- Subscribe

- Premium

- C-Suite

- Insiders

- M&A

- Gurus

- Spinoffs

- Buybacks

- More

American Homes 4 Rent (AMH) $22.49

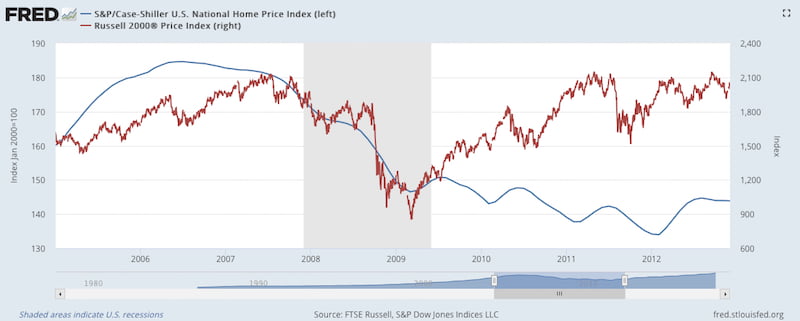

The U.S. housing market, as represented by the S&P Case Shiller Index, peaked nearly a year before the stock market started its sharp decline during the great recession of 2008-2009. While the stock market bottomed in March 2009, it took an additional three years for the housing market to bottom in early 2012 as you can see from the chart below.

American Homes 4 Rent (AMH) with its portfolio of 52,049 single-family homes across 22 states was conceived during the depths of the last housing recession by billionaire B. Wayne Hughes. His impeccable timing in scooping up homes very close to the bottom could have been luck but was probably more on account of his decades long-experience with real estate as the founder and CEO of the largest self-storage company Public Storage (PSA). He retired as CEO of PSA in 2002 and stepped down as Chairman in 2011, just in time to start American Homes 4 Rent. The Seattle Times wrote an article about the company in 2013 and we started noticing his insider purchases of AMH in late 2014.

American Homes 4 Rent is structured as a Real Estate Investment Trust (REIT) that are required to pay 90% of their taxable income to investors as a dividend. Unlike most equity REITs that sport dividend yields around 4%, the yield on AMH is less than 1%. You can find yield data for the various flavors of REITs from the NAREIT website here.

So why would an investor pay any attention to a REIT that yields less than 1% especially in a rising interest environment that is usually unfavorable to REITs? The answer can be found on AMH’s balance sheet, which shows $8.18 billion in properties after depreciation and $2.58 billion in debt consisting of senior notes and asset backed securities. The value of their properties before depreciation is $9.23 billion. The market value of these properties is probably significantly higher than what we see on the balance sheet because AMH purchased a large number of its properties near the bottom of the housing market.

Investors soured on hidden asset plays like Sears Holdings (SHLD), where a declining operating business reduced the appeal of their real estate portfolio. Sum-of-the-parts situations like the old Yahoo (now Altaba) with its stakes in Alibaba and Yahoo Japan worked out in the end but it took several years for the investment thesis to play out. The situation with AMH is very different as revenue has more than doubled over the last three years and is on track to exceed $1 billion this year. Net income was negative until 2015 but turned positive over the last two years.

Most REIT investors tend to focus more on Funds From Operations (FFO) or Adjusted Funds From Operations (AFFO) because it excludes depreciation, which tends to be a large expense for these asset heavy REITs. Instead of trying to figure out the nuances of a non-GAAP metric like AFFO, looking at free cash flow provides a good proxy. Efficiencies of scale have translated into higher free cash flow for AMH over the years and reached $95.6 million last quarter. Unless the rental market collapses or the company embarks on a large capital intensive project, it would not be difficult for the company to generate nearly half a billion in free cash flow next year.

I had three concerns about AMH when I first started taking a look at the company. A rising interest rate environment is usually a headwind for REITs and while AMH might be attractive in its own right, the stock could see downward pressure if the entire sector is weak. The second concern was that maintaining a portfolio of individual family homes might be more challenging than maintaining a portfolio of apartments like AvalonBay Communities (AVB) or Equity Residential (EQR) do. My third concern was that occupancy rates for single family homes might be significantly lower than that seen by apartment REITs.

The first concern is going to remain a headwind but if AMH starts increasing its regular dividend it might offset some of the sector weakness. Despite the healthy free cash flow AMH generates, the dividend paid to investors is a mere 20 cents a share, which translates to about $60 million per year with nearly 300 million shares outstanding. This translates to a payout ratio of less than 15%. Dividends paid for preferred shares has been declining and was just $12 million last quarter as you can see from the latest 10-Q filing. After taking both common and preferred dividends into account, the company still has a lot of room to increase its dividend if it chooses to do so.

Regarding my second concern, maintenance is indeed more difficult and this can be seen in the large difference in operating margins between AMH and AvalonBay where AMH’s 10% operating margin is dwarfed by AvalonBay’s 27% operating margin. I expect operating margins for AMH to continue to improve as it has for the last several quarters but I doubt they will achieve anything close to the apartment REITs.

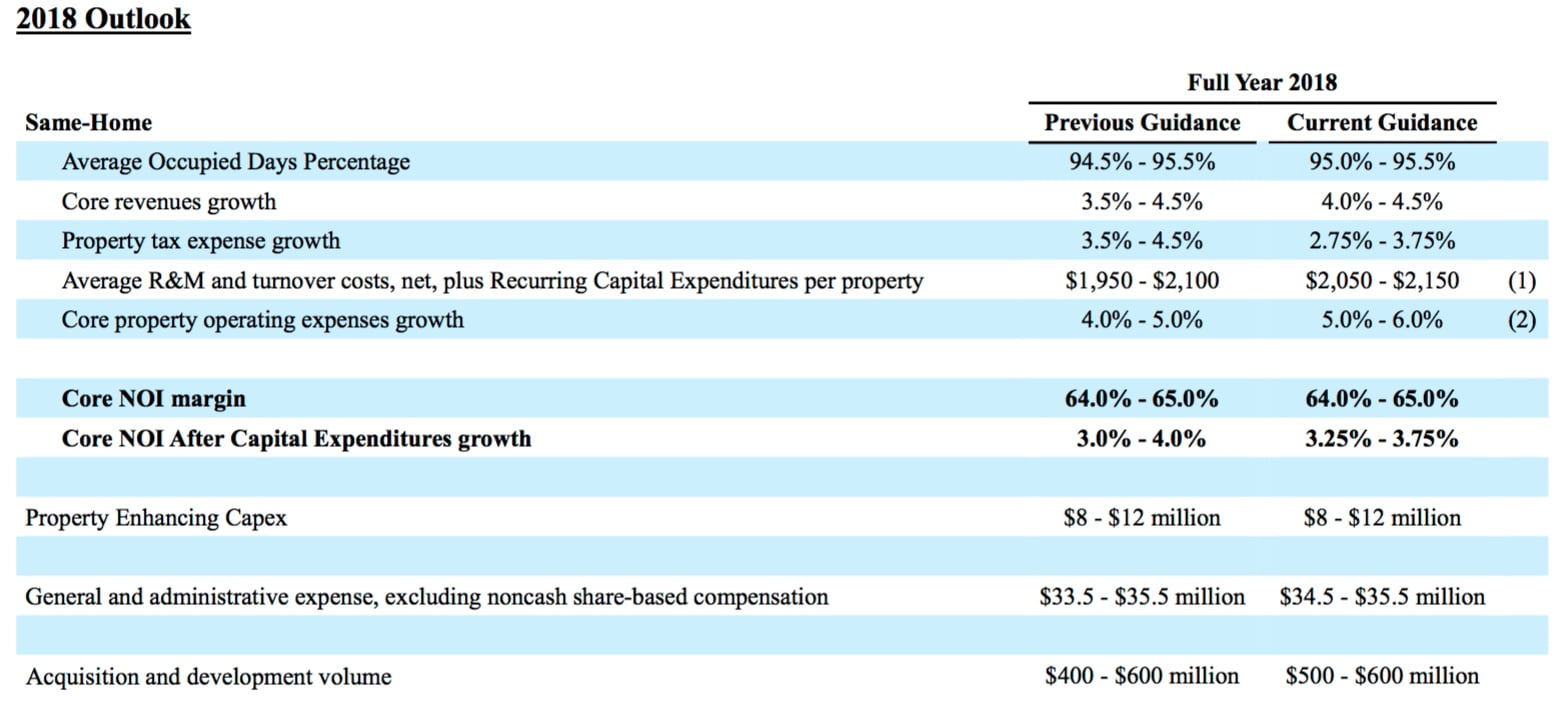

Regarding occupancy rates, I was pleasantly surprised to see that AMH increased its outlook for occupancy rates to a range of 95% to 95.5% as you can see from their 2018 outlook below.

I can see why Mr. Hughes as well as his daughter Tamara Hughes Gustavson consistently keep buying stock. Knowing a company is undervalued might not be sufficient to realize a return on your investment unless the gap between the perceived value and current market value closes. So how might investors expect to see a return on their investment? An increase in their regular dividend yield, special dividends funded by the liquidation of parts of their portfolio or an acquisition are three ways we might realize a return on our investment.

An acquisition is not very likely given the size of the company but is not completely out of the question as both AvalonBay and Equity Residential are three times the size of AMH. I believe once they complete their expansion and redemption of preferred shares, they are going to start returning capital to common shareholders either through an increase in the regular dividend or through special dividends. In conclusion AMH offers the opportunity to buy a company that is generating significant and increasing free cash flows and the net assets on the balance sheet likely exceed the market cap of the company.

Voluntary Disclosure: I currently do not hold a position in AMH but plan on starting a long position after this post is published.