- Subscribe

- Premium

- C-Suite

- Insiders

- M&A

- Gurus

- Spinoffs

- Buybacks

- More

Split-offs and the McDonald’s – Chipotle Example

In 2006 McDonald’s (MCD) decided to spin-off its Mexican fast casual chain Chipotle (CMG) in a series of transactions that started with an IPO of Chipotle in January, followed by a secondary offering a few months later and finally through a split-off in October 2006. After the IPO and secondary offering, McDonald’s had retained a 51% economic stake and 82% voting interest in Chipotle. McDonald’s decided to divest this remaining stake through a spilt-off.

The October 2006 split-off allowed McDonald’s shareholders to exchange their shares for Chipotle shares in a tax free transaction to the tune of receiving $1.11 worth of Chipotle stock for every $1 worth of McDonald’s stock tendered. This offer to exchange their shares for a fast growing chain and that too at a nice discount proved very attractive. A large number of McDonald’s shareholders offered to exchange their shares and the proration factor applied was 7%. Which means that for every 100 shares of McDonald’s shares tendered, only 7 were accepted for the exchange. This proration factor did not apply to anyone tendering 99 shares of McDonald’s as those were considered an “odd lot” and were accepted in full.

Shareholders that chose the exchange did very well in the subsequent year even after excluding the discount they received to Chipotle’s market price on the two days preceding the exchange date. Chipotle’s stock rose 121%, while McDonald’s went on to gain a still respectable 36%. Longer-term Chipotle is up nearly 3,000% since that exchange compared to a nearly 600% gain in McDonald’s not accounting for dividends.

The Johnson & Johnson – Kenvue Split-Off

Taking a page out of Pfizer, GlaxoSmithKline and Merck’s playbooks, Johnson& Johnson announced its intent to separate the company’s consumer health business, creating a new publicly traded company. In the tradition of picking oddball names for consumer products companies, the new company was called Kenvue and housed popular brands including Tylenol, Band-Aid, Neutrogena, Aveeno and more.

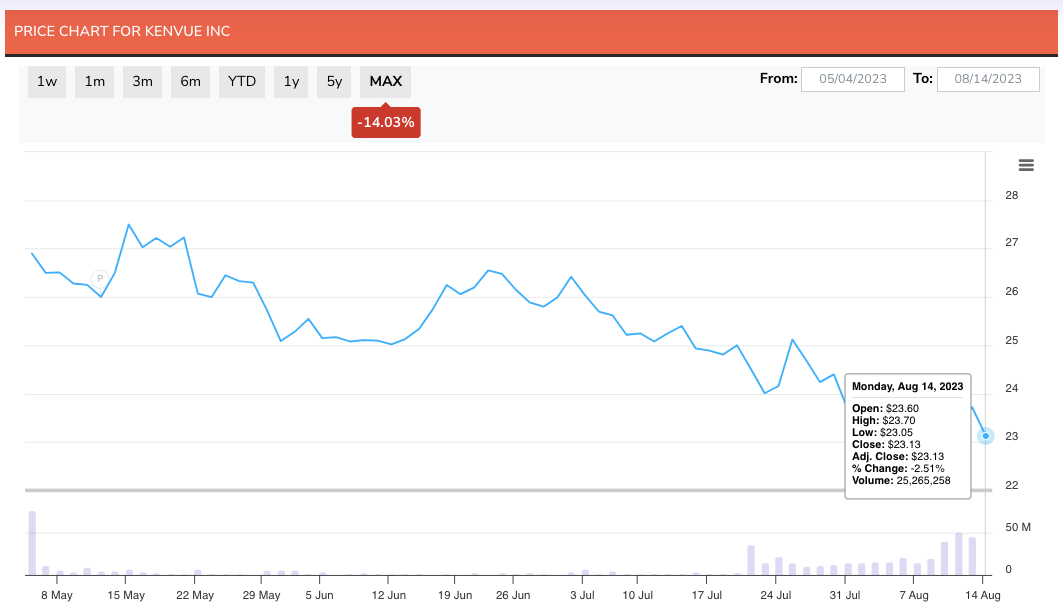

On May 3, 2023, Johnson & Johnson successfully priced the initial public offering of Kenvue Inc (KVUE), at the higher end of the projected range. The IPO generated $3.8 billion in proceeds through the listing of approximately 172.8 million shares at $22 per share valuing Kenvue at around $41 billion. The stock gapped on its first trading day to close at $26.90 and has steadily declined since to its current $22.94.

We are going to discuss the split-off opportunity from two perspectives. One as an arbitrage opportunity and the other from the viewpoint of a long-term shareholder of Johnson & Johnson.

The Arbitrage Opportunity

Johnson & Johnson disclosed on July 24, 2023, its intention to split off a minimum of 80.1% of Kenvue shares via an exchange offer. According to the press release:

‘The exchange offer will permit Johnson & Johnson shareholders to exchange some, all or none of their shares of Johnson & Johnson common stock for shares of Kenvue common stock at a 7% discount, subject to an upper limit of 8.0549 shares of Kenvue common stock per share of Johnson & Johnson common stock tendered and accepted in the exchange offer. If the upper limit is not in effect, tendering shareholders are expected to receive approximately $107.53 of Kenvue common stock for every $100 of Johnson & Johnson common stock tendered.’

This due date for the exchange is this Friday, August 18th providing for a nice opportunity to capture a nearly 7% spread in a short period of time. Since there are no free lunches offered by the market, there are risks to consider as discussed below.

The pricing for the exchange of shares between Johnson & Johnson common stock and Kenvue common stock will be determined based on the average of the daily volume-weighted average prices of these stocks on the NYSE over a span of three consecutive trading days. This period is set to encompass the days leading up to and including the second trading day before the exchange offer’s expiration date, projected to be August 14, 15, and 16, 2023, unless there is an extension or termination of the offer.

Based on the price of $173.44 per share price of Johnson & Johnson and $22.94 per share price of Kenvue on August 14th, it looks like the upper limit of 8.0549 shares will likely be hit assuming both stocks don’t move a lot in the next two days. This translates to a discount of 6.5% on Kenvue if Johnson & Johnson shareholders opt for the exchange. The assumption that both stocks might not move a lot in the next two days might be wishful thinking because traders are likely shorting Kenvue stock to close out their position. This limits the risk from Kenvue dropping a lot right after the exchange is completed.

Besides a lower exchange ratio, the other risk arbitrageurs also face is proration. If too many JNJ shares are tendered for the exchange, arbitrageurs could end up with JNJ shares that they would then have to sell on the open market.

Thankfully for smaller accounts, there is an odd lot provision where if someone tenders 99 shares of Johnson & Johnson, they will be accepted.

A way to capture the nearly 7% discount on Kenvue is to buy 99 shares of JNJ, tender them for exchange by Friday and then hedge that position by shorting the number of Kenvue shares that will be received from the split-off. The cost of the short position will be high because borrowing costs are very high right now on Kenvue shares and this will bring down the effective return on the position.

For arbitrageurs that might decide to get into this trade unhedged, the following discussion about the long-term prospects of both companies might be helpful.

Kenvue operates across three distinct segments: Self Care, Skin Health and Beauty, and Essential Health.

Within the Self Care segment, products such as Tylenol, Nicorette, and Zyrtec underpin offerings for cough, cold and allergy relief, pain management, digestive health, and smoking cessation.

In the realm of Skin Health and Beauty, the brand names Neutrogena, Aveeno, and OGX represent face and body care, hair care, and sun protection products.

Lastly, the Essential Health segment encompasses Listerine, Johnson’s, Band-Aid, and Stayfree brands, delivering items for oral and baby care, women’s health, and wound care.

Even after Kenvue’s IPO, Johnson & Johnson remains accountable for numerous claims asserting that its talc baby powder and related talc items have been linked to cancer. These particular products were previously part of J&J’s consumer-health business, which has now become Kenvue. However, the spinoff is set to take on only the talc-related liabilities originating from regions outside the United States and Canada, as indicated in its IPO filing from January. The other talc related liabilities remain with J&J.

In the second quarter of 2023, Kenvue experienced expansion in sales across all three of its business divisions.

Kenvue Q2 2023 Financial Results

In the second quarter, Kenvue recorded sales amounting to $4.01 billion, marking a 5.4% increase compared to the corresponding period in the prior year. However, gross margin was negatively impacted by 2.3% due to foreign exchange headwinds, as indicated by Kenvue.

The net income for the quarter was $430 million, translating to earnings of 23 cents per share, in contrast to the previous year’s figure of $604 million, equating to 35 cents per share. Adjusted for specific items, the company’s earnings were 32 cents per share.

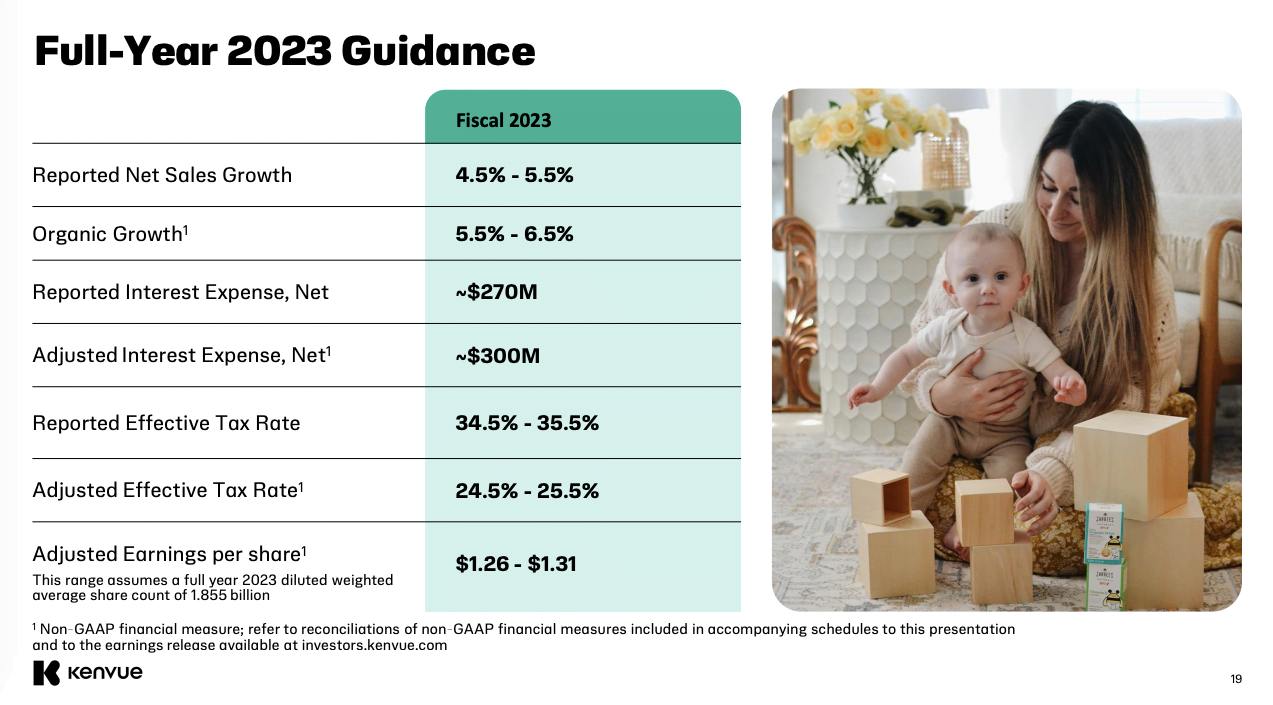

Kenvue has projected a sales growth range of 4.5% to 5.5% for the full year 2023. After its IPO, the company stated that it anticipates global annual sales growth to be approximately 3% to 4% until 2025. Regarding full-year adjusted earnings, Kenvue’s outlook is $1.26 to $1.31 per share

Johnson & Johnson (JNJ) $173.44

Q2 2023 Financial Results

Johnson & Johnson posted net income of $5.14 billion, translating to $1.96 per share, in comparison to a net income of $4.8 billion, or $1.80 per share, for the same period last year. When excluding specific items, the adjusted earnings per share amounted to $2.80 for this duration. The company has projected full-year sales to fall within the range of $98.80 billion to $99.80 billion, which marks an increase of approximately $1 billion compared to the guidance issued in April. Additionally, it has revised its 2023 adjusted earnings forecast to range between $10.70 and $10.80 per share, an upward adjustment from the previous projection of $10.60 to $10.70 per share.

I decided to compare a few metrics across both companies to see how they measure up.

| Johnson & Johnson | Kenvue | |

| Dividend | 2.74% | 3.40% |

| Payout Ratio | 44% | 62% |

| Gross Margin | 67.50% | 55.62% |

| Net Margin | 13.35% | 11.12% |

| 2023 Revenue Growth | 3.31% | 5% to 6% |

| Forward P/E | 16.13 | 17.85 |

| Forward EV/EBIDTA | 13.07 | 13.75 |

| Net Debt / Equity | 61.00 | 76.00 |

Conclusion

I checked with a couple of Johnson & Johnson shareholders and they don’t plan to exchange their shares for Kenvue, which makes a lot of sense. Kenvue is a company that has lower margins than Johnson & Johnson, is more indebted and trades at a slightly higher forward P/E based on adjusted EPS estimates for 2023. Moreover Johnson & Johnson benefits from a pipeline of drugs that could power future growth. The key risk with Johnson & Johnson is the talc liabilities for U.S. and Canada.

Unlike the Chipotle example we started this mid-month update with, Kenvue is not a high growth company and can be considered more of a stable income generating opportunity that might become more attractive at a lower price.

This situation is best for an arbitrage trade and preferably an odd lot hedged trade that can generate profits of around $1,000 in a short period of time assuming borrowing costs don’t go through the roof. I don’t see the exchange to be particularly beneficial for long-term Johnson & Johnson holders. In the short-term I expect Kenvue shares to remain weak because of the dynamics of the trade that require arbitrageurs to short the stock. There is however some positive news on the horizon once the exchange is complete as Kenvue will be added to the S&P 500 and this will generate index related buying that should provide a lift to the stock in the near future.

Given the dynamics of this trade, I will not be adding Kenvue to our model portfolio.