- Subscribe

- Premium

- C-Suite

- Insiders

- M&A

- Gurus

- Spinoffs

- Buybacks

- More

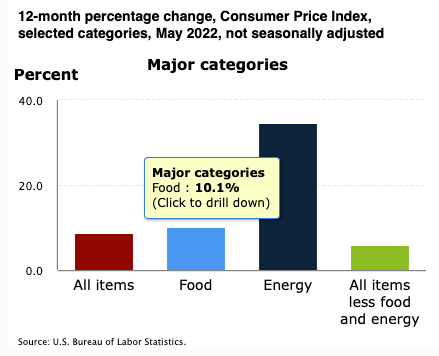

I was in a checkout line at Safeway last week and the person checking out ahead of me was rather taken aback by her grocery bill. She indicated that she did not understand inflation and was not sure if prices will ever come down. This consumer was not the only one surprised. The 8.6% increase in the consumer price index for May 2022 was a big surprise for most economists and investors last week. Food inflation was running even higher at a 10.1% rate. Inflation has gone from “transitionary” to “untamed” and the market broadly expects the Fed to increase its benchmark funds interest rate by 75 basis points instead of the 50 basis point increase that was expected last week.

I was in a checkout line at Safeway last week and the person checking out ahead of me was rather taken aback by her grocery bill. She indicated that she did not understand inflation and was not sure if prices will ever come down. This consumer was not the only one surprised. The 8.6% increase in the consumer price index for May 2022 was a big surprise for most economists and investors last week. Food inflation was running even higher at a 10.1% rate. Inflation has gone from “transitionary” to “untamed” and the market broadly expects the Fed to increase its benchmark funds interest rate by 75 basis points instead of the 50 basis point increase that was expected last week.

We are currently in a challenging macro environment with 30 year fixed mortgage rates nearly doubling in just the span of a few months to 6%, the nationwide average for gas has eclipsed $5 per gallon and cryptocurrencies are imploding at a rapid pace. Buyer’s remorse, potential financing issues or liquidations of certain institutional portfolios is also impacting merger arbitrage spreads, which have widened significantly over the last week. There are 15 active all cash deals with annualized spreads above 30%. I will be writing more about these wide spreads and a three part plan of action to tackle this bear market in our mid-month update tomorrow.

This environment reminded me of a debate I have often seen between investors that either prefer top down or bottoms up analysis. Bottoms Up is a Nickelback song, the name of a bar in San Francisco and an approach investors use to focus on the specifics of a company they are analyzing. Investors favoring this approach are on the lookout for companies that meet their investment criteria, which can include everything from calculating the intrinsic value of the company, analyzing management’s capital allocation track record (were they buying back stock and issuing stock at the right times), understanding potential future growth opportunities and reviewing how the company is positioned compared to peers.

Some bottoms up investors prefer to focus almost exclusively on the company and figure that the macro environment will take care of itself. Implicit in this approach might be the understanding that management will be smart enough to pick up on the prevailing industry winds, anticipate macro issues and tackle them as they arise. We have seen this in action with Southwest Airlines (LUV), which had an excellent oil hedging program that helped the company more than a decade ago when oil prices were even higher than they are right now. A more recent example was retailers like Costco (COST) and Walmart (WMT) chartering their own ships to address logistics issues related to certain ports of entry on the West Coast of the United States.

In contrast, macro investors prefer to swim with the current and like to identify favorable macro tailwinds to pick countries, sectors or industries they want to invest in and then dive deeper to find excellent companies within that sector. They probably don’t have quite the same level of confidence in management’s ability to see the big picture. Having closely followed insider buying every week for more than 12 years, I can agree with the macro investors that a large number of management teams are myopically focused on their companies and often miss signals that the cycle is turning. CEOs like Lisa Su of AMD, Gina Drosos of Signet Jewelers (SIG) and Tim Cook of Apple (AAPL) are few and far in-between.

Investors that decide to pick individual stocks or participate in special situations have their work cut out for them. While the process can be intellectually stimulating, it can also be exhausting. Idea generation, pattern matching, financial analysis/modeling, figuring out management incentives, applying lessons from prior mistakes, understanding the competitive landscape and figuring out position sizing within the portfolio takes time. Add to that the fact that you are likely to reject the vast majority of investments you analyze. Sure, there are some shortcuts and a well established process helps build intuition that brings down the time required to analyze investments. After doing all of this, the time and the ability to understand the macro environment might be limited.

Having been an industry tourist in the past and seeing how much it hurt my investment outcomes, I resolved to pay special attention to industry headwinds or tailwinds, understand cycles and focus on macro factors. Investors would be better served not to pick a “top down” or “bottoms up” camp but take a holistic 360 degree approach to their investments that spans both disciplines. Luck is a huge factor in both life and investment outcomes but improving/expanding our process can hopefully shift the odds in our favor. Best of luck to all ye brave souls that have decided to pick individual stocks in rough seas.