- Subscribe

- Premium

- C-Suite

- Insiders

- M&A

- Gurus

- Spinoffs

- Buybacks

- More

It has been over 14 years since Marc Andreessen, the founder of both Netscape and the premier VC firm Andreessen Horowitz, wrote the article Why Software Is Eating The World for the Wall Street Journal. That article, timed just after the Great Recession ended, kicked off one of the biggest bull markets of the last century, resulting in gains of over 900% for the NASDAQ.

Investors have been starting to write the obituaries of software companies over the last few weeks and that activity hit fever pitch this week when multiple SaaS companies saw their stocks drop double digits. The carnage on Tuesday looked like wholesale capitulation by investors who had watched software company stocks decline for the better part of the year.

The prevailing perception is that AI will eat the world and software companies are particularly susceptible to disruption. The irony is that the carnage in software companies on Tuesday, caused collateral damage in AI and AI adjacent companies on Wednesday, many of which, like Palantir (PLTR), Nebius (NBIS) and Micron (MU), saw double digit declines in their stock prices.

Is Software Really Dead?

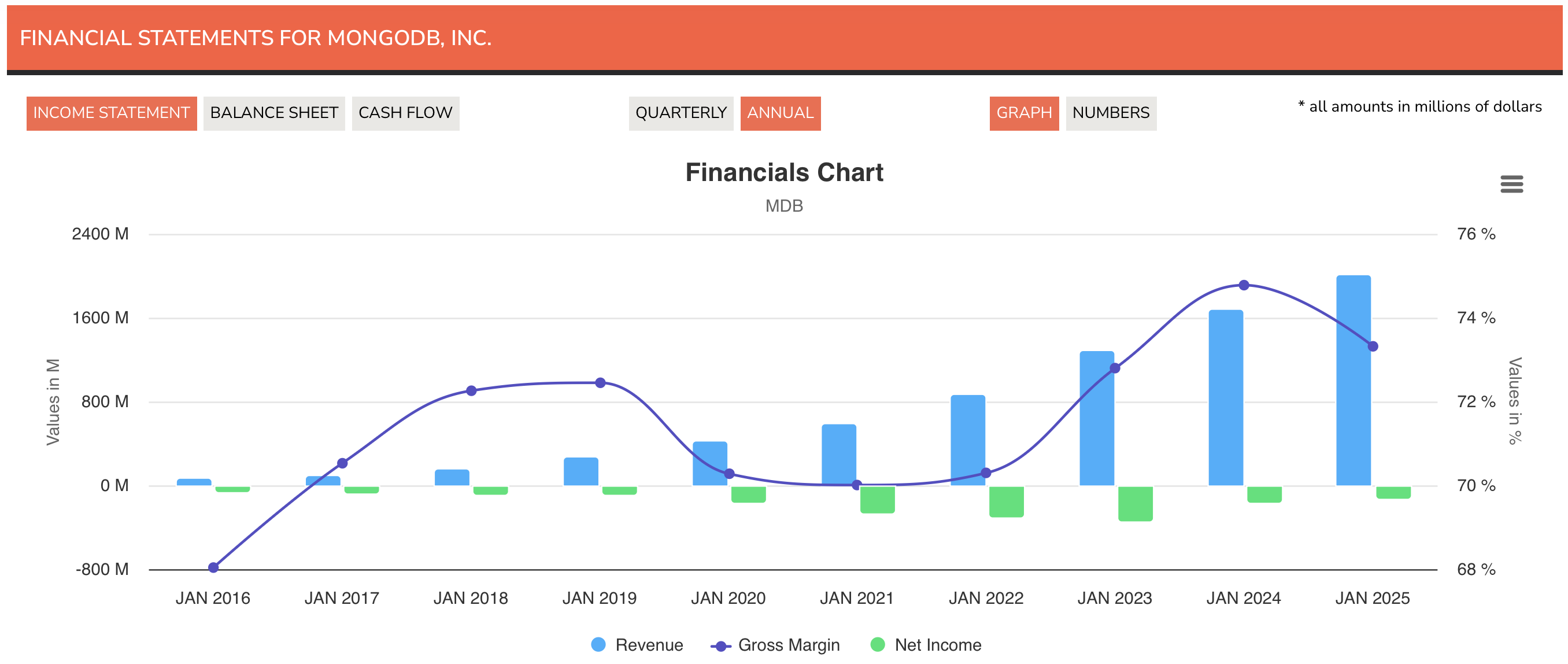

The fallacy of software getting replaced by some vibe coded app using Claude Code reminds me of claims from just a few years ago that the blockchain was going to replace databases and data warehousing. Folks making these claims clearly didn’t understand databases. The growth companies like MongoDB (MDB), Snowflake (SNOW) or Databricks have experienced over the last few years illustrates just how misguided those claims were.

Beyond cryptocurrencies, blockchain had some real use cases and I felt like it was the perfect technology to disrupt something like title insurance, a service every home buyer reluctantly pays for as part of their closing costs. If you check out the financials or stock price chart of Fidelity National Financial (FNF), one of the largest title insurers in the U.S., you will see that blockchain had no impact on its business.

Transformation and Phase Changes

In our February Special Situations newsletter where we covered a software company that was seeing unusual insider buying activity, I wrote the following:

“Electrification, the industrial revolution and the internet all led to phase changes that significantly impacted humanity and often in positive ways. Yes, they also caused disruption and new winners emerged as old companies that couldn’t harness innovation rapidly withered. We also saw some of the old guard reinvent themselves to not just survive but thrive in a new world. General Electric (GE) went from a light bulb company to a jet engine manufacturer and Microsoft (MSFT) managed a successful transformation from shrink-wrapped software company to a cloud services provider. Nintendo (NTDOY), which started as a playing cards company in the nineteenth century is now an integrated video gaming company.

These transitions were not easy and some of these companies suffered years of underperformance: GE under Jeff Immelt, Microsoft under Steve Ballmer and IBM under Ginni Rometty come to mind.”

The emergence of LLM-powered AI, which I see as being distinctly different from the old machine learning era that preceded it, is causing another phase change. The winners have been the picks and shovels companies including GPU providers like NVIDIA (NVDA), memory providers like Micron (MU) and countless power-adjacent companies that work with data centers. The second wave of companies that will benefit from AI like drug development companies, CROs and AI native software companies are just starting to emerge.

In this environment, investors are shooting first and asking questions later. The subjects of their target practice have been software companies.”

Perception vs. Reality

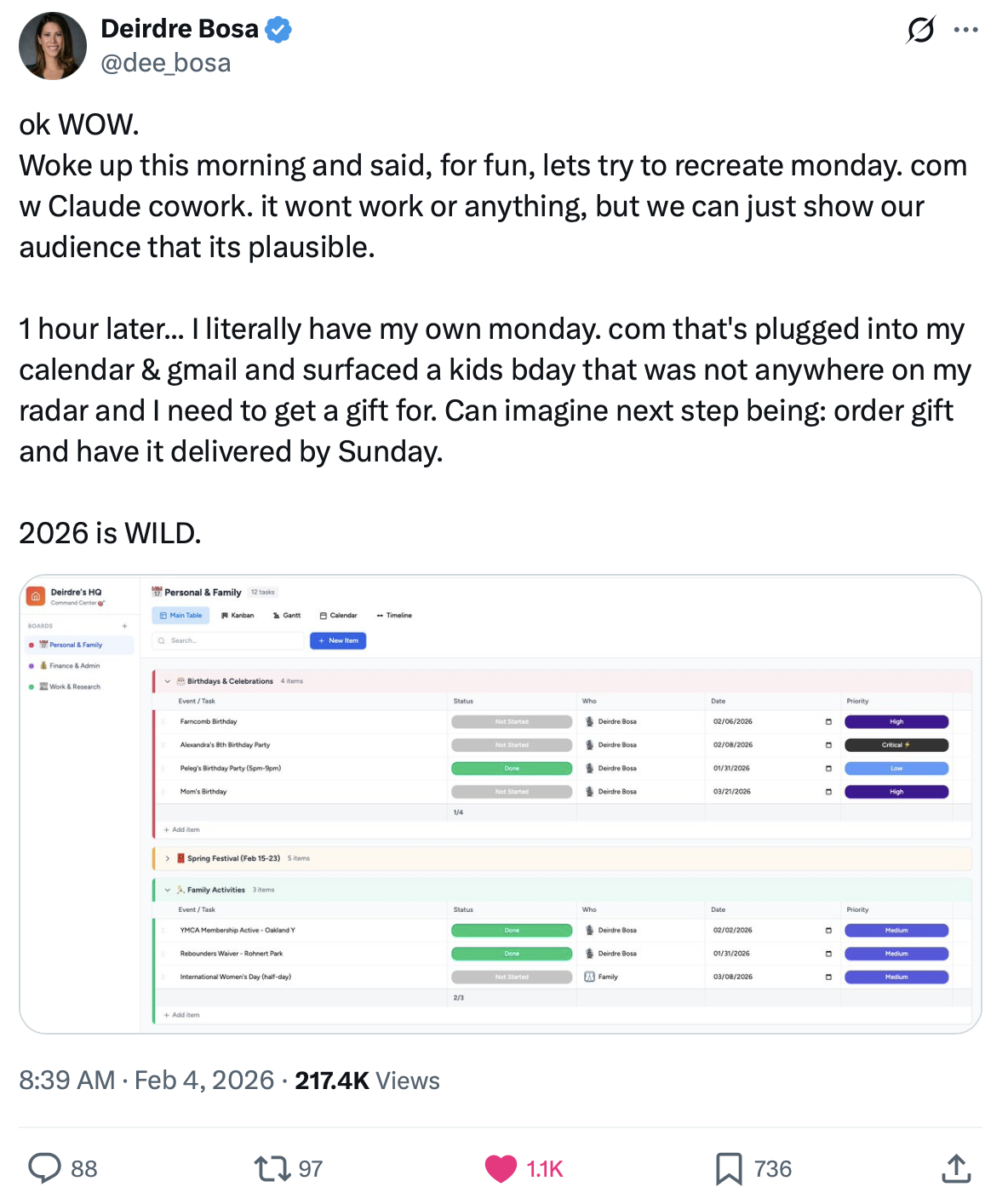

Whether it is coding copilots or the release of Claude Code, there is no denying that AI is significantly improving the ability to create code and even build applications. However, there is an ocean of difference between enterprise software built by companies like Workday (WDAY) and a single productivity related vibe coded app that CNBC anchor Deirdre Bosa created.

The software industry is large and nuanced:

The software industry is large and nuanced:

I have barely scratched the surface with this list and it mostly includes large public companies.

While it might be possible to disrupt some of these companies, especially the ones focused on productivity or CRM, the rest are successful not just because they created some code and built a few features.

This reminds me of software engineers who looked at the features of Facebook and Twitter in their infancy and felt that they could easily recreate it. What they didn’t understand is that Facebook and Twitter worked because of network effects and the work that was done to scale those platforms (anyone remember the Twitter fail whale?) not simply because of code that was written to string together a few features.

Overnight Success

To elaborate on what it actually takes to build a successful business of any kind, software or otherwise, I also wrote the following in our February newsletter:

“Starting a new company and building a sustainable business is excruciatingly difficult. In many ways, if those starting businesses for the first time were not naive about the challenges they will face, they will likely not do it. A book that helped me when I was going through my own journey with a startup was Ben Horowitz’s The Hard Thing About Hard Things. Jessica Rees reviewed the book for InsideArbitrage in 2024 and Ben Horowitz liked her review.

I have recommended the book to many people including the CEO of a startup that was going through a difficult patch and that eventually had a successful exit. The interesting thing about success is that people mostly see the “overnight” success and not the years of work that went into getting to that success. This is similar to the 10,000-hour rule that Malcolm Gladwell mentions in his book Outliers, where he details numerous instances of people achieving world-class mastery of a subject after spending over 10,000 hours on deliberate practice.

I have noticed something similar with software companies and especially large enterprise software companies. By the time they hit their stride after years of figuring out product-market fit, customer acquisition costs, a scalable business model, customer retention, etc., more than a decade has often elapsed. Employees and investors that get involved more than a decade later often benefit from the compounding engine the founders and early employees of the business put into motion.”

While this AI revolution is unfolding around us, established software companies are not sitting still. Software companies will evolve. Current SaaS companies are not running on software designed for punch cards. When I first started web programming, I used Perl/CGI but by the time I built an enterprise software solution in the 2000s, I used a completely different set of technologies.

Workday has gone on an acquisition binge acquiring multiple AI native companies including Sana for AI-based search, Pipedream for AI agent development, Evisort for AI enabled document intelligence and more. Other software companies have utilized AI across their development organization ranging from faster code development to enhanced QA automation.

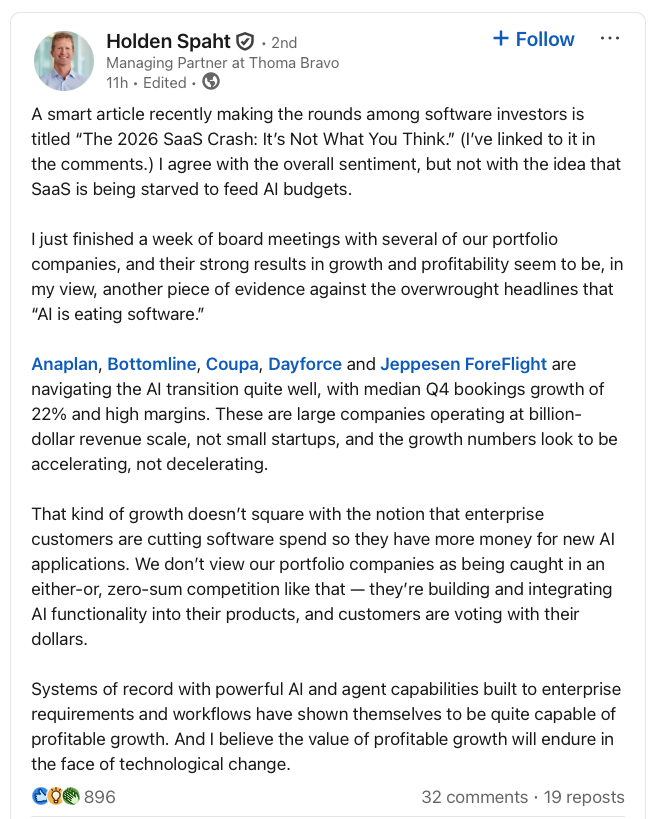

You don’t have to take my word for it. Over the 15 years we have tracked M&A activity on InsideArbitrage, we have seen nearly three dozen software public companies taken private by the large private equity firm Thoma Bravo. This is what Holden Spaht, a managing Partner at Thoma Bravo had to say about their portfolio companies:

The Software Nuclear Winter

Biotech stocks experienced a deep nuclear winter that started in early 2021 and went on for nearly four years before the industry started to thaw in 2025. The current situation with software companies is reminiscent of the biotech nuclear winter where many real companies with FDA approved drugs were thrown out with the bathwater of “science projects” companies that were cash incinerators.

Before you go fishing in the software carnage for opportunities, it is important to keep in mind that for years investors were willing to accept outrageous valuations, incomprehensible stock-based compensation plans and adjusted EBITDA mumbo-jumbo to participate in high margin growth companies. The hope or the misconception was that on a long enough timeline these companies will generate real profits (of the GAAP kind) and shareholders will be rewarded.

The foundation on which that hope rested has been shaken and while there are no real cracks, the earthquake of AI was sufficient to create a phase change in perception. The new perception, which is just as misguided as the earlier enthusiasm, is that these software companies will die an untimely death at the hands of AI.

Terminal Value and Conclusion

In late 2021, analysts following high growth companies had to suddenly adjust their models to incorporate a new world where inflation was no longer transitory and we were looking at the end of the zero interest rate era. When playing with valuation models for various high growth companies in the fourth quarter of 2021, I was struck by just how much their valuations dropped if I increased the interest rate in those models up by just one or two percent. I firmly believed that inflation was not transitory and this meant that tech company valuations would drop and their stocks would take a hit. I adjusted my portfolio to reflect this view.

The ensuing carnage allowed me to buy companies like Meta (META) and Netflix (NFLX) that had long been on my watchlist.

Valuation models like discounted cash flow analysis (DCF) models contain two key components. One part determines the future cash flows the company will generate over the next few years (5 years or 10 years) and the second part is the terminal value, which assumes that the company will grow forever at the rate of inflation.

While this terminal value part could be true for companies like Johnson & Johnson (JNJ) or Nestlé, tech companies get disrupted all the time. The terminal value that analysts are assigning to software companies in their valuation models is greatly diminished now and this translates to much lower stock prices.

The wide chasm between perception and reality is where serious money is made and I believe the current dislocation will once again yield opportunities like the 2022 drop in tech stocks did. I think we are very early in this adjustment process and patience will be required as stocks hit new lows. The flip side of patience is that market participants have been trained to “buy the dip” over the last decade. Most events, like the sudden strengthening of the Japanese Yen in mid-2024 or the tariff fears of early 2025, only led to short periods of pain in the markets before they rebounded.

I am not sure if this time is different in terms of the duration of this downturn but I have my watchlist ready and will be going shopping in the next few weeks and months.

Voluntary Disclosure: I hold long positions in Meta (META), Netflix (NFLX), Lyft (LYFT), Workday (WDAY), Palantir (PLTR), Nebius (NBIS) and Micron (MU).

Disclaimer: Please do your own due diligence before buying or selling any securities mentioned in this article. We do not warrant the completeness or accuracy of the content or data provided in this article.