- Subscribe

- Premium

- C-Suite

- Insiders

- M&A

- Gurus

- Spinoffs

- Buybacks

- More

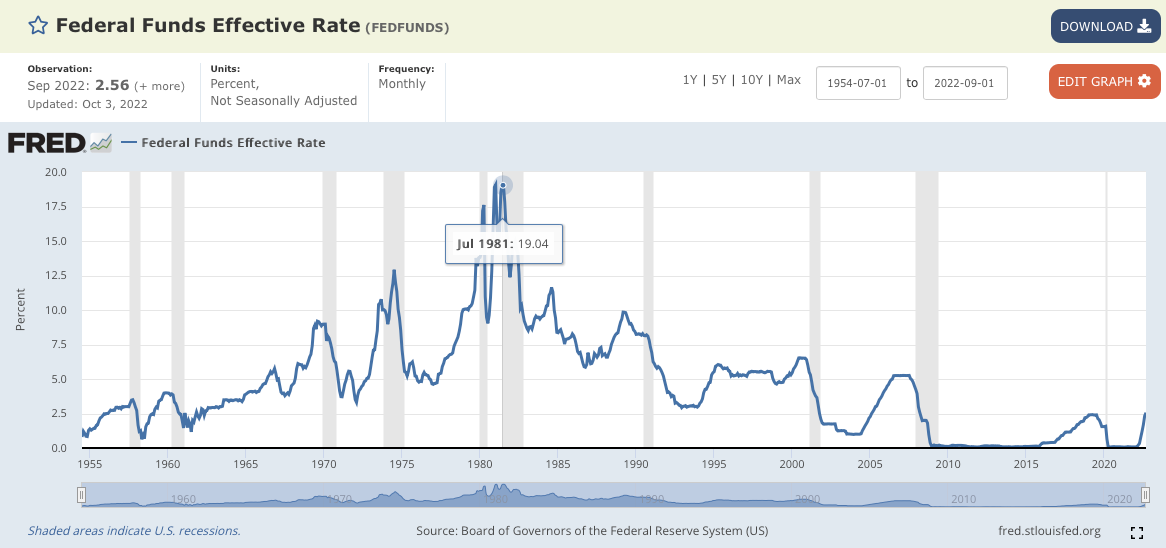

The St. Louis Fed’s website FRED is a treasure trove of data and tools for the data curious. If you want to pull back the curtain on the current narrative and see how history played out, pull up a chart on FRED and see what happened to the Fed Funds Effective Rate, the Sticky CPI or the M2 Money Supply over decades. Fair warning: You might get sucked down a wormhole of data.

NAREIT is another wonderful resource for REIT investors and it has decades of data about the performance and yields of real estate investment trusts. I really like how they break down REIT data by sectors and sub-sectors and you can check out average yields after excluding mortgage REITs, which by their very nature tend to have very high yields (often in the double digits).

When I was looking at apartment REITs as a potential area of investment during the 2008/2009 bear markets, I looked at the spread or difference between REIT yields and the 10 year treasury note. The comparison is important for several reasons. If an investor can get a reasonable return, say 5% from 10 year treasury notes, their appetite for REITs is going to be limited unless a REIT is yielding more and has potential for capital appreciation. The other reason is that 10 year treasury notes are a good benchmark for long-term borrowing rates and REITs that benefited from decades of refinancing their debt at lower rates, will now run into interest rate headwinds. Even if they have pricing power with the ability to raise rents, payouts will be impacted by rising interest payments. Scarce capital will also mean fewer options to acquire new properties. When asset values are dropping, it becomes harder to dispose of properties as a source of capital or to divest underperforming properties.

Given this perfect storm, it is not surprising to see that the The Vanguard Real Estate ETF (VNQ) lost more than a third of its value this year. What is surprising to me is the big jump in insider buying I am seeing at REITs. I see this pretty much every day I look at form 4 filings for our daily event-driven monitor series of articles. Last week, we reported on insider purchases in the apartment REIT BRT Apartments (BRT), the office REIT Hudson Pacific Properties (HPP) and the diversified REIT Nexpoint Diversified Real Estate Trust (NXDT). The diversified REIT American Assets Trust (AAT) is a frequent guest in our Insider Weekends series of articles, was a spotlight idea in our September 2022 Special Situations newsletter and I wrote the following about AAT in that newsletter,

American Assets Trust (AAT) grabbed my attention during the pandemic related downturn in REITs and especially in REITs that focused on the retail or office segments. AAT dropped to the low $20s twice during the depths of the pandemic but did not stay there for very long. After noticing a string of insider purchases by Mr. Rady in late 2020, my first reaction was to dismiss the company. Who in their right mind would want to own an office REIT when most parts of the U.S. and especially the geographic locations AAT operated in, were in lockdown?

Upon further investigation I realized that AAT was more than an office REIT and had a diversified portfolio of premium retail, office and multifamily properties with one Embassy Suite hotel thrown in for good measure.

The company’s focus on premium properties partially helps explain why unlike other retail and office REITs, AAT’s revenue and funds from operations (FFO) did not take a dramatic hit during the pandemic with revenue down just 2.4% in Q2 2020 and down 14.22% in Q3 2020. By 2021, the company’s revenue and net operating income (NOI) had already exceeded their pre-pandemic 2019 revenue and NOI.

REITs with premium properties in highly desirable locations will be able to offset the impact of higher rates through higher rents, especially in a high inflation environment. However if the recession deepens, companies continue laying off employees and high interest rates make alternative investments more attractive, then all bets are off. Mr. Rady has capitalized on the recent stock weakness by increasing his insider purchases. AAT has survived multiple market cycles and its performance during the pandemic was admirable. Given the current environment, it might be a good idea to monitor the stock for further weakness or buy gradually over time.

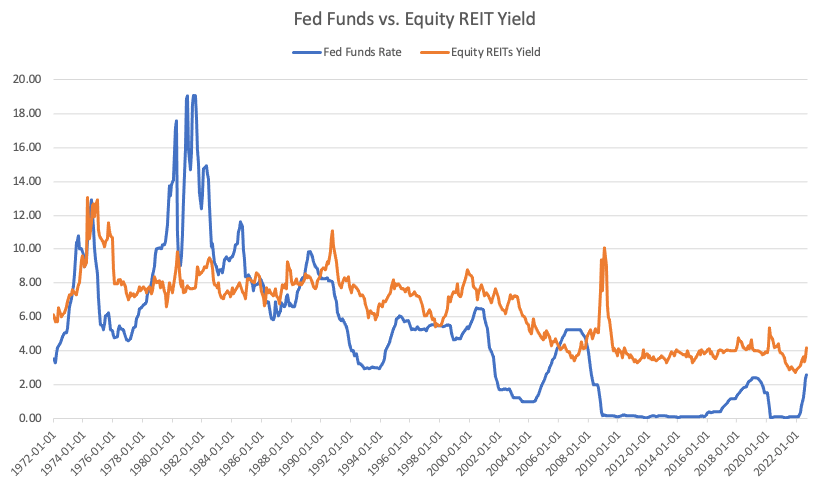

Since writing about it, I have been monitoring AAT frequently to see if Mr. Market is offering it up at an attractive price and it isn’t quite where I want it. I didn’t want to base my opinion on how it performed during the pandemic and wanted to pull back the curtain further. I also wanted to look at the big picture by tracking the spread between the Federal Funds Effective Rate and the average yield of REITs, which is where the abundant data from FRED and NAREIT comes in. I was able to download data for the Fed Funds Rate going back to 1954 and REIT yields data back to January 1972. The following chart shows the relationship between the two over a period of more than 50 years.

With the exception of a few periods in the 1970s, through much of the 1980s and right before the Great Recession in 2006-2007, the spread between the Fed Funds Rate and Equity REITs was positive. The average spread was 1.58% and the median was 2.25%. The standard deviation of 2.93% indicates quite a bit of variability in the spread, which you can also observe in the chart above.

If we assume the Fed Funds Rate peaks at 5% next year, the average and median spread indicate REIT yield could be expected to hit anywhere from 6.58% to 7.25%. For a brief period in early 2000 and early 2009, REIT yields eclipsed 8% and 10% respectively. If we assume REIT yields will peak at around 7% this cycle and the current yield is 4.39% for Equity REITs according to NAREIT, then it implies that REITs have another 37% to drop before we get to a 7% yield. This assumes that payouts remain the same. If payouts decline because of a recession and higher debt servicing costs, the decline could be steeper. While this seems like a doomsday scenario for REITs, it is entirely plausible based on what we have seen in previous cycles. The other more optimistic possibility is that the spread narrows or even turns negative. I have exposure to medical property, single family and retail REITs and while I would prefer not to see my investments lose further value, the next six to twelve months could present great opportunities for investors that are willing to look beyond the current cycle. The time to act however, is not now.