- Subscribe

- Premium

- C-Suite

- Insiders

- M&A

- Gurus

- Spinoffs

- Buybacks

- More

Flip floppers have a bad reputation in politics. People like to see their politicians hold fast to a set of principles or beliefs instead of changing them on a whim. The reality is unfortunately far different from people’s expectations of their elected officials.

In financial markets, flip flopping is actually a good sign because when new information becomes available, it is best to change your mind instead of doubling down on your existing position. All the best investors including Warren Buffett and Stanley Druckenmiller have done it.

When challenged by a critic for being inconsistent, famed economist Lord John Maynard Keynes was credited for saying:

“When the facts change, I change my mind. What do you do, sir?”

Some also attribute a version of this saying to Noble prize winning economist Paul Samuelson. At the end of the day, it doesn’t matter who said it and how they said it but the key lesson is that the smartest folks are willing to turn on a dime and act differently when they run into information that contradicts their original hypothesis.

Flip flopping among company insiders is rare, as insiders who were buying shares on the open market, don’t all of a sudden start selling. Nor are you likely to see chronic sellers turn into buyers of their company’s stock.

Besides the signal this kind of behavior would send to the market, the other reason for this reluctance to switch sides has to do with the SEC. The SEC does not want insiders to engage in short-term trading and requires them to give back any profits from trades that happened within a six month period.

This is called the “short-swing profit rule”. Section 16(b) of the Securities Exchange Act of 1934 states that if an insider of a public company buys and sells, or on the other hand sells and buys, stock of the company within a six-month period, they have to disgorge profits from these “matching” trades to the company.

The rule is used to discourage insiders from using the information they possess to make short-term profits. Every once in a while, we come across insider transactions where the insider indicates that the transaction violates the Short-Swing Profit rule. In most of these cases, the footnotes of the filing indicate that the insider is going to return any profits from the prior trade back to the company.

Flip flopping insiders are sending us a signal that they think the prevailing winds have changed and that they are willing to give up some short-term profits to make even more money down the road.

The Flip Flopper is a premium screen we built on InsideArbitrage that identifies insiders who purchased and sold shares within a period of time. For example they purchased shares on July 1, 2024 and sold those shares by September 5, 2024. The screen also identifies insiders that were selling and then suddenly flip to buying instead.

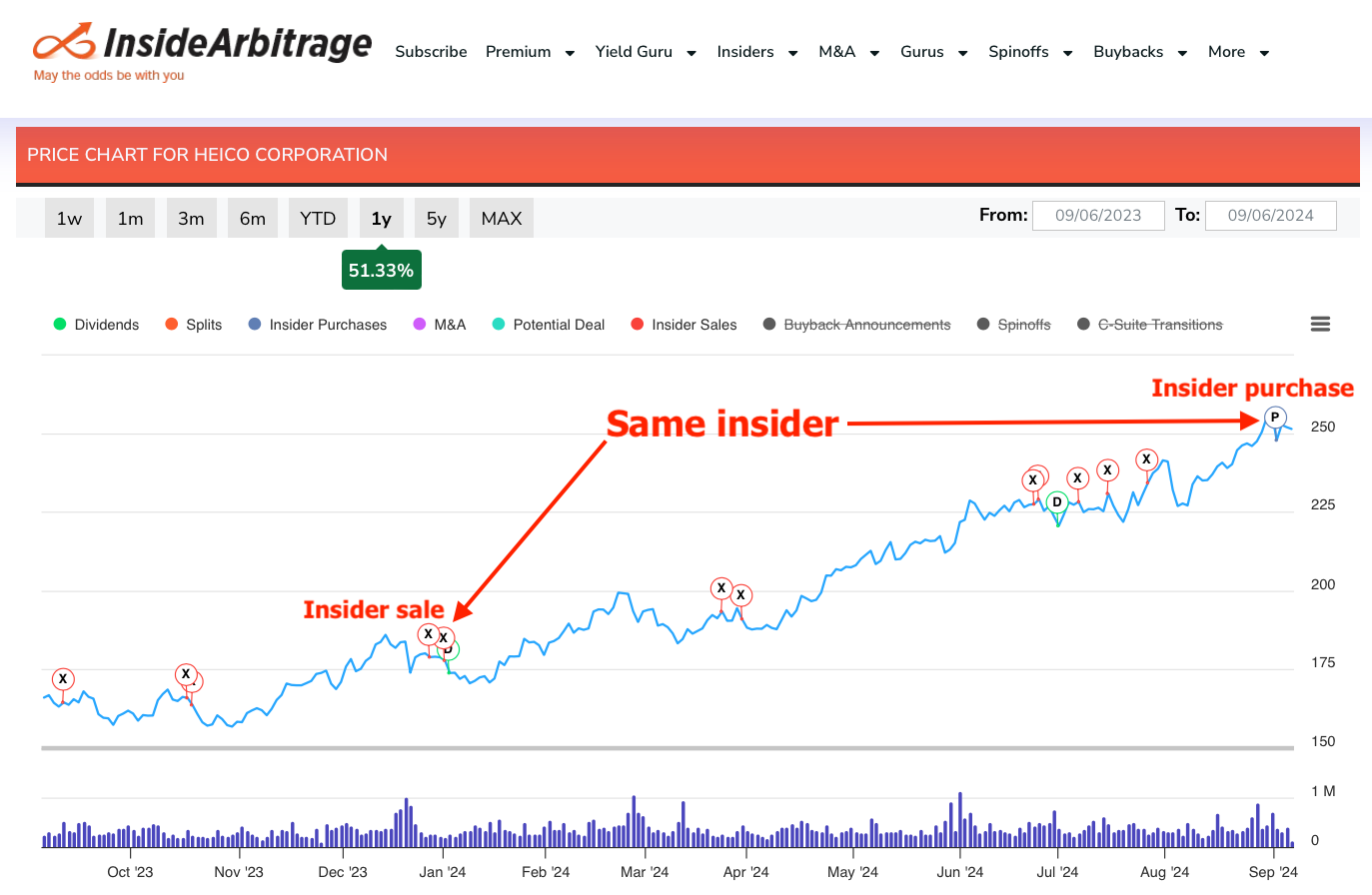

Last week I came across a flip flopper situation that does not meet the six month criteria but was interesting nevertheless. The company is HEICO (HEI) and it is the largest supplier of FAA approved parts for aircraft engines and components. Think of it as an aftermarket auto parts supplier with significantly lower pricing compared to an OEM like General Electric (GE) but with healthier margins.

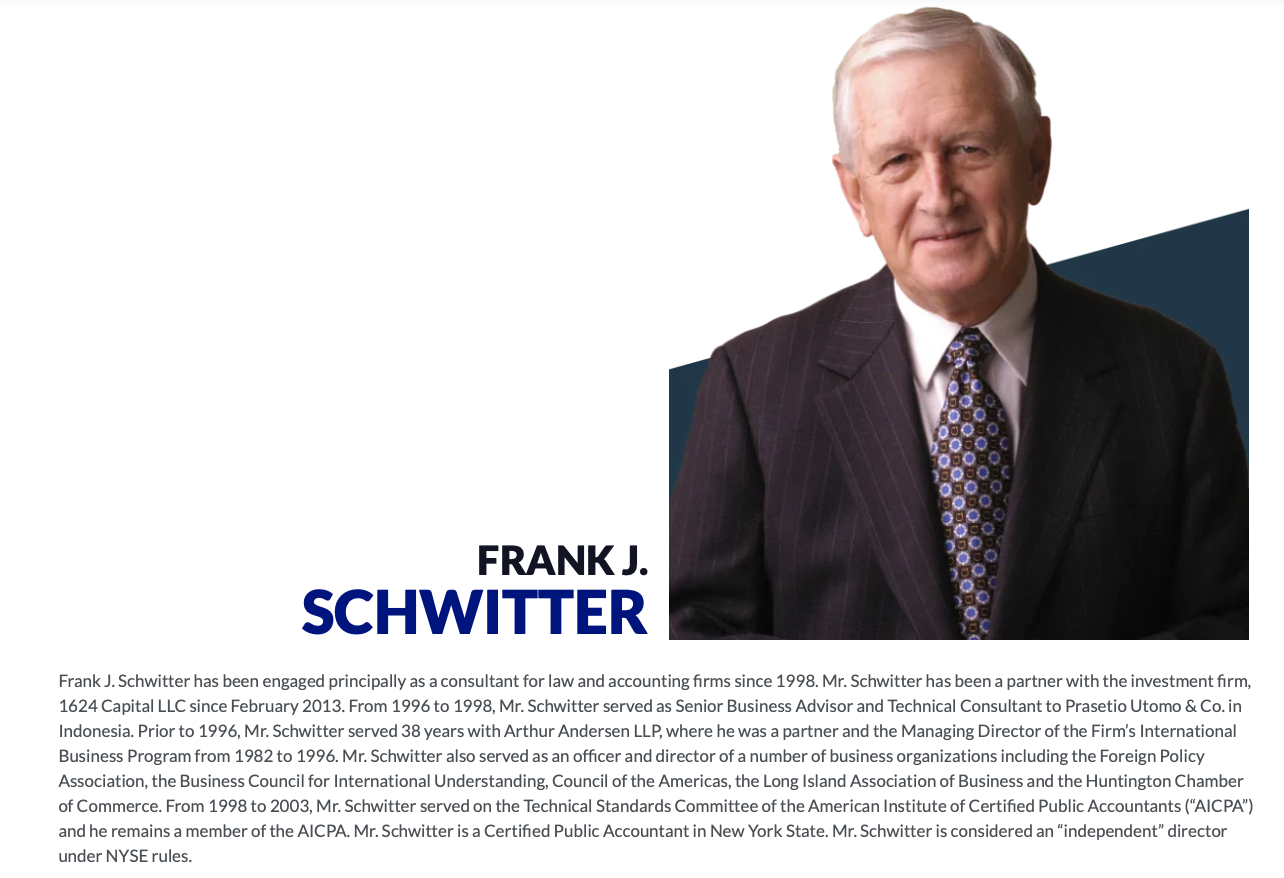

The insider that flip flopped was, Frank Schwitter, an independent director with an investing background. Exactly the kind of insider we like to track. He was selling shares in January and then purchased shares last week despite a 40% run up in the stock price this year.

Mr. Schwitter’s background as listed on HEICO’s website is given below:

Mr. Schwitter’s background as listed on HEICO’s website is given below:

Considering HEICO has two classes of shares including class A shares (HEI.A) and common shares (HEI), I verified that this wasn’t a dual class arbitrage situation like Greif (GEF). Insiders of Greif, including their CFO and General Counsel, would often sell class A shares to buy class B shares, because the class B shares entitled them to a larger dividend. There is no economic difference between HEI and HEI.A but class A shares of HEICO only carry 1/10th of a vote per share.

Considering HEICO has two classes of shares including class A shares (HEI.A) and common shares (HEI), I verified that this wasn’t a dual class arbitrage situation like Greif (GEF). Insiders of Greif, including their CFO and General Counsel, would often sell class A shares to buy class B shares, because the class B shares entitled them to a larger dividend. There is no economic difference between HEI and HEI.A but class A shares of HEICO only carry 1/10th of a vote per share.

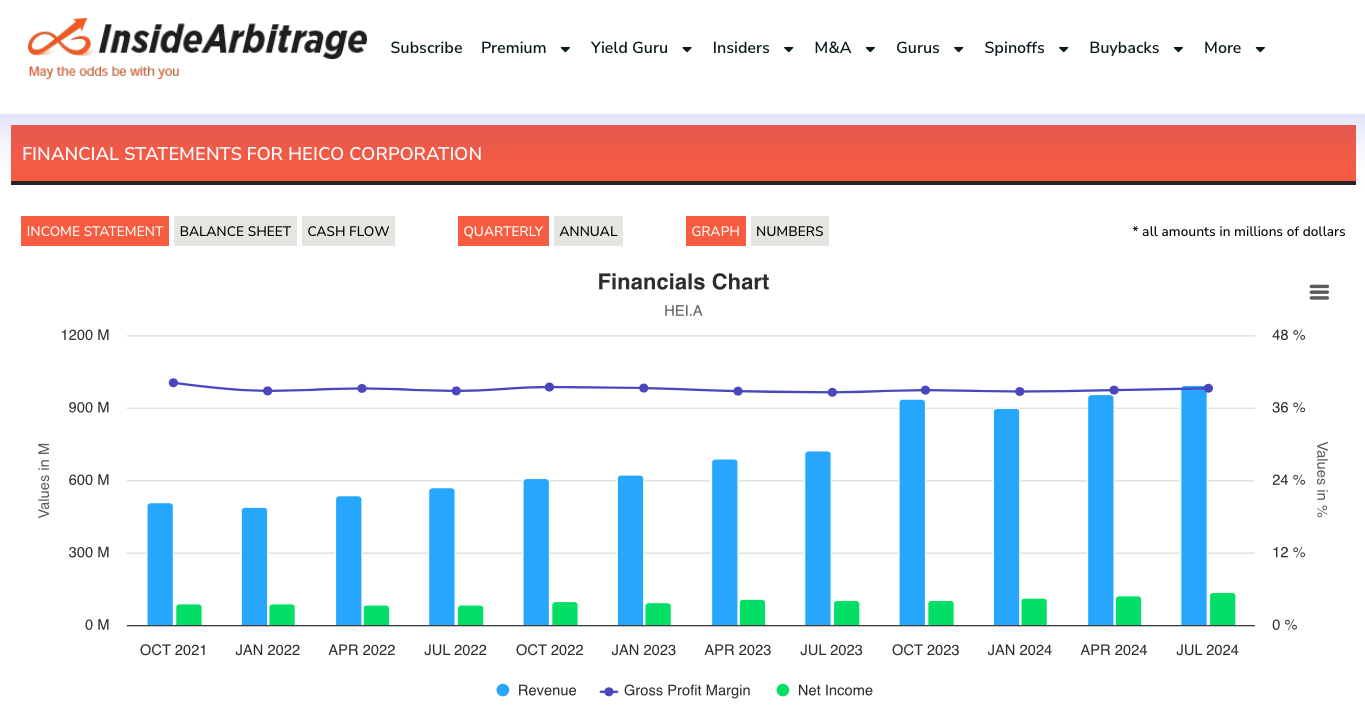

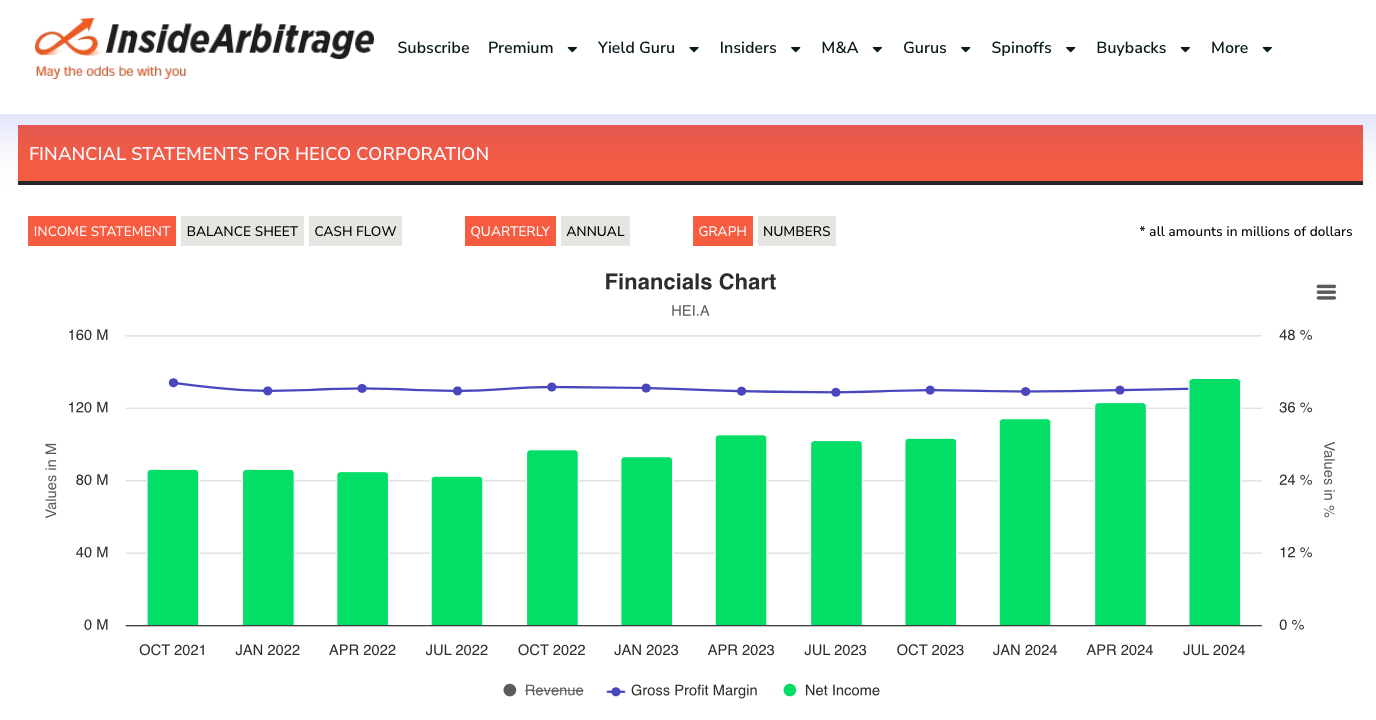

I have personally been long GE for some time now and can see how the acceleration in aircraft engine orders GE has seen in recent years will eventually lead to more business for HEICO in the coming years. You can already see this acceleration in HEICO’s revenue and especially its earnings over the last few quarters.

As one would expect, HEICO trades at a high valuation, especially after the 53% run up in the stock over the last year. I am intrigued that Mr. Schwitter is willing to buy at these levels and have added HEICO to my watchlist.

As one would expect, HEICO trades at a high valuation, especially after the 53% run up in the stock over the last year. I am intrigued that Mr. Schwitter is willing to buy at these levels and have added HEICO to my watchlist.

Disclaimer: I hold a long position in General Electric (GE). Please do your own due diligence before buying or selling any securities mentioned in this article. We do not warrant the completeness or accuracy of the content or data provided in this article.