- Subscribe

- Premium

- C-Suite

- Insiders

- M&A

- Gurus

- Spinoffs

- Buybacks

- More

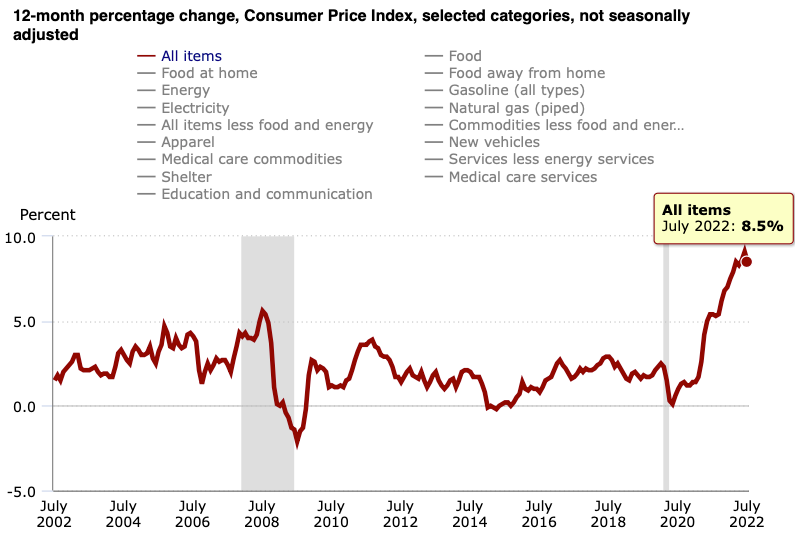

Inflation is a hidden tax that impacts everyone and especially the less fortunate among us. Unless you own your home, drive an electric car, don’t eat out much and grow your own food, the recent big spike in inflation likely impacted you. The 20 year CPI chart below shows the unusual nature of the current inflationary period.

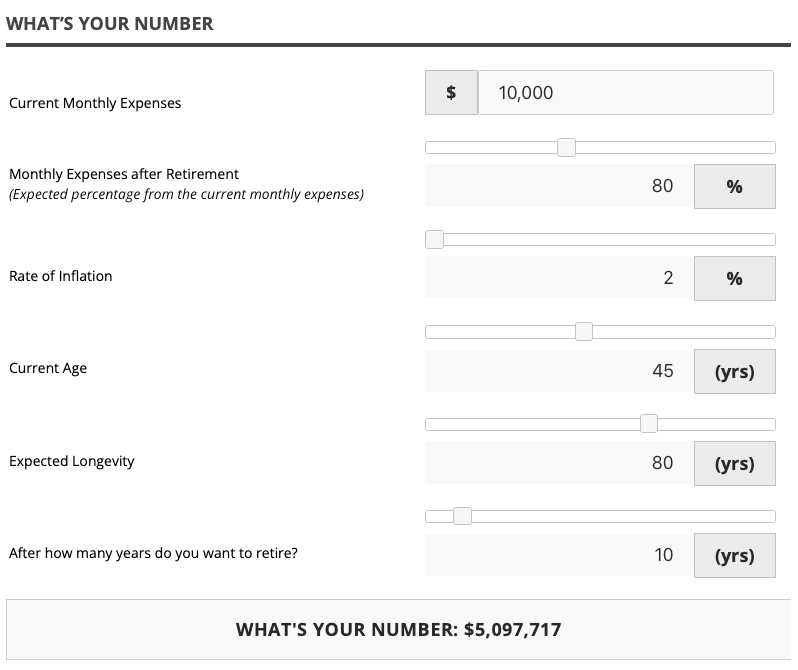

Last week in our What’s Your Number article, we discussed how figuring out the amount of money you need for retirement is a multi-faceted problem that is unique to each of us. When playing with the inputs that go into our What’s Your Number tool, I was struck by just how big of an impact two of those inputs had on the results. Just a small change could switch the eventual outcome from leaving millions of dollars for your heirs/charity to being without money in the later years of your retirement.

One of those two factors was the expected rate of inflation during retirement. When we were building and testing this free tool, I rarely changed the rate of inflation and usually left it at 2% as I tried hundreds of tests with different variables. One of the mandates for the Federal Reserve is to achieve inflation that averages 2% over time and as you can see from the chart above, barring some short periods of time, on average we stayed close to that 2% level. To illustrate the impact of inflation on a retirement plan, let us modify some of the inputs we used to determine my hypothetical retirement number last week. I have reused the scenario we used last week below.

For example,

my number works out $5,097,717 or a little over $5 million.

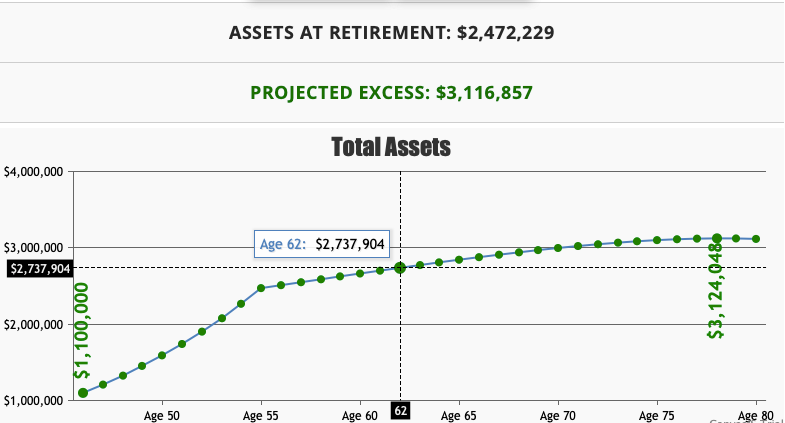

If I currently have $1 million in liquid assets, those assets are generating 8% a year in after tax returns, I save an additional $20,000 each year before I retire and every year that saving rate goes up by 2%, I will have $2,472,229 or almost $2.5 million when I retire at the age of 55. Based on my expected longevity to age 80, after paying for my retirement expenses, I will be left with a surplus of $3.12 million that can go to my survivors or charity. In other words they would be enough to cover my retirement and my principal would have grown despite all the withdrawals. Adjusting for inflation, the purchasing power of that $3.12 million is likely to be significantly lower thirty five years from now.

If I currently have $1 million in liquid assets, those assets are generating 8% a year in after tax returns, I save an additional $20,000 each year before I retire and every year that saving rate goes up by 2%, I will have $2,472,229 or almost $2.5 million when I retire at the age of 55. Based on my expected longevity to age 80, after paying for my retirement expenses, I will be left with a surplus of $3.12 million that can go to my survivors or charity. In other words they would be enough to cover my retirement and my principal would have grown despite all the withdrawals. Adjusting for inflation, the purchasing power of that $3.12 million is likely to be significantly lower thirty five years from now.

Now let us move that inflation number up from 2% to 4% without changing anything else. My number now changes to $8.2 million from a little over $5 million and instead of a projected surplus of $3.12 million at the end of my life, I am now left with a steep shortfall of almost $3 million by the time I am 80 years old. I essentially run out of money by the age of 74, 19 years after retirement.

There are several ways to offset this impact including but not limited to,

Each of these adjustments present their own challenges. I had estimated that in retirement I would only spend 80% of my pre-retirement expenses per month. Cutting back further could change things from a comfortable retirement to an unpleasant one that leaves little room for error. Owning a fully paid off home or even one with a low fixed rate mortgage could help a great deal. Delaying the retirement age and picking up a part-time job (if possible) are more palatable options.

The last option of generating more than 8% after-tax returns on the investment portfolio on a consistent basis is the hardest part. Most retirement portfolios are structured to have more exposure to less volatile asset classes like bonds, which over long horizons tend to have significantly lower returns compared to equities.

An 8% after-tax annual rate of return with low volatility is a tall order. Lest we forget, Bernie Madoff, pulled off one of the biggest Ponzi schemes in history promising just 10% annualized returns. My portfolio would have to have a large number of high quality dividend paying stocks that have grown their dividends over the decades I held them, a carefully selected group of merger arbitrage situations to beat the returns of an equivalent bond portfolio and a sprinkling of high growth companies that provide upside potential that can help the portfolio grow.

Late last year, I was playing with a number of discounted cash flow (DCF) analysis models for high growth stocks. I was doing this on multiple Google sheets and we have now built a premium tool on InsideArbitrage that allows you to do this easily. I did not believe that the inflation we were seeing was transitory and it was hard to come to a different conclusion after looking at what had happened to the M2 money supply thanks to all the stimulus money ending up in bank accounts. Moving the discount rate up in the DCF models had a huge negative impact on the valuation of these stocks and especially those companies that were currently losing money with expectations of becoming cash flow positive in the distant future. This was the canary in the gold mine for me and caused me to stick the picture of a bear on my 2022 outlook article.

The impact of a high rate of inflation on a retirement plan is very similar. While we should expect a higher rate of return on our investments during a period of high inflation, there is no guarantee this would be possible. Being aware of the factors that can have a large impact on our retirement – especially in the later years when our options are limited and our needs greater – is important. The sooner we are aware of them and the levers that are available to us to offset this impact, the better prepared we would be to avoid becoming financially dependent on our children, the state or the kindness of strangers.