- Subscribe

- Premium

- C-Suite

- Insiders

- M&A

- Gurus

- Spinoffs

- Buybacks

- More

Is $2 million enough money for a comfortable retirement? The answer to this simple question is as unique and varied as each of us and our complex lives. Over the years I have had several conversations with friends about the money they think they need for retirement and the number they come up with often surprises me. The number is often overstated and the more assets they appear to already have, the higher the number appears to be. The concept of “your number” should ideally be simple enough where you know what you need to meet your monthly living expenses and a little extra for unforeseen circumstances. However there is a deep gorge between what is ideal and the ground reality.

Coming up with “your number” is difficult because it is a multi-faceted problem with a mix of unknowns, expectations, fears and desires. Some folks may not even have a good grasp of their monthly budget and savings. Starting today, we are rolling out a large number of free and paid tools on Inside Arbitrage that span the gamut of a DCF modeling tool to estimate the intrinsic value of an investment to a monthly budgeting tool that can help you figure out what your monthly budget is and how much you save. Once you have a handle on your total monthly income, your expenses, monthly savings and current assets (cash, investments, real estate, etc.), getting to “your number” may appear less daunting.

For me, my number is the amount of money invested in moderately safe investments that can generate the living expenses I would need in retirement with a little extra for emergencies so that the principal remains untouched. Let us unpack this statement and break it down.

I still remember filling up my beat-up Ford with gas that cost $1.44 per gallon as a grad student in Oregon twenty three years ago but now pay more than $5.50 per gallon in California. That number could just as easily be $10 per gallon if I plan to retire twenty years from now or we might be an all-electric world and there would be no gas stations. The state or country you choose to retire in can also have a huge impact on your expenses in retirement. There are seven U.S. states including Washington, Texas and Florida that don’t have personal income taxes. You might however end up paying more in property taxes or utilities if your retirement location is hotter or colder than where you live now.

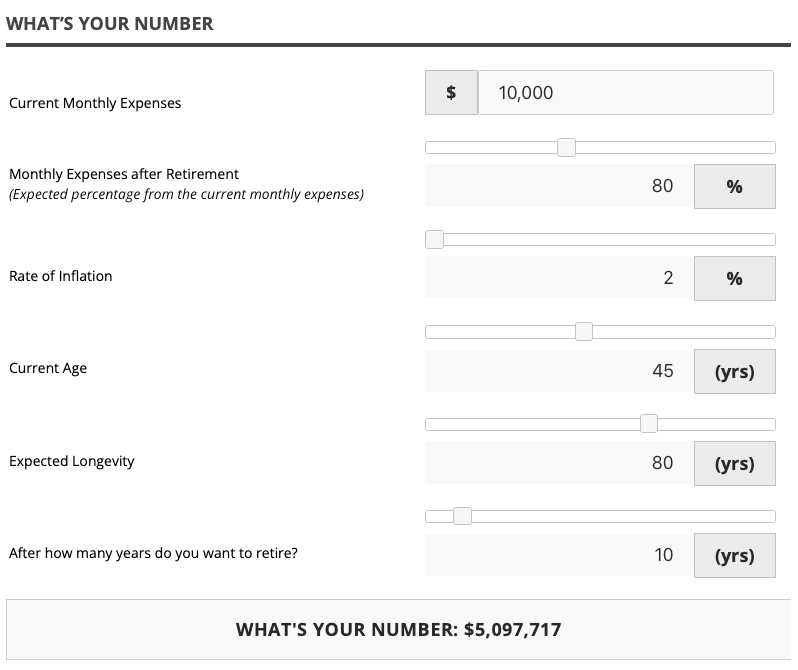

To make things easy, we decided to build the What’s Your Number tool that lets you play with all these factors to see what you number is and if you are likely to end up with a surplus or shortfall at the end of your expected life. If you are receiving this email, you already have free access to this tool by logging into Inside Arbitrage.

For example,

my number works out $5,097,717 or a little over $5 million.

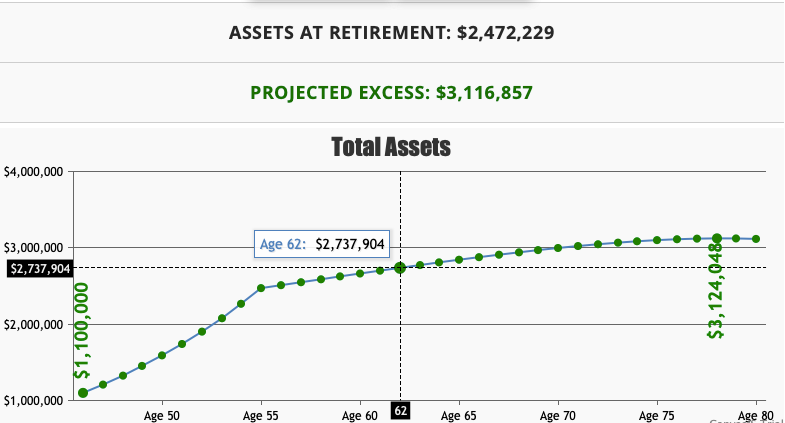

If I currently have $1 million in liquid assets, those assets are generating 8% a year in after tax returns, I save an additional $20,000 each year before I retire and every year that saving rate goes up by 2%, I will have $2,472,229 or almost $2.5 million when I retire at the age of 55. Based on my expected longevity to age 80, after paying for my retirement expenses, I will be left with a surplus of $3.12 million that can go to my survivors or charity. In other words they would be enough to cover my retirement and my principal would have growth despite all the withdrawals. Adjusting for inflation, the purchasing power of that $3.12 million is likely to be significantly lower thirty five years from now.

Obviously all of this depends on the assumptions I provide to the What’s Your Number tool. An 8% after-tax return on a conservative portfolio may be overtly optimistic and a 2% inflation rate given our current environment may also seem optimistic. I plan to cover the impact of changing these numbers in an article next week. In the meantime, you can input your own assumptions to see how it impacts your number.

Editor’s note: This article was originally published on our sister site PowerCompounding.com and is being reproduced on Inside Arbitrage with some changes.