- Subscribe

- Premium

- C-Suite

- Insiders

- M&A

- Gurus

- Spinoffs

- Buybacks

- More

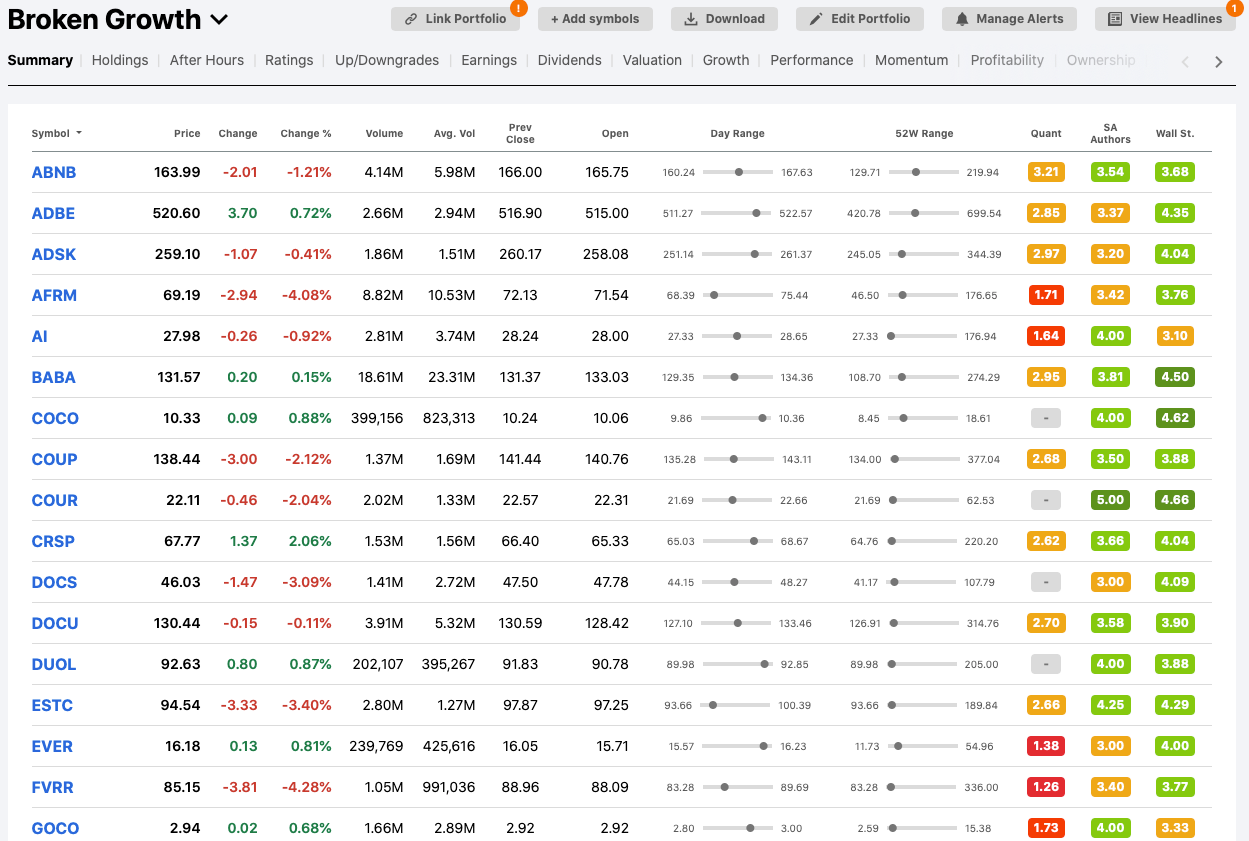

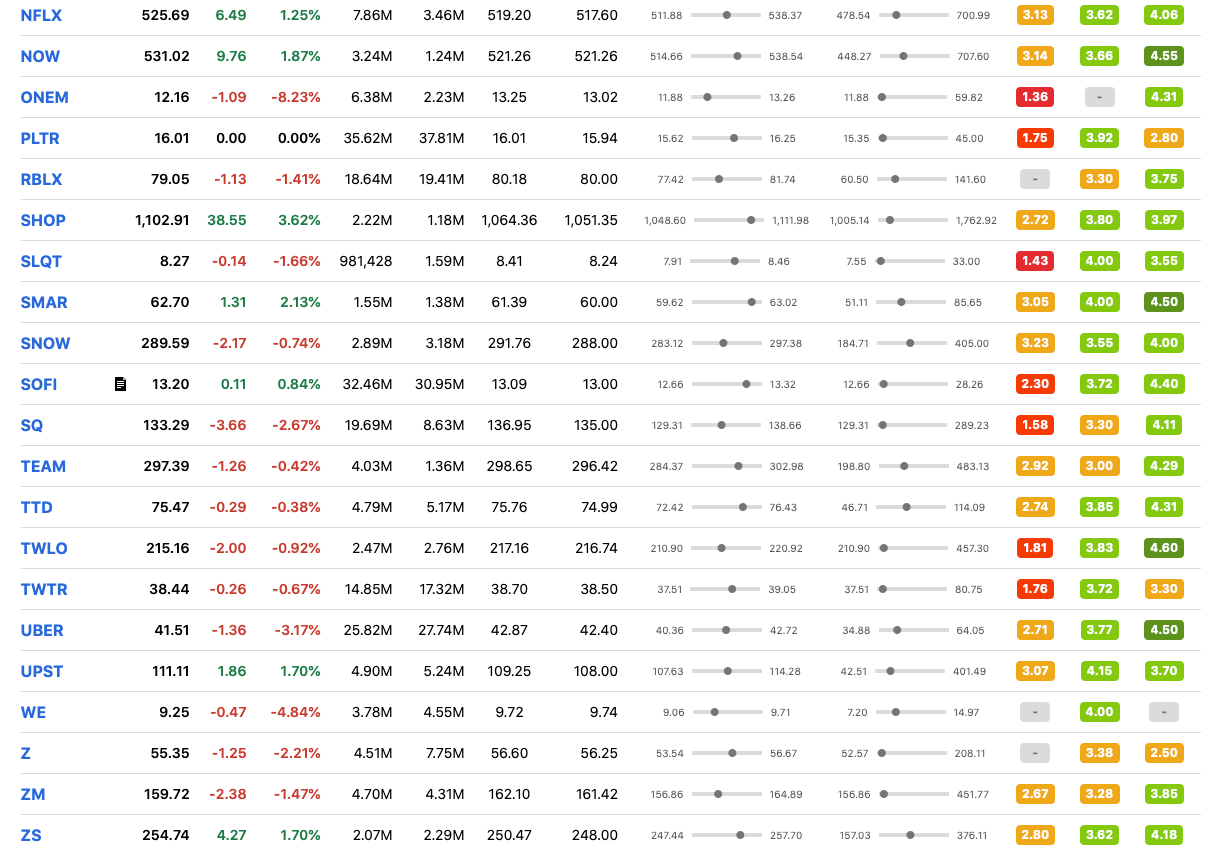

We started the year discussing a basket of “Broken Growth” stocks that had declined anywhere from 50% to 70% from their peaks and looking at the universe of SPACs for short ideas in an article titled January 2022 Mid-Month Update: SPAC Attack. It is fitting that we end the last mid-month update of the year discussing another company from that list of 38 broken growth stocks (screenshots included at the bottom of this article). Three of the companies on that list including Twitter, 1Life Healthcare (ONEM) and more recently Coupa (COUP) ended up with definitive merger agreements and the company I want to discuss today is likely to be another acquisition target.

Not every company on the list was a potential long opportunity. For the better part of this year we were short WeWork (WE) and closed the position two weeks ago for a gain of 57%. Unfortunately the ones we picked on the long side like Doximity (DOCS), Coursera (COUR), Twilio (TWLO) and Nextdoor (KIND), also did not fare well. Thankfully we started all of them at well below our usual position size and only added to one of them. I still hold all of them and plan to add to them at some point in 2023.

Most bubbles end with a few bankruptcies and M&A among some of the survivors. While many of the companies from the broken growth list have declined sharply, we haven’t seen a lot of bankruptcies yet but have been seeing M&A activity and I expect that activity to ramp up in 2023. Private equity firms that raised huge funds still have a lot of capital to deploy and they are going to be looking at the universe of unique growth companies that can’t get their act together and generate either positive net income or free cash flow.

I was discussing the enterprise AI software company C3.ai (AI) with my brother last weekend and was struck both by how far the stock had fallen and how much cash the company had on the balance sheet. Along with Snowflake (SNOW), C3.ai was another highly anticipated IPO in 2020 and both companies soared after going public. Snowflake, which priced its IPO at $120 per share in September 2020 went on to peak at over $400 per share three months later. C3.ai, which went public in December 2020, just days after Snowflake’s peak, priced its IPO at $42 per share and peaked the same month at nearly $184 per share. The stock currently trades at $13.04, an astounding peak-to-trough decline of 93%.

The world has been recently fascinated by ChatGPT, the AI system that can write limericks, articles and even code. I discussed my experience with AI in an article earlier this year called Pattern Matching, where I wrote,

A lot of what we do as investors could be best described as pattern matching. We are constantly looking at new opportunities or existing positions though the lens of our past experience and using current information to see if we can spot familiar patterns. As humans, we are prone to making mistakes and our pattern matching process is likely colored by,

- our inherent biases

- the impact of emotions like fear and greed and

- more importantly forgetting exactly how a past investment unfolded.

Given these human limitations, the question that comes up is whether machines are better equipped for pattern matching and making the investment decisions for us. I got a chance to experience this firsthand when a business partner and I embarked on a six year journey to dive deep into insider transactions to look for unique insights and strategies. After two years of traditional data analysis, we pivoted to using artificial intelligence or machine learning to see what the machine learning models could pick up. What was remarkable was that the machines within weeks picked up the same insights and strategies we found through the prior two years of traditional data analysis.

The machine learning algorithms we used back then are archaic compared to what is out there right now. Getting behind the wheel of a self-driving car or taking a ride in a robo taxi operated by Google’s Waymo or GM’s Cruise divisions makes you realize just how effective pattern matching can be. Obviously there are edge cases, where the machine encounters something it has not experienced before and things go wrong, leadings to bad outcomes including fatal crashes. Most programmers, including the ones that don’t work on machine learning, are acutely aware of edge cases.

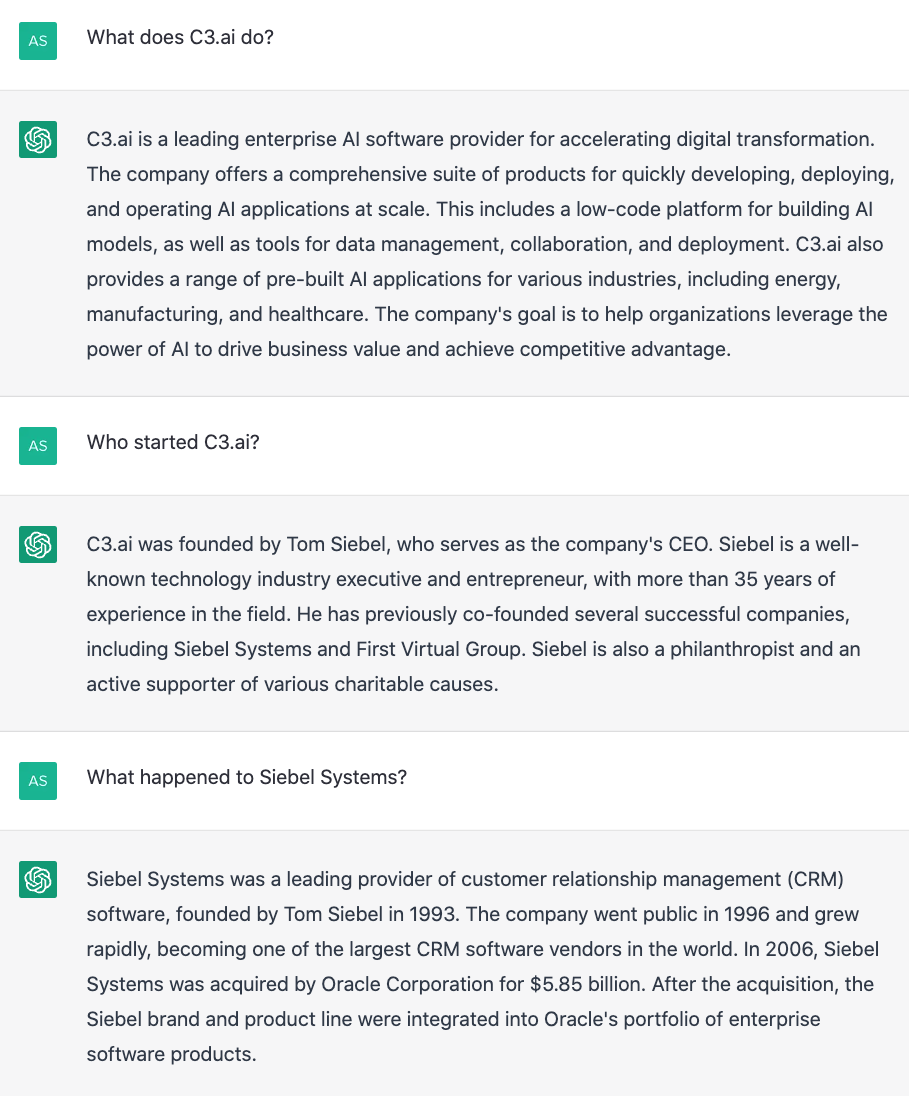

Instead of trying to explain what C3.ai does, I figured it would be appropriate to let an artificial intelligence program do it for me. I decided to ask ChatGPT and it did a pretty good job of providing a company outline as you can see below.

I always thought of C3.ai as an AI focused consulting services firm. When I pulled up the company’s financials, I noticed that it had TTM gross margins of almost 73%, which is inline with what you would expect from a software product company and not a services company. For example, Oracle’s gross margins are 76%, while Accenture’s gross margins are just 32%.

I reached out to a friend who has a Ph.D in machine learning and runs his own AI firm to discuss C3.ai and he confirmed my hunch that C3.ai offers both products and services. Despite the impressive gross margins and the rapid growth rate the last few years, the company remains unprofitable. Some high growth companies post losses but when you look at their cash flow statements, they generate free cash flow after adjusting for egregiously high stock-based compensation and other items.

Unfortunately that is not the case with C3.ai, which posted negative free cash flow to the tune of $90 million in fiscal 2022 ended April 2022 and negative FCF of $201.7 million during the trailing twelve months. Normally my analysis would have ended at this point and I would have either discarded the company or put it on a secondary watchlist. There is usually no floor to be found in these unprofitable companies and the fact that it is down 93% from its peak might not stop it from losing half its value from current levels.

The three things that gave me pause are,

C3.ai is still a “show me” story and the company has pivoted multiple times during its short history, starting at first with a focus on the energy sector (Baker Hughes is both an investor and has committed to certain minimum levels of revenue over a six year agreement), then IoT and eventually AI. Investors have lost patience with show me stories and if growth falters, these kinds of companies fall rapidly with no bottom to be found. We saw a moderation in both growth and margins at C3.ai, with fiscal Q2 2023 revenue growth decelerating to 7% YoY and gross margins slipping to 67%.

With an experienced CEO at the helm, a new business model that is showing strong traction, the potential of AI to transform industries and an inexpensive stock with a cash rich balance sheet, the positives outweigh some of the negatives with C3.ai.

I am going to start a position in both the InsideArbitrage model portfolio and my personal portfolio at half our standard position size after this mid-month update is published. I plan to add to the position in the coming quarters if the company can reduce its cash burn and we start seeing traction on the top line.