- Subscribe

- Premium

- C-Suite

- Insiders

- M&A

- Gurus

- Spinoffs

- Buybacks

- More

This mid-month update is a couple of days late because I was in Dallas, Texas attending the IDEAS Conference where nearly 60 companies were presenting. It was an eclectic mix of companies across industries – ranging from a chocolate franchisor with a market cap of just $25 million (RMCF) to a $4 billion aircraft leasing company (FTAI).

Considering the conference was in Texas, there were a large number of energy companies including non-operator oil production companies like Vitesse Energy (VTS) that was spun out of Jefferies (JEF) earlier this year, and oil services companies like Ranger Energy Services (RNGR) that provides onshore oil rigs.

To fit the 60 presentations in two days, at any given time 3 companies were presenting simultaneously. I narrowed the list to 20 companies based on a set of quantitative criteria before the conference (growth, balance sheet strength, profitability, future earnings estimates, etc.). I eventually attended 17 presentations and the parts that were the most useful were the QA sessions that followed the presentation. I also found sidebar conversations with CEOs and CFOs about the state of their industry and big picture headwinds/tailwinds such as the impact of consolidation in their industry or the impact of high interest rates insightful.

For this mid-month update I was contemplating between covering some of the recent challenges faced by mid-market investment bank B. Riley (RILY) or sharing the two most compelling ideas from the conference. I figured I would share the two ideas and cover B. Riley in more detail in our next Insider Weekends article this Sunday. There was a lot of insider activity at B. Riley this week including both purchases and sales triggered as a result of margin calls.

One of the reasons I was excited to attend the IDEAS Conference was that many of the companies presenting were already on my radar due to frequent insider purchases. I’ll keep the writeup of these two ideas brief. If you would like to see my quick notes for other companies or specific investor presentations, feel free to drop me an email. The full list of companies that were presenting can be found here.

Energy Recovery (ERII): $19.48

Market Cap: $1.10B

Enterprise Value: 1.01B

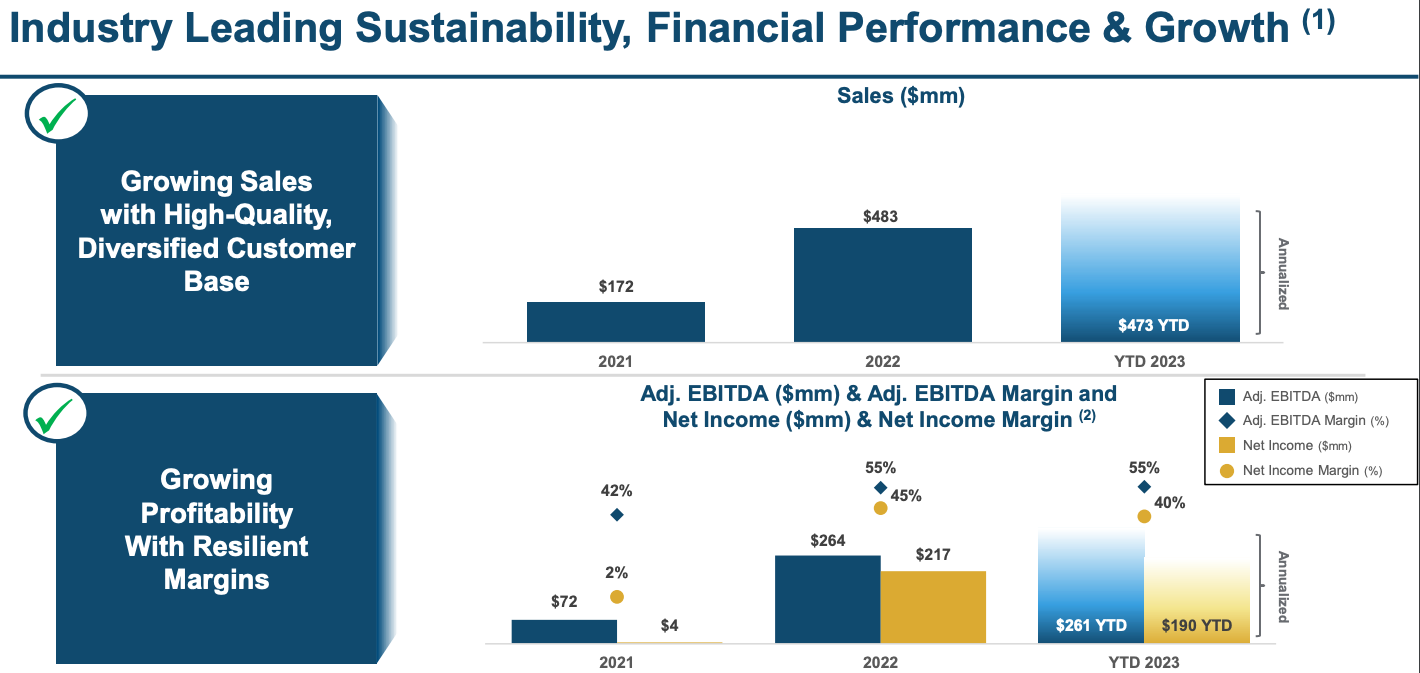

Small and micro cap stocks have had a rough go over the last decade compared to their larger brethren. It was not surprising that many of the companies at the conference were trading at what appeared to be very low valuations. Energy Recovery was a huge exception. The stock was trading at 72 times trailing P/E, 59 times trailing EV/EBITDA and 45 times forward EV/EBITDA. These numbers would make even the fastest growing tech unicorns blush.

Unlike those unprofitable unicorns, Energy Recovery is solidly profitable and the P/CF ratio looked a little less outrageous at 28. They also happen to sport software like margins with a 2022 gross margin of 70% and operating margin of 20%. My quick quantitative notes about the company before going into the conference were:

“Strong forward revenue growth, net cash on balance sheet, earnings estimates neutral, strong margins and high valuation. Insider buying. What is driving growth?”

My question about what was driving the company’s strong revenue growth and its premium valuation were quickly answered. The company had engineered a turnaround starting in 2016 that helped with revenue growth and eventually returned them to profitability.

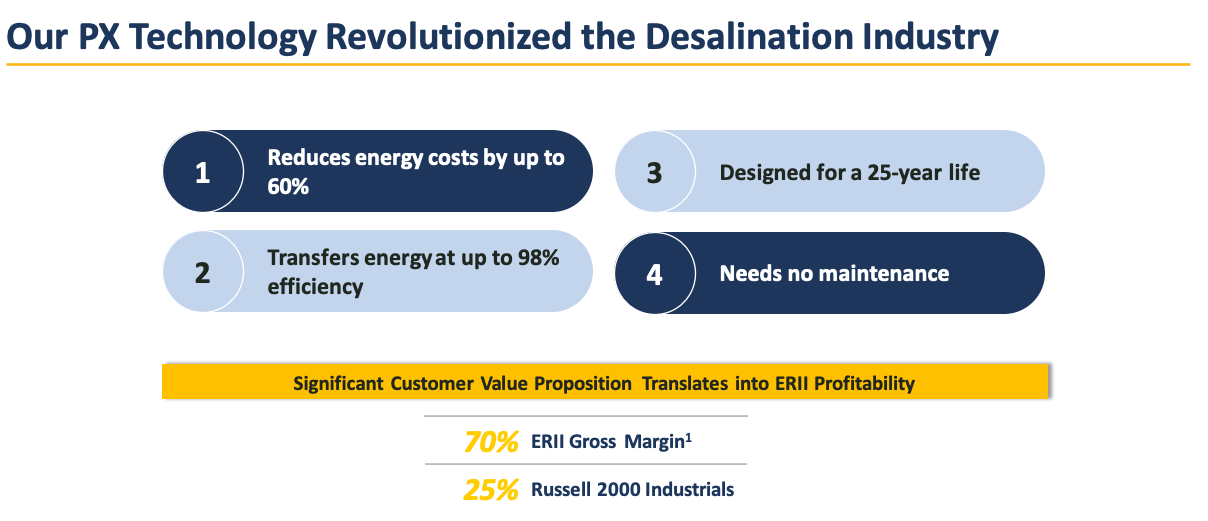

A big reason for this turnaround was an innovative technology they developed for water desalination called the PX pressure exchanger. A combination of displacing their key competitor in 2016 and much better efficiency compared to thermal desalination drove growth. The cost of desalination through their reverse osmosis process is only about 25% of thermal desalination. As the world heats up and fresh water sources become scarce, desalination is an alternative many governments will consider.

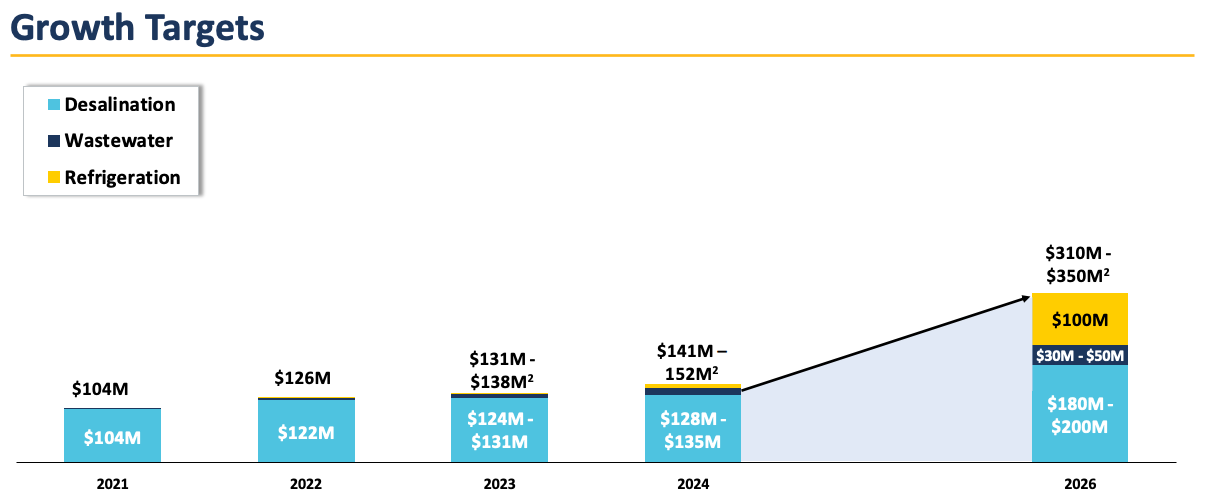

The team presenting appeared both confident and very bullish. They indicated that they expect to see cash flow increase in the next two quarters. The company is expanding beyond desalination and treatment of wastewater to adjacent industries that can use the same innovative PX pressure exchanger technology.

Hydrofluorocarbons (HFCs) are 13,000 times worse for the environment compared to carbon dioxide. Countries around the world are in the process of replacing HFCs for refrigerants with CO2 and Europe is leading the way in this change. The U.S. EPA has also proposed the banning of HFCs starting in January 2025. Unfortunately using CO2 for refrigeration is more energy intensive when compared to HFCs. Energy Recovery has built components that can integrate with commercial refrigeration systems that use CO2 and significantly improve efficiency.

They signed their first contract in 2021 and installed their first unit in Q1 2023 at Carrefour. While relatively unknown in the U.S., I first came across a Carrefour more than 20 years ago in Dubai and shopped at one in Paris last year. The company is an international supermarket chain that is headquartered in France and has operations in more than two dozen countries.

Energy Recovery expects future growth to come from both wastewater treatment and CO2 refrigeration. It is currently working to get a contract for a large wastewater treatment project in the UAE.

The company is also focused on the bottom line and expects its EBITDA margin, which is already higher than most Russell 2000 industrial companies, to improve over the next few years.

The company is also focused on the bottom line and expects its EBITDA margin, which is already higher than most Russell 2000 industrial companies, to improve over the next few years.

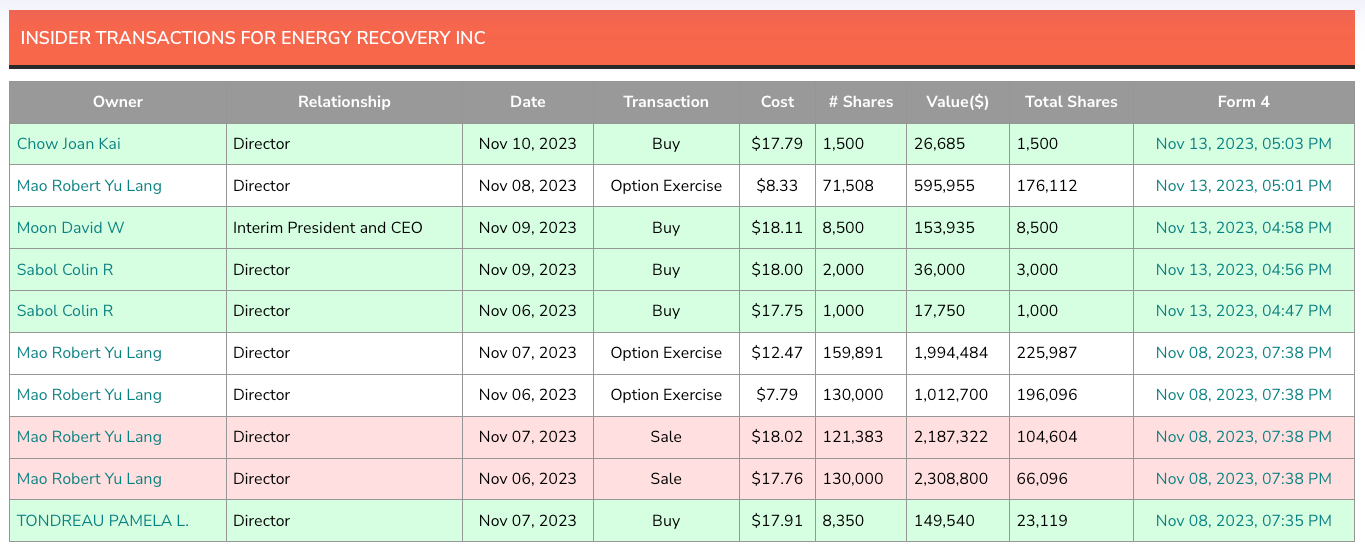

The two key concerns I have about the company are the valuation and the fact that the CEO Robert Yu Lang Mao resigned last month after nearly four years at the company. He will remain on the board but will no longer be the Chair of the board. A board member stepped in as Interim CEO while the company looks for a permanent replacement. I don’t mind paying up for quality but given the premium valuation Energy Recovery is trading at, I am instead going to add it to our watch list and see who takes on the mantle of CEO before deciding to initiate a position.

Atlas Energy Solutions (AESI): $17.11

Market Cap: $1.65B

Enterprise Value: $1.51B

Note: My enterprise value calculation is different from most financial websites because I am excluding $987 million in redeemable non-controlling interest when calculating EV. More details about this in pages 11 and 20 of the Q3 2023 10-Q.

Atlas Energy Solutions is an Austin, Texas based oil services company with a simple business model. They deliver sand to oil & gas producers that use both sand and water to fracture rock formations and generate oil & gas in the Permian basin. The Permian basin, located in West Texas, is the highest producing oil field, responsible for nearly half of all U.S. oil production.

A company that delivers sand is a commodity business and likely to have low margins. This is not the case with Atlas Energy Solutions and there is more going on under the surface (pun not intended), including the construction of something called the “Dune Express”. The Dune Express reminded me of Michael Lewis’ book Flash Boys that recounts the laying of a “as the crow flies” fiber-optic cable between Chicago and New Jersey for $300 million. The project required going through mountains and was done to shave a mere 4 milliseconds off the time it takes to transmit data and facilitate high frequency trading. More on the Dune Express later.

Despite tall claims by oil & gas producers that they were going to hold the line on production and prioritize returning capital to shareholders, we have seen a boom in fracking and increased production over the last year. Atlas has benefited from this boom with a very rapid increase in both revenue and profitability. The company capitalized on this boom and went public in March, 2023 at $18 per share. After running up to over $24 per share by late September, the recent weakness in crude oil prices has seen the stock decline to below its IPO price.

My quick quantitative notes about the company before going into the conference were:

“High growth, high debt, earnings estimates very negative, great margins and low valuation. CEO purchase.”

The high debt note was incorrect because of how the non-controlling interest is reported as debt on most websites. I am glad I looked at the balance sheet from the last 10-Q when doing research after the investor presentation. Not including that nearly $1 billion non-controlling interest, the company has nearly $150 million in net cash on its balance sheet.

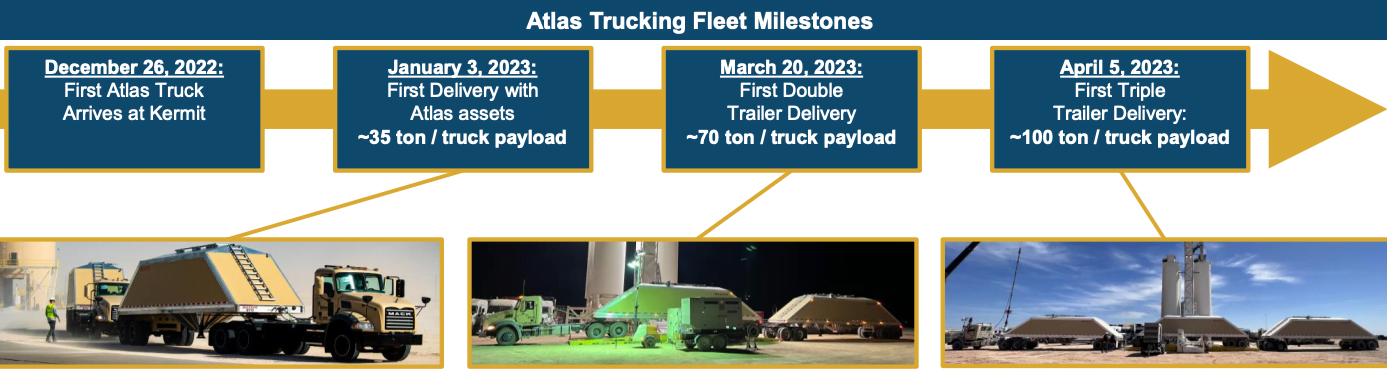

The company’s high margins are the result of their low cost advantage in mining and transporting sand where their cost is nearly half that of their nearest competitor. Atlas achieved this advantage by increasing the payload its trucks can carry and plans to shorten the distance they need to travel by building the Dune Express.

The Dune Express is a 42 mile overland conveyor system that can transport sand continuously from the company’s production facilities to deep into the heart of the Permian basin. When I first heard of the Dune Express, I thought it was a unique science project with all the associated risks of failure if the project did not succeed. It was reassuring to hear that conveyor systems are relatively common in mining facilities across the world. This video on the company’s website does a great job of explaining the project.

I don’t like to invest in science projects, especially ones that burn through capital as they attempt to achieve their goal. Atlas Energy’s current business is already very profitable and the Dune Express is slated for completion in Q4 2024. I asked them about the need to raise additional capital either through a secondary offering or issuing debt. The company indicated that they already have the capital they need to complete the project as a result of the IPO proceeds they received earlier this year.

The company spent 4.5 years to get land right of way and all 42 miles have been cleared for construction. The company has the capacity to transport 11 million tons of sand now and expects that to increase to 15 million tons next year with 40%+ EBITDA margin. Trading at 7 times expected full year 2023 earnings of $2.44 per share, the company is attractively valued now and the Dune Express represents future upside.

The company was founded by Ben “Bud” Brigham, who previously founded multiple upstream energy companies, including two that were acquired by Statoil in 2011 and Diamondback Energy (FANG) in 2016. Given his track record, I would not be surprised if Atlas Energy becomes a future acquisition candidate once its Dune Express is operational.

The key risk I see is production cuts in the Permian basin due to recent oil weakness that will impact both the pricing of future service contracts and the amount of sand needed for fracking.

I am going to initiate a position in AESI in our model portfolio at our full position size and will also be purchasing it for my personal portfolio.