- Subscribe

- Premium

- C-Suite

- Insiders

- M&A

- Gurus

- Spinoffs

- Buybacks

- More

Over the last three years, I have added several ideas to our watchlist that I liked but wanted to follow for a while or pick up at a more attractive price. Unfortunately in many cases, these companies got away from me and from a recent review of the watchlist, I realized that I would have been much better off buying them right away instead of adding them to the watchlist. Not all the watchlist stocks have gone on to do well, but as is usually the case, the big winners more than pay for the losers in a diversified portfolio.

The current market turmoil has hit stocks in specific industries particularly hard and this has created a couple of opportunities. I am going to move a company that was on our watchlist to the model portfolio and double down on an existing position in the portfolio.

American Assets Trust (AAT) $18.82

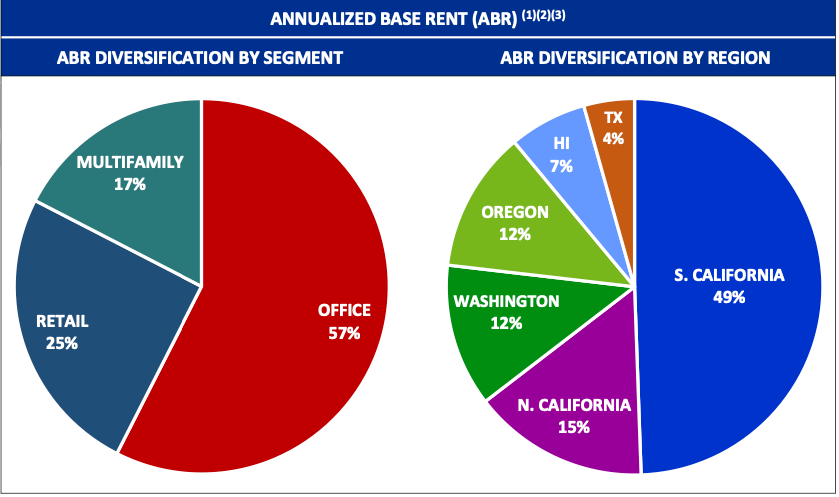

American Assets Trust is a diversified REIT with premium properties covering office (57%), retail (25%) and multifamily (17%) in Western states including California, Oregon, Washington State and Hawaii. I have been following the company for several years and wrote about the company in more detail in our September 2022 Special Situations newsletter.

I wrote the following about the company in our September newsletter:

Ernest Rady, the 84 year old Chairman and CEO of American Assets Trust (AAT), founded the real estate company’s predecessor American Assets in 1967 after moving his family from Manitoba,Canada to the sunny clime of San Diego, California. We have written about the company several times in the past few years and some of this might be familiar to long-term subscribers of InsideArbitrage.

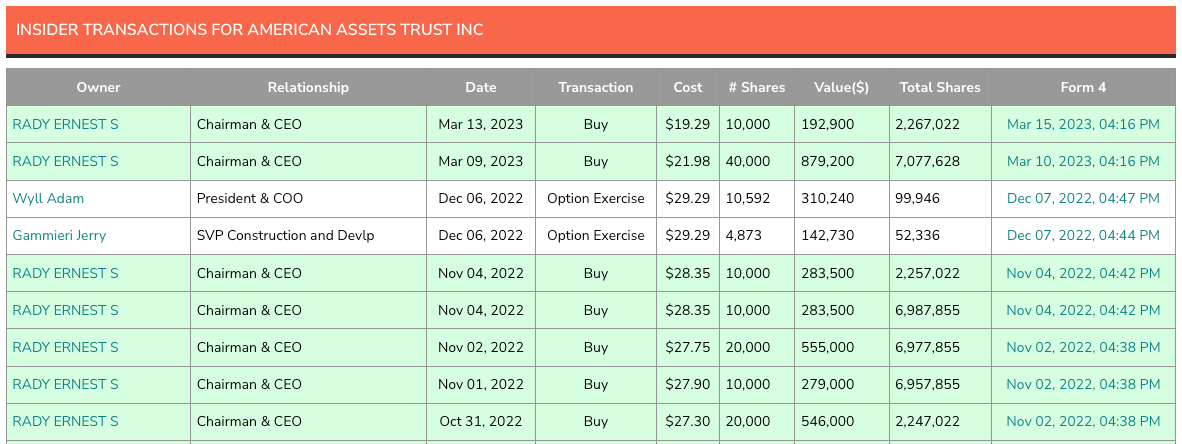

American Assets Trust (AAT) grabbed my attention during the pandemic related downturn in REITs and especially in REITs that focused on the retail or office segments. AAT dropped to the low $20s twice during the depths of the pandemic but did not stay there for very long. After noticing a string of insider purchases by Mr. Rady in late 2020, my first reaction was to dismiss the company. Who in their right mind would want to own an office REIT when most parts of the U.S. and especially the geographic locations AAT operated in, were in lockdown?

Upon further investigation I realized that AAT was more than an office REIT and had a diversified portfolio of premium retail, office and multifamily properties with one Embassy Suite hotel thrown in for good measure. The company’s portfolio spans 5 different states with most of its properties concentrated in California, Hawaii, Oregon and Washington, with one location in San Antonio, Texas. I’ve had a chance to visit one of their properties (shown below) near Waikiki beach in Hawaii but at the time did not realize it was an AAT property.

The company’s focus on premium properties partially helps explain why unlike other retail and office REITs, AAT’s revenue and funds from operations (FFO) did not take a dramatic hit during the pandemic with revenue down just 2.4% in Q2 2020 and down 14.22% in Q3 2020. By 2021, the company’s revenue and net operating income (NOI) had already exceeded their pre-pandemic 2019 revenue and NOI.

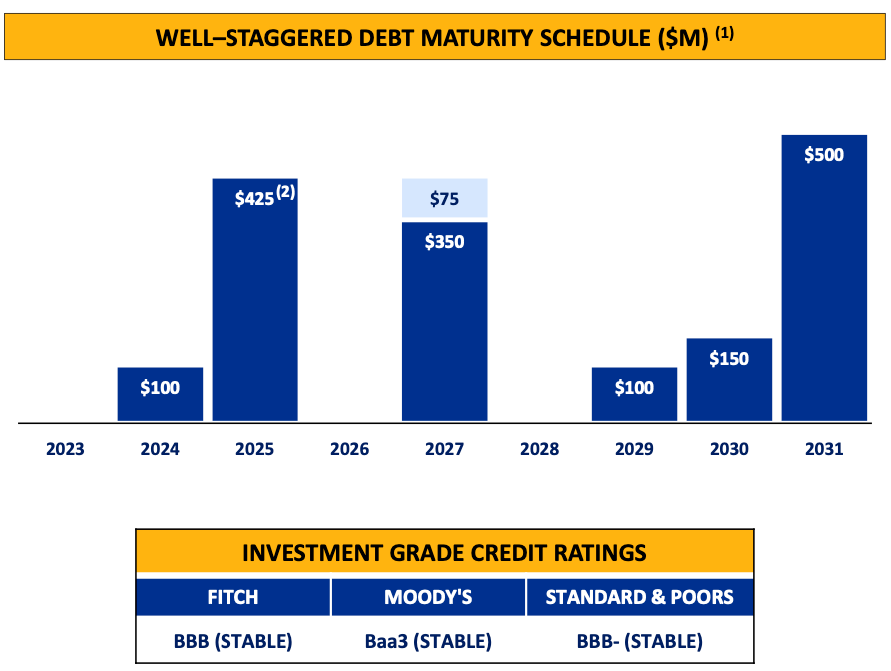

My biggest concern at that time was valuation and the impact of interest rate increases on REITs that had enjoyed very favorable rates for an extended period of time. The debt maturity profile turned out not to be a big concern because most of the company’s debt was maturing well into the future. The company recently refinanced $150 million of debt that was due in March 2023 by rolling it into $225 million of new debt. The interest rate went from 2.65% to 5.47% and the impact on funds from operations (FFO) was $0.10. The company has more cash on hand now ($104 million) and its full revolver credit line ($400 million) accessible compared to when we wrote about the company last September. The current debt profile is given below.

I concluded the September newsletter as follows:

REITs with premium properties in highly desirable locations will be able to offset the impact of higher rates through higher rents, especially in a high inflation environment. However if the recession deepens, companies continue laying off employees and high interest rates make alternative investments more attractive, then all bets are off. Mr. Rady has capitalized on the recent stock weakness by increasing his insider purchases. AAT has survived multiple market cycles and its performance during the pandemic was admirable. Given the current environment, it might be a good idea to monitor the stock for further weakness or buy gradually over time. I am going to add AAT to our watchlist and monitor it for buying opportunities in the future.

The stock was $27.76 when we wrote about it and has dropped sharply from those levels to the current $18.82. I was not surprised to see that after his last set of insider purchases in November 2022, Mr. Rady started buying again this month, picking up 50,000 shares for about $1.07 million.

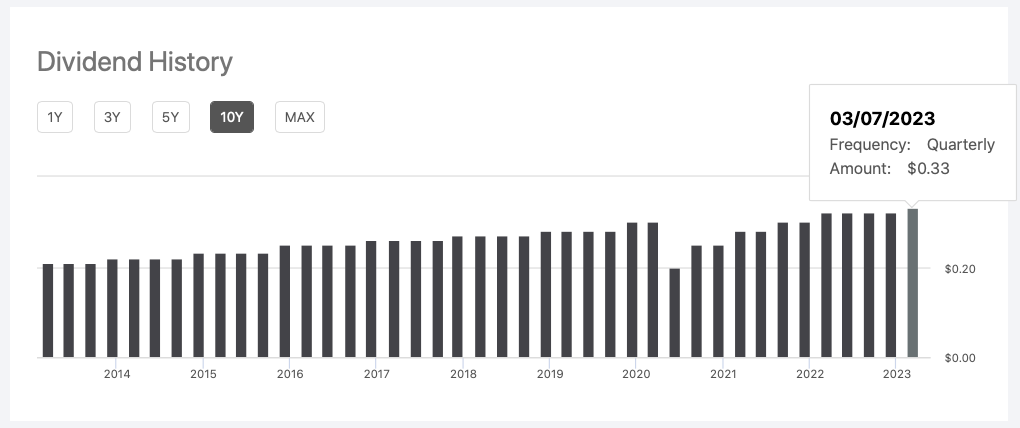

The yield on the REIT has now spiked to over 7% based on a quarterly payout of $0.33 per share. At the mid-point of its 2023 guidance, the company expects $2.23 in FFO, a decline of 4.7% from 2022. This puts the company’s payout ratio at a conservative 59%, leaving additional room for dividend increases. With the exception of a few quarters during the pandemic, the company has continuously increased its divided every year as you can see from the dividend history below.

The stock trades for 8.44 times the estimated 2023 FFO, which for a well managed REIT like American Assets Trust appears to be a steal. The company has $3.7 billion worth of properties on its balance sheet ($2.76 billion after depreciation) and $1.6 billion of net debt. The stock not only trades below where Mr. Rady was buying last November and earlier this month but also below where it traded at the bottom of the pandemic bear market. I think concerns about interest rates is more than baked into the current price. If you continue to remain concerned about market volatility, you can scale into the position across multiple trades spread out over a few months.

I am going to start a position for the model portfolio at our full position size ($5,000) and will also be purchasing the stock for my personal portfolio after this mid-month update is published.

First Horizon Bank (FHN) $15.68

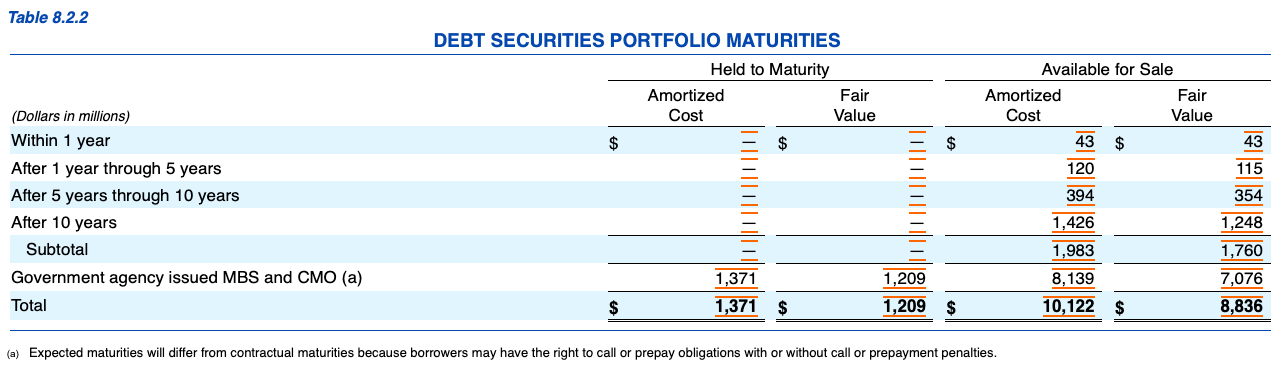

We discussed the merger arbitrage situation where Canadian bank TD is acquiring First Horizon in our March 6th Merger Arbitrage Mondays article. Since then, the banking world changed and we had three bank failures including the 16th largest bank in the U.S. failing in a single day. Available for sale (AFS) and held to maturity (HTM) securities entered the lexicon of investors. Fears about mark-to-market risk hiding in bank balance sheets has seen the entire banking sector take a hard hit.

First Horizon was no exception and the spread on the deal increased to 59.44% or over 200% annualized if the $25 per share all cash deal can close by mid-year without a price cut. I pulled up First Horizon’s 10-K and their held to maturity securities at $1.21 billion (fair value) are a small fraction of total assets and equity, unlike what we are seeing at Charles Schwab, Silicon Valley Bank, Bank of Hawaii and Bank of America.

Following this big decline in the price, First Horizon currently trades at 1.16 times its book value of $13.48 as of December 31, 2022. If the deal goes through, we have a near term catalyst to realize value. If it does not go through, I don’t mind owning the company below 1.2 times book value. I am going to increase our position in the model portfolio by adding 215 shares to our existing position of 215 shares. I will also be increasing my personal position in First Horizon after this mid-month update is published.

Following this big decline in the price, First Horizon currently trades at 1.16 times its book value of $13.48 as of December 31, 2022. If the deal goes through, we have a near term catalyst to realize value. If it does not go through, I don’t mind owning the company below 1.2 times book value. I am going to increase our position in the model portfolio by adding 215 shares to our existing position of 215 shares. I will also be increasing my personal position in First Horizon after this mid-month update is published.