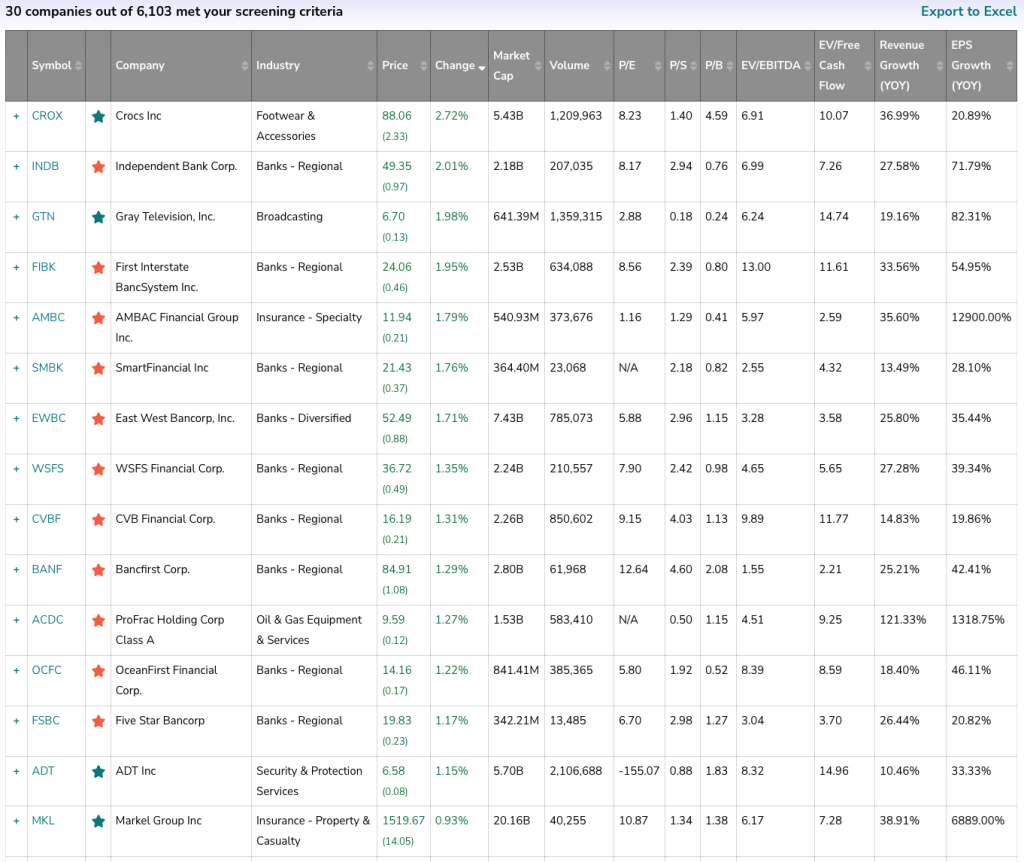

The screen generated 30 companies from a universe of over 6,100 and it was interesting to see companies that I was already following like Markel (MKL), Crocs (CROX) and ADT (ADT) on the list. In fact Crocs was one of the spotlight ideas for our October 2023 Special Situations newsletter and I wrote the following in the conclusion of my Crocs writeup:

Charlie Munger once joked that he had never seen Warren Buffett run a DCF model. Given their extensive experience they don’t really need to run models. For mere mortals like me, I sometimes like to run a simple ten-year DCF model as a quick gut check. Using average analyst estimates of $12.08 and $13 in earnings for 2023 and 2024 respectively and then using a 10% growth rate for 2025, dropping gradually over time to a 3% rate, I get an intrinsic value of $184.23. I used 10% as a discount rate and 2% as a terminal growth rate.

Any way you look at it, the stock is undeniably cheap and is not a melting ice cube as seen by its organic growth in both revenue and earnings. The company has been adequately punished by the market for its pricey acquisition and unless demand collapses due to a deep recession, I like the company’s prospects over a three to five-year period.

The list also included a broadcasting company, an auto manufacturer and an electronic components manufacturer that I added to my watch list for further research. There were surprisingly few oil & gas companies but more than a fair share of banks.

I have included a screenshot below with some of the companies generated by the screen:

Screens suffer from several issues including hindsight bias and data issues but I like to use them from time to time as a starting point to see if they generate ideas worth exploring further. Happy hunting.