Onsemi Goes All-In on Physical AI With Synaptics Deal – Merger Arbitrage Mondays

Synaptics Incorporated (SYNA): $121 Market Cap: $4.68B Deal Value: $7B

Read MoreInside Arbitrage is an idea discovery platform. We provide institutional quality investment tools and research to investors that focus on specific events. These events could be transformative events such as one company merging with another or a simple one such as a company insider purchasing the company's stock on the open market. Inside Arbitrage provides up to date information for various event-driven or special situations strategies like merger arbitrage, spinoffs, legal insider transactions, stock buybacks and SPACs. We also track management transitions and the portfolios of investment gurus through their 13F filings.

Event-driven or Special Situations funds invest in one or more strategies including but not limited to risk arbitrage, spinoffs, special purpose acquisition vehicles (SPACs), warrants, bankruptcies, etc. We have identified a curated list of funds that are either dedicated to these strategies or use them for a portion of their portfolio.

It is sometimes difficult to classify a fund under one investing style and in those cases, we may have the same fund listed under two or more categories. Investing styles also evolve over time and a fund that was event-driven focused may decide to adopt a different strategy.

We reviewed the fund websites, looked at SEC filings and reviewed the holdings of these funds to classify them into one or more categories but you can draw your own conclusion by clicking on the name of a fund to pull up their portfolio as of their last 13F filing.

Beyond the 13F filings, we have also incorporated 13G and 13D filings as well as form 4 insider filings. Funds are required to file a 13D or a 13G within 10 business days of acquiring a 5% position in a company. Funds are considered an insider if they own more than 10% of a company and are required to file a form 4 within two business days after a transaction.

For each fund, we have included new additions, stake increases, stake reductions and the complete sale of a position in separate tabs. You can also click on the "View All

If you have suggestions for additional funds we should track, we would love to hear from you.

A fund that acquires a 5% position in a company and that plans to influence the management or the direction of a company is requited to file a 13D with the SEC. The 13G filing is required for a 5% owner if they plan to remain passive.

Activist funds could be hostile to management with plans to get their own candidates elected to the Board of Directors or firms that collaborate with management to effect change. Good examples of the former are Elliott Investment Management and Carl Icahn, while good examples of the latter are Starboard Value and Third Point.

Activist funds play an important role in financial markets by effecting necessary change and investors follow activist positions with a lot of interest.

Value is in the eye of the beholder and a company that trades at a premium multiple to the average P/E of the S&P 500 could be considered a value stock if its margins are high and the investor believes its future prospects are significantly better than the market is anticipating.

Other value investors might focus on companies that are trading at low multiples by looking at their favorite comparative valution metrics like price/earnings (P/E), price/tangible book, EV/EBITDA or Price/FCF. A third group might prefer building detailed financial models and then running discounted cash flow analysis using bull case, base case and bear case scenarios.

Value traps are their nemesis and many of these investors pay a heavy price battling this nemesis before they start to identify them from a long distance and steer clear.

My favorite kind of investors. A company is like a living organism that is either growing or on its path to oblivion. These folks don't mind paying up a little if they can find a growth stock that is temporarily being discounted on account of an adverse event or an earnings miss.

Stocks that were formerly in the growth camp, might be temporarily in the growth at a reasonable price (GARP) camp on their way to value territory. These are best avoided if you can identify them in advance, which is no small feat.

These investors are drawn to rapidly growing companies. A mistake in valuing a company can be easily forgiven if the company continues to grow rapidly. Investors with a growth focus are willing to suffer a few quarters or years of bottom line losses to realize an eventual payoff. Think the "Tiger Cubs" of the investing world.

Volatility is a feature of this style of investing and not a bug. Broadly diversified portfolios could help smooth the roller coaster ride but we have seen highly concentrated growth portfolios.

These are funds that are difficult to pin down to a specific style or belong to categories we have decided not to separate out into their own group. You will find your quantitative funds with thousands of positions (D. E. Shaw and Renaissance Technologies for example), the healthcare focused funds (Baker Bros. Advisors and Orbimed Advisors), the energy focused funds (Alps Advisors and Chicasaw Capital) as well as famous hedge fund managers that now run family offices (Soros, Paulson and Druckenmiller to name a few).

Synaptics Incorporated (SYNA): $121 Market Cap: $4.68B Deal Value: $7B

Read More

I’ve been a loyal Expedia user for more than two

Read More

The Perceived Disrupted Last month, I wrote about how the

Read More

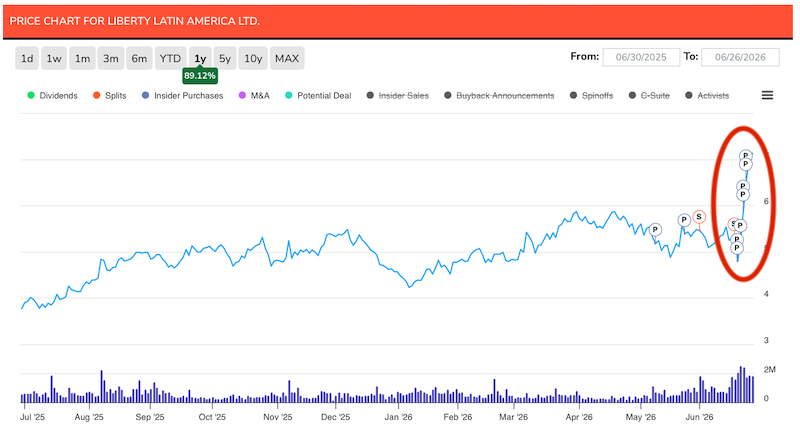

Liberty Latin America Series A Preferred Shares (LILAP): $20.37 Type:

Read More

This mid-month update is a little late as I was

Read More

I was at the Planet MicroCap conference in Las Vegas

Read More

CEO succession is often the toughest test for any company.

Read More

It’s a wrap! We created the Friday Wrap in April

Read More