- Subscribe

- Premium

- C-Suite

- Insiders

- M&A

- Gurus

- Spinoffs

- Buybacks

- More

I don’t often do an end of year look back but this year was so unusual that I wanted to put it down in words before it gets lost to the mists of time.

Personal

On the personal front, the year was a big rollercoaster. I lost a childhood friend who departed much too early in his 40s and left behind a young family. It was also the year when I got to check off a few things off my bucket list including attending my first Berkshire Hathaway meeting, presenting for the first time at ValueX Vail and completing my first book. I also got a chance to be a guest on a couple of podcasts including this one with Jesse Felder that I enjoyed a ton.

This was also the first year I got to spend almost full time on my investment research business InsideArbitrage and launch my advisory service Inside Arbitrage Advisors.

I had to work on myself to improve productivity, spend quality time with family, dedicate time to do deep dives into investment opportunities, train an amazingly supportive team and introduce non-negotiables in my life (learn a foreign language and workout everyday). Three books I enjoyed reading this year included Relentless: From Good to Great to Unstoppable (thanks for the recommendation Chris), The Voltage Effect by John List and Towers of Debt: The Rise and Fall of the Reichmanns by Peter Foster.

InsideArbitrage Business

When I launched InsideArbitage six years ago, it was a part-time passion project that complemented my personal investment journey with a focus on event-driven or special situations investing. Last year I decided to quit my job at a private equity-funded healthcare services company in San Francisco to focus full time on InsideArbitrage.

We decided to expand both the breath and depth of the platform by adding C-suite transitions, a daily event-driven monitor, a curated gurus section, a screener that includes event-driven filters like buybacks, user portfolios, an M&A calendar, an online community and more. I was also lucky enough to convince a friend and one of the smartest yield-focused investors I know, to launch the Yield Guru service on InsideArbitrage.

Revenue growth for 2022 fell 1% shy of my 50% goal and is on track to slightly exceed my 35% goal for 2023. I hope to ramp up growth an additional 50% in 2024 through a series of initiatives and experiments including our first acquisition that we plan to announce in January. Thinking of growth initiatives as experiments was important to help me double down on what was working and not regret the time and money spent on things that didn’t work.

The platform has been an amazing source of new investment ideas for me and I have enjoyed exchanging ideas with a small group of investors that I meet on a regular basis over Zoom or for lunches all over the San Francisco Bay Area.

InsideArbitrage Portfolio Performance

The InsideArbitrage model portfolio generated 14.78% returns in 2023 as of December 27, 2023.

In any other year this would have been considered a respectable return, especially when a portion of the portfolio is dedicated to merger arbitrage situations. Especially, coming off 2022 where the model portfolio managed to eke out a small gain when compared to very significant losses in the S&P 500 and an even larger loss in the Nasdaq of 34%.

However 2023 was not a typical year. Both the Nasdaq and S&P 500 roared back and while we participated in the rebound this year to double digits returns, our performance was nowhere close to the S&P 500. Over a two year period, the model portfolio did end up outperforming the S&P 500.

So what went right and what didn’t work out for us in 2023? At the start of 2023 the discussion was mostly about whether we will end up in a hard landing or by some miracle the Fed engineers a soft landing by the second half of 2023. A recession did not follow an unprecedented rate hike cycle but instead GDP increased 4.9% in Q3 2023, inflation tapered off and markets bounced back. In our August 2023 Special Situations Newsletter I wrote,

This isn’t a Goldilocks economy, this is a miracle. I looked at data going back more than three decades and never have we increased interest rates by such a large magnitude and in such a short period of time. Four back- to-back 75 basis point interest rate increases were not a scenario anyone would have had in their models going into 2022. Yet, we are in a market approaching its all- time highs set in December 2022 even as the yield curve remains stubbornly inverted for months.

The Federal Reserve usually gets a bad rap and it is often what market participants like to point a finger to when monetary policy wreaks havoc on financial markets. I have also been a critic of the Fed in the past.

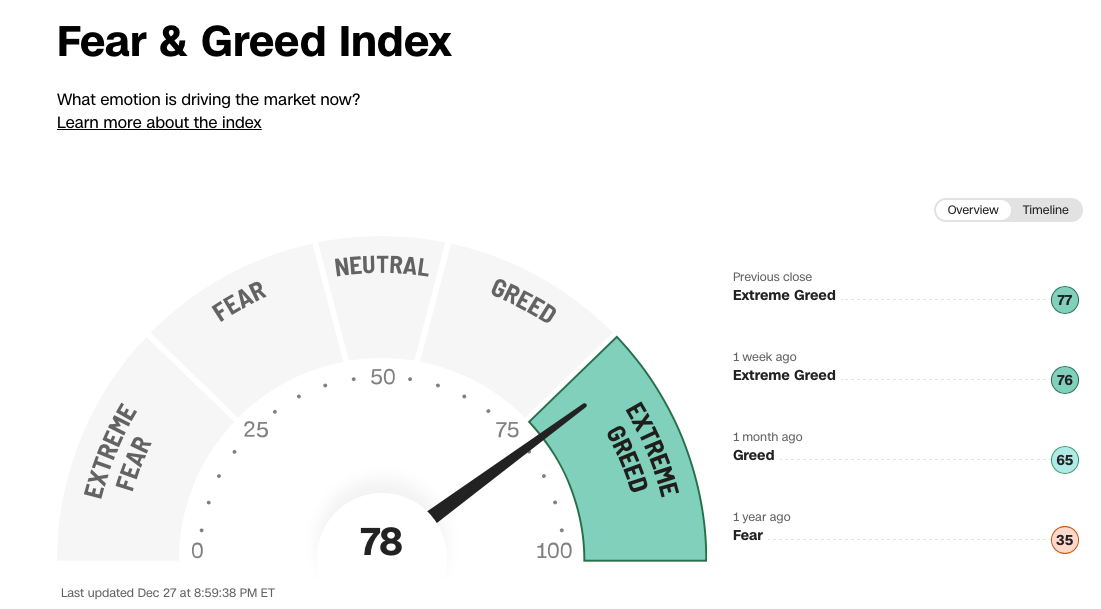

This time around, the Fed was once again wrong by expecting inflation to be transitory in late 2021 and waiting too long to raise interest rates. Despite these shortcomings, what the Fed has managed to engineer is not just a soft landing but a miracle. Beyond GDP growth, a decline in inflation and low unemployment, we also saw credit card delinquencies decline in June and homebuilder confidence increased for the seventh month in a row to over 56 in July. In such an environment, it is not surprising to see that market sentiment, measured by the CNN Fear & Greed index finds itself solidly in extreme greed territory.

The model portfolio’s exposure to commodities (copper and oil), short positions (GameStop and some SPAC “science projects”) and investments across multiple industries helped us do well this year. The merger arbitrage strategy has been a strong performer for us in prior years and has helped us do well in challenging market conditions but we were not quite as fortunate this year. While several merger arbitrage and pre-merger situations worked out great for us (Activision Blizzard, Seagen, Oak Street Health, Momentive and 1Life Healthcare) there were a few that failed (Magnachip, Tower Semiconductor, Tegna and First Horizon) and dragged down our performance.

I continue to like our investments in General Electric (GE), industrial company ITT (ITT), oil services company Atlas Energy Solutions (AESI) and Vertex Pharmaceuticals (VRTX), which came our way through Two Briefcases Bruce.

Looking ahead, I am very concerned about the first half of 2024 and plan to scale back exposure significantly in the coming days with a focus on retaining positions in a few high quality companies or specific event-driven situations. A combination of mean reversion, sentiment at extreme greed and extended valuations all give me pause.

I want to thank friends and investors who have enriched my life this year and especially my family who have supported the burning of endless gallons of midnight oil. Wishing all of you a wonderful 2024.