- Subscribe

- Premium

- C-Suite

- Insiders

- M&A

- Gurus

- Spinoffs

- Buybacks

- More

Writing covered calls is an investment strategy that works very well for some investors, especially at a time when markets are trading sideways or declining like we are currently experiencing. A majority of options expire worthless, skewing the strategy to the benefit of those writing the options and collecting premiums. Obviously if you go too far out the risk spectrum with options, you stand the risk of blowing up as recounted in gory detail in Malcolm Gladwell’s 2002 New Yorker article titled Blowing Up. While a covered calls strategy works great in theory, my personal experience has been a mixed bag and there are certain nuances to be aware of before adopting the strategy with gusto.

For those of you that are familiar with options, you can skip the next section borrowed from a premium post I wrote in 2019 to capture the merger arbitrage spread from Nvidia’s acquisition of Mellanox Technologies using options.

An equity option is a derivative product that grants the buyer the non-obligatory right to buy (if a put, to sell) 100 shares of an equity at a certain price by a certain time. In order to gain that right, the buyer of the contract pays a premium.

It is very similar to an insurance contract. When you buy car insurance, you are given the non-obligatory right to claim money upon certain conditions, namely that your car requires repairs. You have a limit on how much money you receive, and usually you are given a year before you renew your contract. Indeed, options were designed as portfolio insurance for investment institutions. Before options, there was no easy way a heavily diversified fund could simply buy insurance on their whole portfolio, and now they can.

I know you are thinking “Thanks for the lesson, why do I care in this arena of merger arbitrage?”

When you read the definition above, you can intuit three different variables that affect the value of each option. “At a certain price” reflects the movement of the equity price. “By a certain time” reflects a reliance on the amount of time until expiration, and the related expected volatility in that timeframe. “Premium” reflects that the option itself has a value. Much like insurance, the premium reflects the “implied volatility” of that option, and is subject to its own supply and demand. Fortunately, anyone can write or buy an option at market prices that reflect these variables.

Let us illustrate writing covered calls with an example. Assume that you purchased a 1,000 shares of Intel (INTC), for $45 per share during the market pull back in March 2022. You believe we are going to experience onshoring for critical manufacturing activities in the coming years and think Intel could benefit from this trend. You also like Intel’s decision to invest $20 billion in two factories in Arizona to meet demand from the U.S. Department of Defense and other commercial customers. You further believe that Intel will eventually catch up to Taiwan Semiconductor (TSM) or semiconductor demand is likely to be so high that both companies could thrive in a digital future.

The stock was trading at a forward EV/EBITDA below 7, had a dividend yield north of 3% and the dividend had grown roughly 6% a year during the last 5 years. Performance over the last five years was not stellar with gains of 22% compared to a nearly doubling in the S&P 500. After including dividends, performance improved to over 40%.

Considering the anemic growth in both the stock price and the dividend, you start looking into squeezing extra returns from your Intel position by writing covered call options and giving the option buyer the ability to buy Intel from you at a certain price (the strike price) for a certain period of time (until expiration). The option is “covered” because you own the underlying stock and can sell it to the buyer, if at expiration, the price of the stock exceeds the strike price of the option. You can also keep the stock and buy back the option at any time before expiration.

As I write this, looking at the options chain for Intel, I see that slightly “out of the money” $50 July 15th call options are trading at a bid of $1.72 and an ask of $1.74. The last trade was $1.73, implying someone paid $173 for the ability to buy 100 shares of Intel at $50 per share until July 15th. Open interest of 11,025 contracts and the small bid/ask spread imply ample liquidity. If you were to sell 10 covered calls at a strike price of $50 with the options expiring on July 15th, you would collect $1,730 in premium from the buyer of the options. This translates to a return of 3.84% on your $45 investment if the stock does not cross $50 by July 15th. If you can do this four times a year, you can squeeze an additional 15% returns (not taking compounding into account) from Intel beyond any appreciation in the stock and returns from dividends.

All of a sudden, you have a boring tech stock that appears past its prime, generating annual gains of 18% (15% from selling covered call options and 3% from dividends) before any potential appreciation in the stock. This is the allure of the covered calls strategy and when done right can generated a good source of additional income. It is not surprising that there are more than two dozen ETFs that can give you exposure to a covered calls strategy.

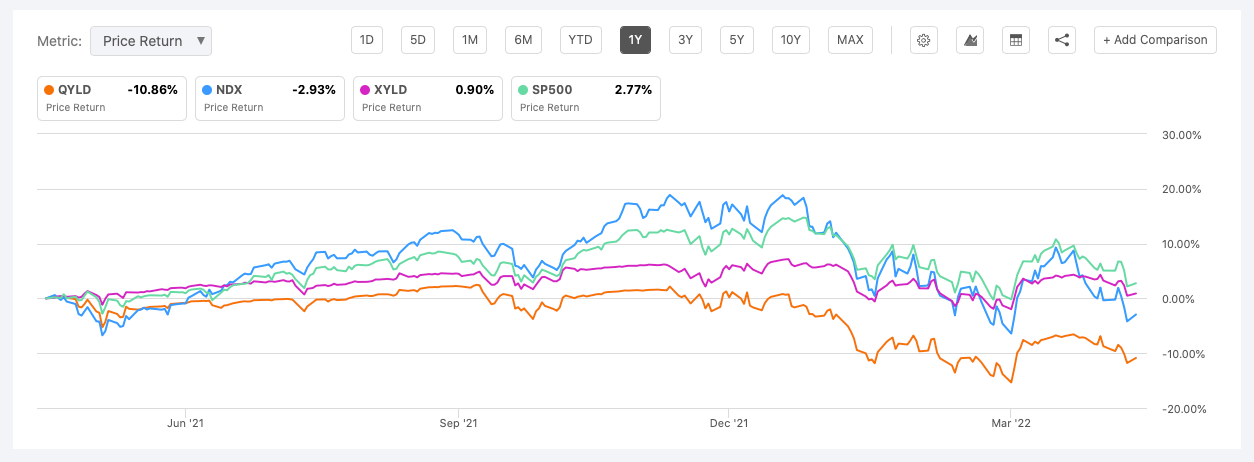

There are covered calls ETFs for the Nasdaq 100 (QYLD), the S&P 500 (XYLD), the Russell 2000 (RYLD) and the recently launched Dow 30 (DJIA). However when you take a closer look at some of these ETFs (at least the ones that have been around long enough), they lost money in each of the last one year, three year and five year periods. While QYLD did not drop as much as the Nasdaq 100 this year, returns were still negative.

This is where the nuances and pitfalls of a covered calls strategy come in. In a rising market, it is likely that the call options happen to be in the money at expiration and you would either be forced to sell the underlying stock at the strike price or buy back the option at a higher price. You could delude yourself into thinking that you will sell the stock now and buy it back later when it dips lower but that dip may not happen or you may have moved on to other things. This was my experience with selling covered calls on storage company Western Digital (WDC) and the gaming company Take Two Interactive (TTWO) more than a decade ago. Right after those stocks were called away, they went on to more than quadruple in price.

Portfolio returns are often driven by a few outliers and this is true both for individual portfolios as well as indexes like the S&P 500 and the Russell 2000. The “ten baggers” that we end up with, either by luck or by skill, drive our portfolio returns even as other positions languish or lose most of their value. Writing covered calls indiscriminately could create an asymmetrical risk/reward profile where the potential best performers get called away long before their full potential is realized and we are left with the losers. This could partially explain the dismal performance of the aforementioned ETFs. Beyond performance, it is also important to understand the tax implications of a covered calls strategy and Fidelity does a great job of covering them in this article.

However as illustrated in the Intel example, if the strategy is adopted with a portion of the portfolio that consists of stable low beta stocks then the strategy could work to generate additional income. Portfolio construction and understanding each position well are prerequisites to adopting a covered call strategy. Different market cycles require different strategies and given current market conditions, I am starting to once again get interested in a covered calls strategy.