Sixty Companies, A Two Day Conference And Ten That Made The Cut

The first part of this article is an excerpt from our September special situations newsletter and the second part briefly touches upon five additional companies that I found interesting for further research.

Last week I spent a few days in Chicago attending the Midwest Ideas conference, one of three wonderful conferences Three Part Advisors holds each year. This was my first time in Chicago and I absolutely loved the city. I fully understand that winters can be brutal in the Windy City and that I saw no more than a tiny sliver of the city but it is beautiful and the river walk area was excellent for taking a long walk after the conference. I really enjoyed meeting some old friends at the conference and made some new ones.

Last week I spent a few days in Chicago attending the Midwest Ideas conference, one of three wonderful conferences Three Part Advisors holds each year. This was my first time in Chicago and I absolutely loved the city. I fully understand that winters can be brutal in the Windy City and that I saw no more than a tiny sliver of the city but it is beautiful and the river walk area was excellent for taking a long walk after the conference. I really enjoyed meeting some old friends at the conference and made some new ones.

Last year, I attended the conference in Dallas and eventually added Atlas Energy Solutions (AESI) and the Jefferies spinoff Vitesse Energy (VTS) to our model portfolio and my personal portfolio. Both companies went on to generate double-digit returns for the portfolio without taking into account their sizable dividends.

This year, nearly 60 small and micro-cap companies presented at the conference. Since they hold three presentations simultaneously, I can only attend a maximum of 20 presentations and participate in the QA sessions that follow the presentations. To narrow the list of companies I want to check out, I usually create a spreadsheet looking at 21 metrics, including growth, management effectiveness, balance sheet strength, valuation, etc.

For the companies that pass my quantitative filter, I then dig deeper before and during the presentation.

Conversations with fund managers and other attendees during and after the presentations help surface any interesting companies that didn’t look good based on the numbers but were potentially at an inflection point.

The ten companies from the conference that really stood out to me were:

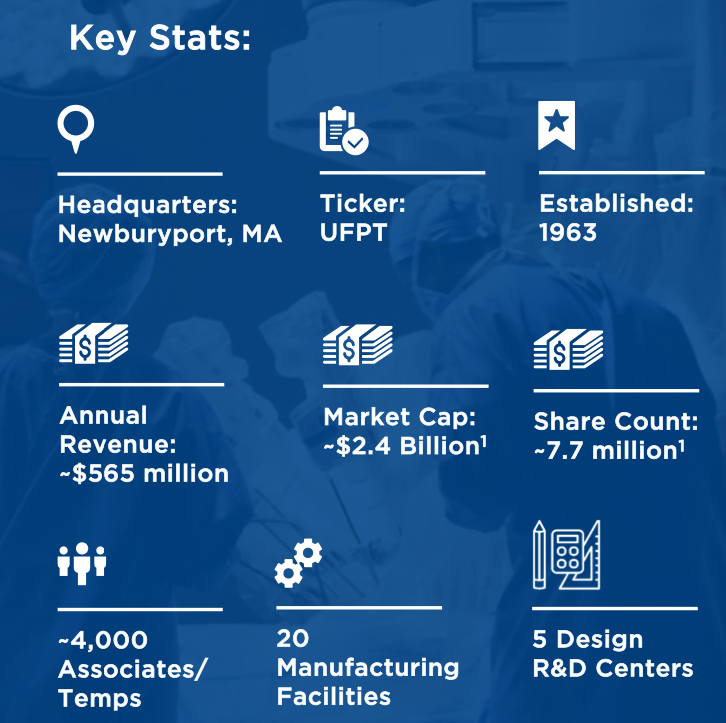

- UFP Technologies (UFPT): An advanced components and medical devices company that has a rapidly growing robotic surgery program and counts Intuitive Surgical (ISRG) as an early customer. The fact that the company’s current growth is directly the result of a couple of strategic acquisitions in 2018 and 2022 and the rich valuation (trading at 47 times cash flow) are giving me pause.

- Select Water Solutions (WTTR): An oil services company that is led by a founder CEO. The company stores, delivers and recycles water used in fracking. The investment thesis is very similar to Atlas Energy, which delivers sand, and both companies have a board member in common. While Select Water trades at an attractive valuation, I find Atlas Energy to be more innovative with its “Dune Express” project and didn’t want double the exposure to fracking in the Permian Basin.

- Powell Industries (POWL): A 75 year old company that is an expert in electric distribution and acquired GE’s circuit breaker division in 2010. The company is firing on all cylinders with very strong growth due to demand from data centers, industrial companies, etc. Strong revenue growth, net cash on the balance sheet, a big EPS beat last quarter, decent margin and low/moderate valuation make for a heady mix. The key concern is that this is a cyclical business and while we might not be near the top of the cycle just yet, we will eventually see mean reversion following a near doubling in the stock price over the last year and a 370% jump in the last five years. Insiders who were buyers a year or two ago are now sellers.

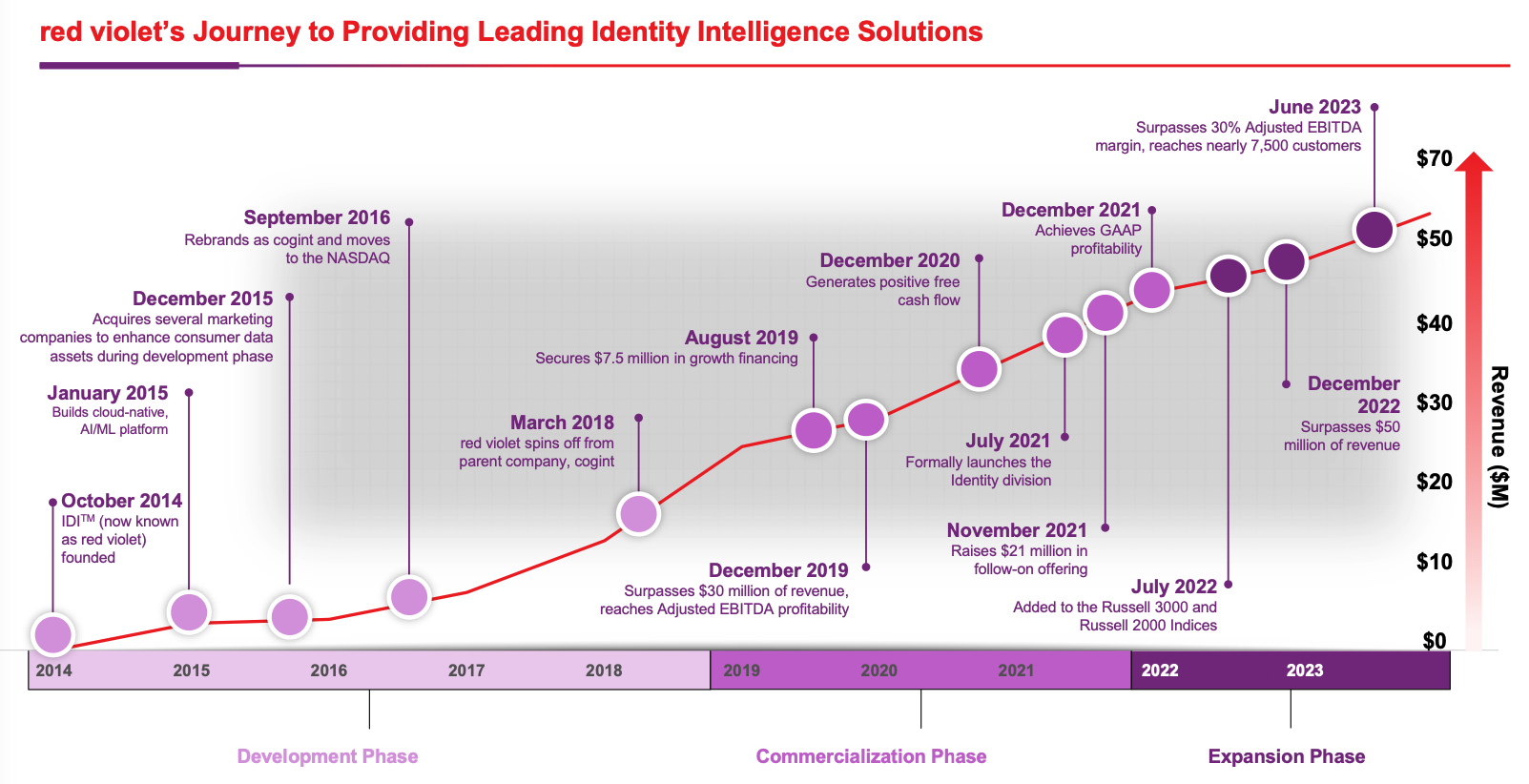

- Red Violet (RDVT): A SaaS company focused on identity management solutions that is growing both the top and bottom lines rapidly and appears poised to benefit from a new focus on large enterprises and the public sector compared to its SME bread and butter. This is one of two spotlight ideas we discussed in more detail in the September special situations newsletter.

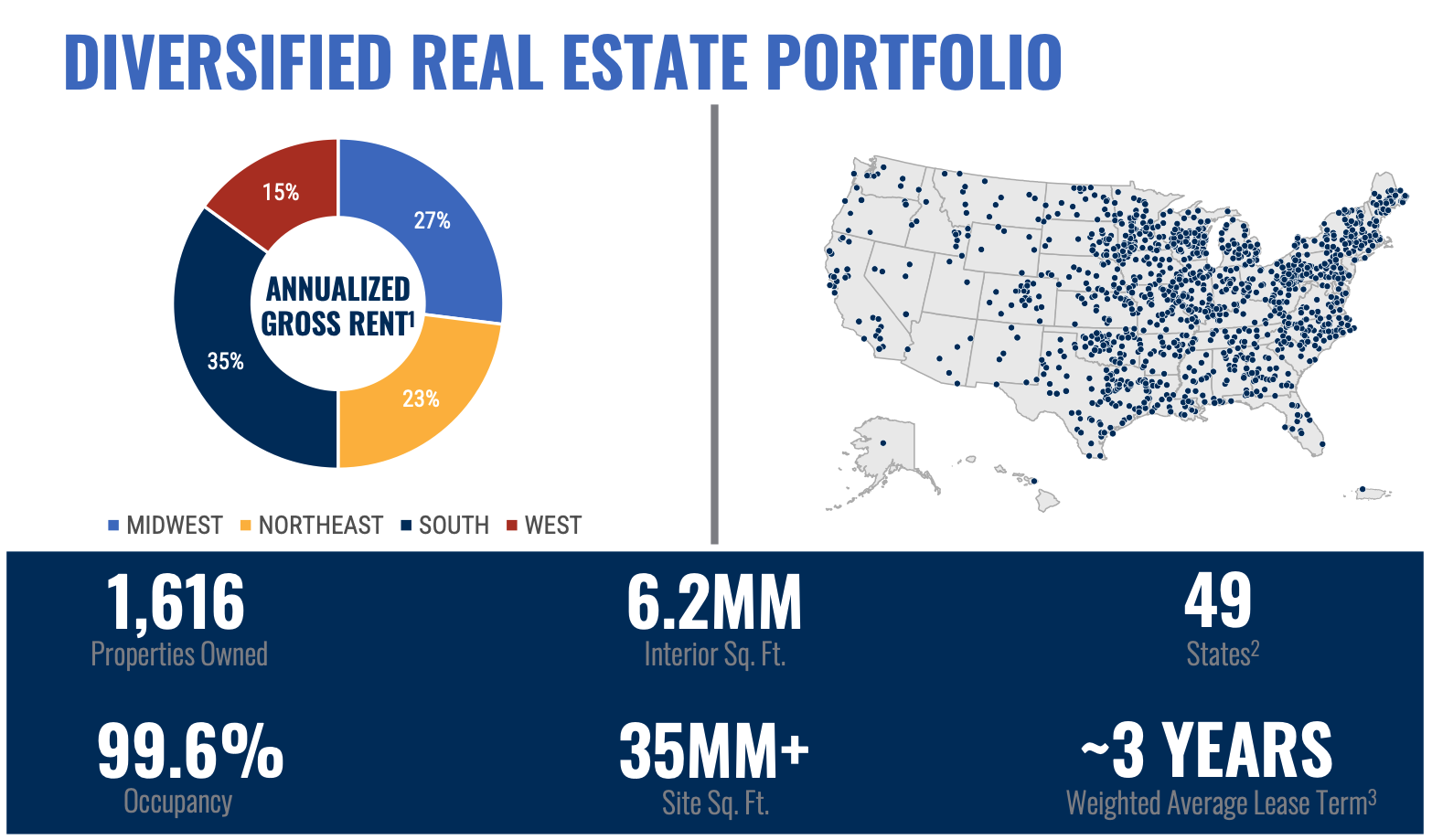

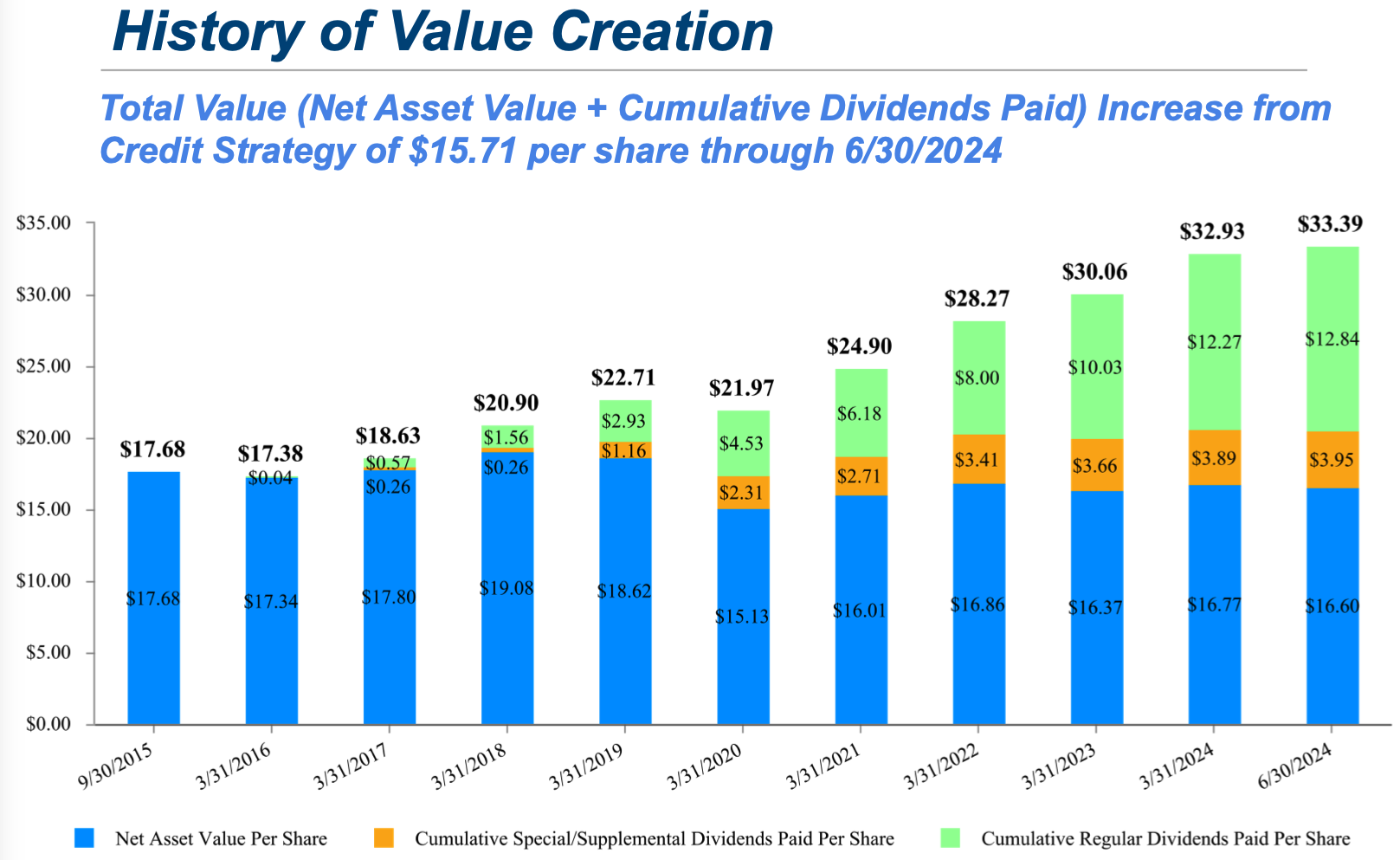

- Postal Realty Trust (PSTL): A unique REIT with a 6.63% yield that leases properties to the U.S. Postal Service and enjoys a 99% occupancy rate. We discussed the company in an insider weekends article following insider purchases by the CEO a few months ago and it was good to meet him at the conference. This is the other spotlight idea we discussed in the newsletter.

- Miller Industries (MLR): The largest manufacturer of towing and recovery equipment in the U.S., U.K. and France that exports its products to 60 companies worldwide. As of last week, the stock was up 52% this year and 100% last five years. Industry drivers are miles driven and age of vehicles. We are seeing an increase in age of vehicles on the road. Natural disasters also create a need to recover vehicles. Last year the company surpassed $1 billon in revenue for the first time. The company is “Debt averse” and carries very little net debt on its balance sheet. Chassis sales are low margin, which is dragging down overall gross margin. Low gross margin and growth are key concerns. P/E at a ten year low.

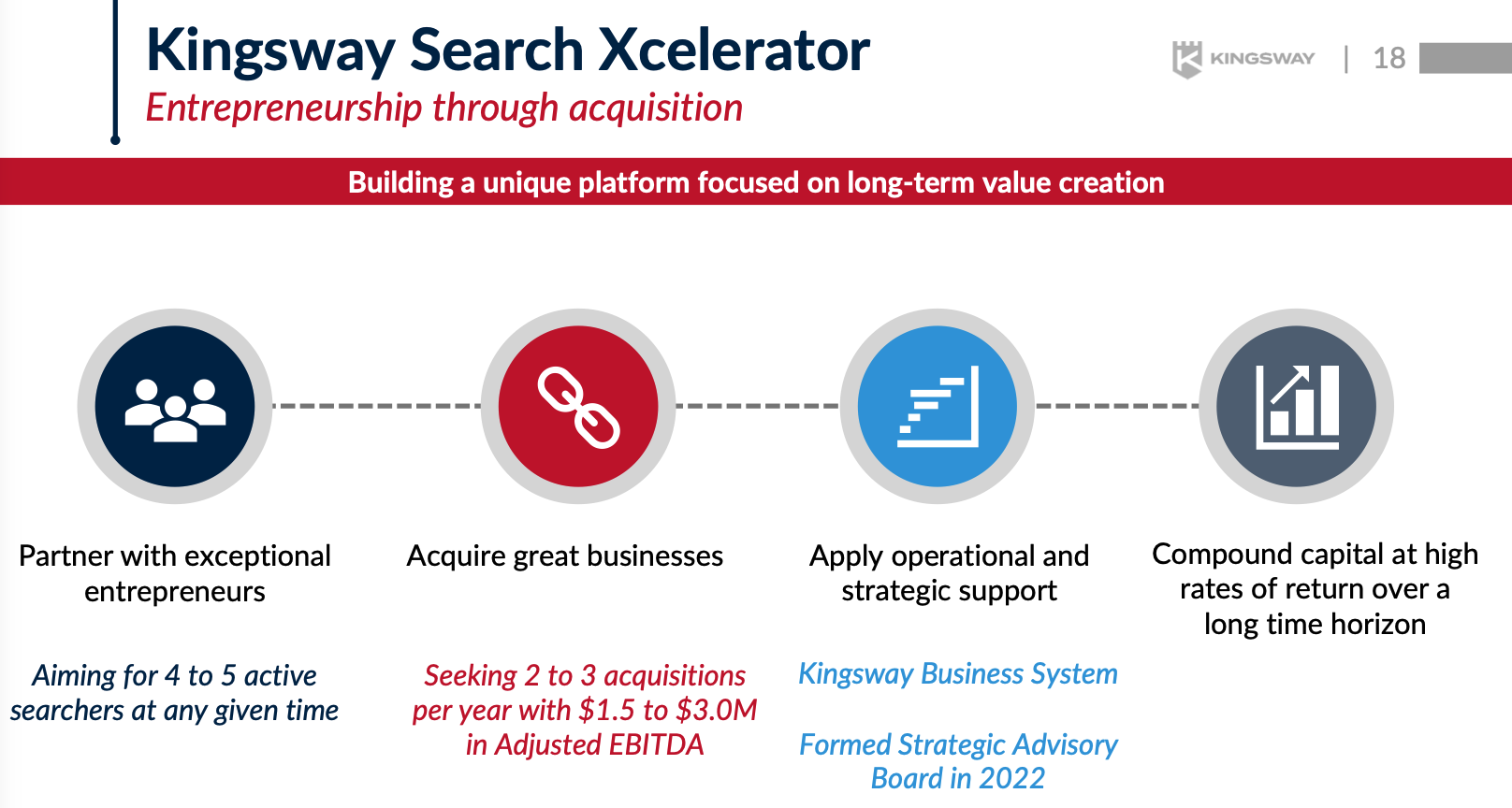

- Kingsway Financial Services (KFS): A small holding company with just 10 employees at the holding company level. 66% of revenue is extended warranty and 34% is Kingsway Search Xcelerator (also known as a search fund and sounds something like a mini-SPAC). Average return of search funds is 35% per year based on some studies. They got hit by claims inflation because of rising labor cost on the extended warranty side. Not an insurance company but policies have to be backed by an insurance company. Negative working capital as they collect 3 year of premium upfront. The extended warranty product is offered primarily through credit unions. Average customer relationship is 12 years, longest is 20 years. Untapped market in HVAC and plumbing. Invests float in bonds, which should yield better returns going forward as old bonds with 2 to 3 year maturities roll over. Interestingly Joseph Stillwell is a large shareholder and I discussed his style of activism in an article titled Stilwell Value – An Activist Fund With A Focus On Banks a couple of years ago.

- Capital Southwest Corp (CSWC): I normally don’t invest in Business Development Companies (BDCs) but this was one was interesting. They partner with private equity firms to lend to their portfolio companies with top of the capital stack lending (first lien). On the debt side of their balance sheet they have two loans due 2026 at low rates that need to be refinanced and will impact earnings. They have been issuing shares to raise capital consistently. Trades above book compared to other BDCs. Times of overall market distress impact BDCs disproportionately due to the nature of their business and I plan to keep this one on the watchlist to see how it weathers the next storm.

- Hamilton Beach Brands Holdings (HBB): The #1 small appliance brand. Proctor Silex is one of their high trust brands. Commercial relationships with companies like Costa Coffee, McDonalds, Norwegian Cruise, etc. Commercial sales are currently only 8% of revenue right now. HBB licenses premium brands like Wolf. They are buying back stock but I don’t see this reflected in a decline in shares outstanding. The company trades for less than 6 times TTM free cash flow of $65 million but over the next two years FCF will normalize to $25 to $30 million per year.

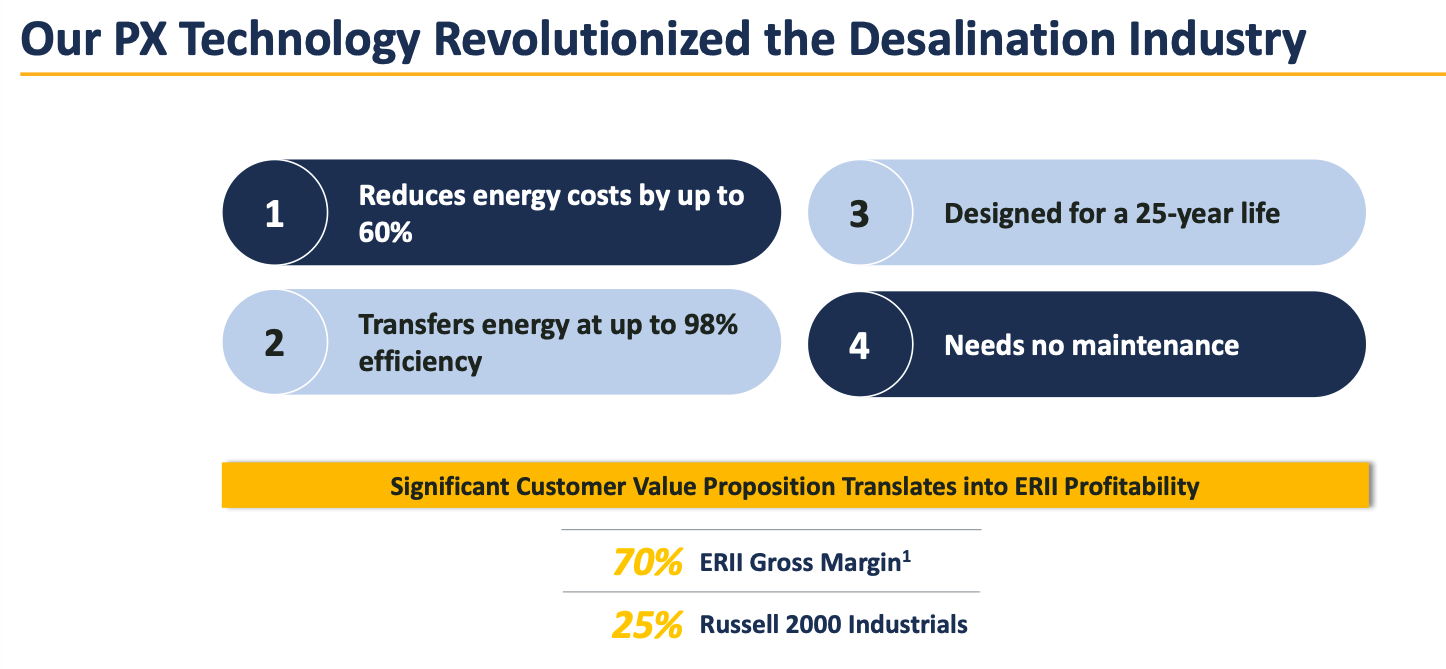

- Energy Recovery (ERII): A company I found absolutely fascinating when I attend the Dallas conference and was looking forward to an update in Chicago. Energy Recovery developed innovative technology in 2016 for water desalination called the PX pressure exchanger. A combination of displacing their key competitor in 2016 and much better efficiency compared to thermal desalination drove growth. The cost of desalination through their reverse osmosis process is only about 25% of thermal desalination. As the world heats up and fresh water sources become scarce, desalination is an alternative many governments will consider. They are now expanding the use of their PX pressure exchanger in refrigeration systems that are replacing hydrofluorocarbons (HFCs) with carbon dioxide, especially in Europe. The company is growing rapidly and has software like gross margins. This combination also means that it trades at a premium valuation. Forward growth rate is decelerating and I would like to see additional inroads into refrigeration systems before I get interested.

Disclaimer: I hold long positions in Atlas Energy Solutions (AESI) and Vitesse Energy (VTS). Please do your own due diligence before buying or selling any securities. We do not warrant the completeness or accuracy of the content or data provided in this article.

Last week I spent a few days in Chicago attending the Midwest Ideas conference, one of three wonderful conferences Three Part Advisors holds each year. This was my first time in Chicago and I absolutely loved the city. I fully understand that winters can be brutal in the Windy City and that I saw no more than a tiny sliver of the city but it is beautiful and the river walk area was excellent for taking a long walk after the conference. I really enjoyed meeting some old friends at the conference and made some new ones.

Last week I spent a few days in Chicago attending the Midwest Ideas conference, one of three wonderful conferences Three Part Advisors holds each year. This was my first time in Chicago and I absolutely loved the city. I fully understand that winters can be brutal in the Windy City and that I saw no more than a tiny sliver of the city but it is beautiful and the river walk area was excellent for taking a long walk after the conference. I really enjoyed meeting some old friends at the conference and made some new ones.