- Subscribe

- Premium

- C-Suite

- Insiders

- M&A

- Gurus

- Spinoffs

- Buybacks

- More

During Berkshire Hathaway’s annual meeting last week, Warren Buffett went into a lot of detail about his position in Activision Blizzard (ATVI) to capture the arbitrage spread on the deal. This position was distinct from the position one of his managers, Ted Weschler and Todd Combs, had started before the $95 per share all cash deal with Microsoft (MSFT) was announced on January 18, 2022. Incidentally Barry Diller, his step-son Alexander von Furstenberg and David Geffen also had started a position in Activision Blizzard (ATVI) through an options trade before the deal was announced. The timing of their trade caused JPMorgan Chase to report the trade to law enforcement and it is currently being investigated. Mr. Diller denied the accusations and indicated that it was just a lucky bet.

Berkshire Hathaway’s purchases of Activision Blizzard before the deal was announced were also the subject of a WSJ article and Buffett wrote this letter to various news outlets to clarify that the position was started long before the acquisition was announced and at prices that could be replicated after the announcement.

Subsequent to the position that one of Berkshire Hathaway managers started in Activision, Warren Buffett also decided to buy Activision for the arbitrage spread, which was approaching nearly 20%. If you are not familiar with the strategy, we did a primer on it though Twitter threads last week here, here and here, and also wrote an introduction to merger arbitrage article several years ago. Warren Buffett and Charlie Munger have been doing merger arbitrage, or “workouts” as they used to call it, for over fifty years. In Alice Schroeder’s book The Snowball: Warren Buffett and the Business of Life, she details a arbitrage trade where Charlie Munger put all his investment partnership’s money, all his own money and everything he could borrow into a single arbitrage trade where the Canadian government was buying British Columbia Power for a little more than $22 per share and the stock was trading around $19.

Given Berkshire Hathaway’s size, they can only meaningfully participate in very large deals such as Bayer’s acquisition of Monsanto and IBM’s acquisition of Red Hat. The Monsanto deal was particularly hairy as it required approvals from all the BRIC countries (Brazil, Russia, India and China), the European Union, CFIUS and the U.S. DOJ. The entire deal took the better part of two years to complete and Bayer had to sell Monsanto’s digital farming business and part of its Crop Science unit to German chemical company BASF to get regulatory approval. I was personally long both Monsanto and Red Hat for the arbitrage spread and was also long LinkedIn when Microsoft’s acquisition of LinkedIn was trading at a large spread.

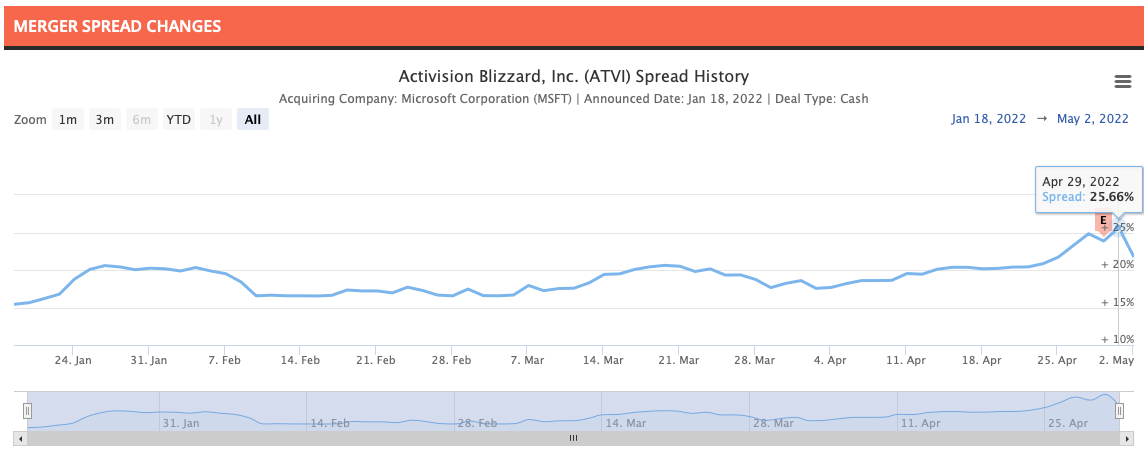

The Activision deal has similar characteristics where it is a large tech merger and is subject to regulatory approval by the United States and several countries. The spread on the deal had eclipsed 25% last Friday before news about Buffett’s arbitrage play made the rounds and Activision’s stock rebounded this week. You can see the spread history of the deal below.

We wrote the following about the deal in our Merger Arbitrage Mondays article after the deal was announced,

The deal is priced at $95 per share in cash, representing a premium of over 45% to Activision’s closing price before the deal was announced. Activision’s stock had taken a big hit in recent months after allegations of workplace harassment resulted in employee walkouts and several resignations. This deal with Microsoft is as much about fixing the culture at the company as it is about allowing Microsoft to strengthen its gaming presence and enter the metaverse with strong franchises. The deal is subject to clearance from antitrust regulators in the US, Europe and China. The termination fee of $3 billion is likely to compel all parties to get this deal completed.

The deal is currently trading at an unusually large 16.78% spread or 14.18% annualized assuming it closes by March 31, 2023. The large spread represents the market’s skepticism about regulators allowing this deal to close or delaying the closing. There could be some interesting ways to play this situation by using long dated options and I plan to write about it in our next premium newsletter.

The more I looked into the deal, the less I was excited by it despite the large spread, which kept increasing. Instead of highlighting the Activision deal for premium subscribers I wrote about three other arbitrage opportunities in our March 2022 mid-month update. Buffett and Munger have been doing arbitrage long before I started using the strategy 12 years ago and their assessment of the probability of the deal going through is likely better than mine. However we are not constrained by the same size issues that Berkshire Hathaway faces and there are plenty of other arbitrage deals out there with better risk/reward characteristics. If the deal does go through, I would benefit indirectly through my long position in Berkshire Hathaway. Should the deal fail and Activision stock were to drop as arbitrageurs exit the trade, I would be very interested in taking a fresh look at Activision as an investment.

You can check out the deal metrics for the Activision deal here and can watch Buffett explain his position here.