- Subscribe

- Premium

- C-Suite

- Insiders

- M&A

- Gurus

- Spinoffs

- Buybacks

- More

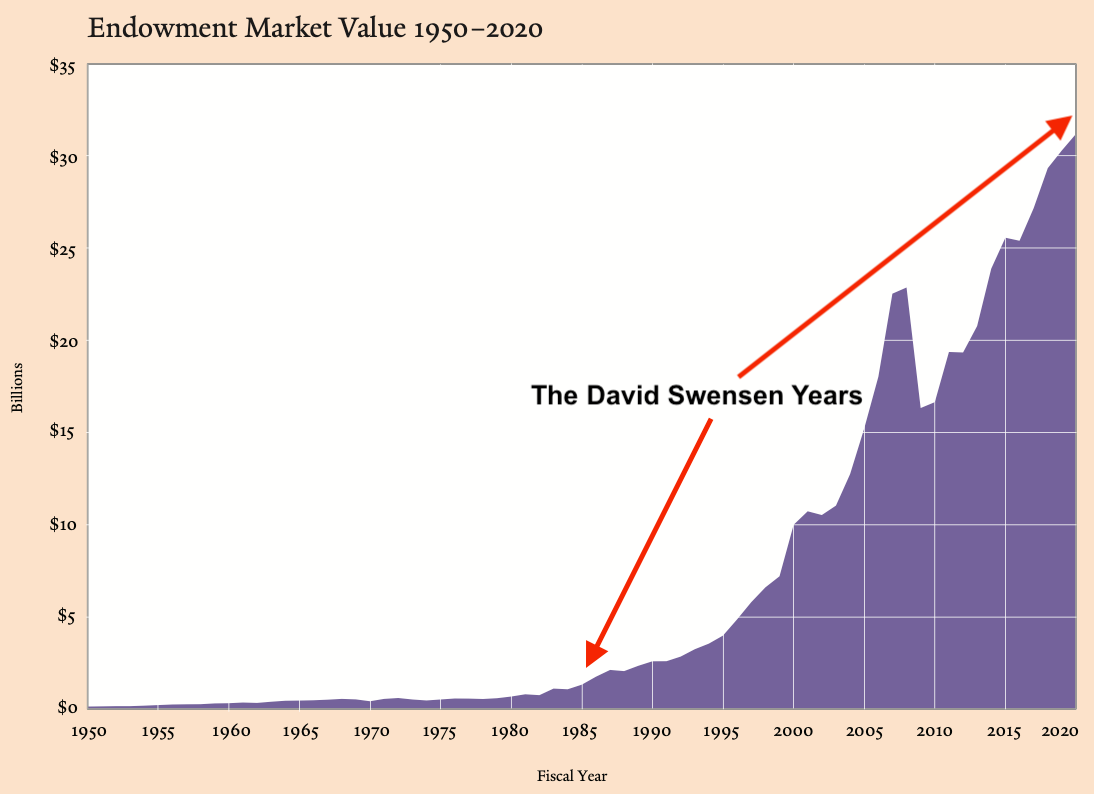

In fiscal 2021 ended June 30, 2021, Yale’s massive endowment generated $12.1 billion in investment gains. The size of these gains was only trumped by the fact that this represented a 40.2% return net of fees. Clearly Yale University was positioned well to benefit from the stimulus fueled pandemic bubble of 2020-2021. In a big loss to the investment community, less than two months before the end of Yale’s fiscal year, we lost David Swensen. Mr. Swensen served as Yale’s Chief Investment Officer from 1985 until his death in May 2021 and was instrumental in helping Yale’s endowment grow to $42.3 billion by June 30, 2021. Through the two decades ending in 2021, he generated annual gains of 11.3% significantly outperforming both U.S equities and bonds. His returns during his early years managing Yale’s endowment were even more impressive as you can see from the chart below.

In fiscal 2021 ended June 30, 2021, Yale’s massive endowment generated $12.1 billion in investment gains. The size of these gains was only trumped by the fact that this represented a 40.2% return net of fees. Clearly Yale University was positioned well to benefit from the stimulus fueled pandemic bubble of 2020-2021. In a big loss to the investment community, less than two months before the end of Yale’s fiscal year, we lost David Swensen. Mr. Swensen served as Yale’s Chief Investment Officer from 1985 until his death in May 2021 and was instrumental in helping Yale’s endowment grow to $42.3 billion by June 30, 2021. Through the two decades ending in 2021, he generated annual gains of 11.3% significantly outperforming both U.S equities and bonds. His returns during his early years managing Yale’s endowment were even more impressive as you can see from the chart below.

I was thankfully introduced to Mr. Swensen’s philosophy of investing early in my investing journey when I read his books Unconventional Success and Pioneering Portfolio Management. As someone who liked to focus on individual security selection, my biggest take away after reading these books was just how important asset allocation was compared to simply picking the right stocks. To put this in perspective, consider that going into fiscal 2021, Yale only had 2.3% of their portfolio in domestic U.S. stocks and their exposure to foreign equities was nearly fives times as much at 11.4%.

Given where we are at this stage of the market, I felt that it was appropriate to take a little break from idea generation/security selection and instead discuss portfolio construction. Bonds returns (at least for longer duration bonds) are inversely correlated to interest rates. With the rise in interest rates this year, bonds have been crushed after a nearly four decade bull market. This means that anyone that was using the traditional 60/40 portfolio (60% in equities and 40% in bonds) or even target date funds that automatically rebalance from stocks to bonds based on your target retirement date, has been hit hard this year.

A series of tweets by my friend @scipreblog over the long Labor Day weekend highlighted how 9 out of 10 large country ETFs are still trading at or around where they were in 2007. The one exception was the U.S.

A strong dollar that acts as the global reserve currency, a business friendly environment, laws that (for the most part) give investors a level playing field, companies that have been on the cutting edge of innovation and the ease of investing in U.S. securities have all contributed to both domestic and foreign investors pouring money into U.S. equities. Markets, economies and asset classes all move in cycles and it is not surprising to see that Vanguard believes foreign stocks will return 2.5% more than U.S. equities over the next decade. Considering the P/E of the S&P 500 is 21.53 (September 2022) compared to a P/E of 10.52 for South Korea (September 2022) and 13.16 for Singapore (June 2022), Vanguard’s prediction starts to make sense.

As investors, many of us suffer from both recency bias and home country bias. It might be time for us to look beyond our biases and start thinking about our portfolios more holistically by taking a page out of David Swensen’s storied career. Foreign equities, real estate, commodities and alternative investments are all going to be very important as we construct portfolios for the coming decade.