- Subscribe

- Premium

- C-Suite

- Insiders

- M&A

- Gurus

- Spinoffs

- Buybacks

- More

Over the long weekend, I got a chance to catch the new movie by Apple, F1, starring Brad Pitt and my personal favorite, Javier Bardem (of No Country for Old Men fame). With an estimated production cost of over $250 million, the movie did not disappoint and I would put it up there with Ford v Ferrari and Rush when it comes to racing-related movies. F1 currently has an IMDB rating of 7.9 out of 10 and 83% on Rotten Tomatoes.

Advertisers Galore

What also stood out about F1 were the product placements or ads, with the microcap company Expensify (EXFY), the consumer products company SharkNinja (SN), Tommy Hilfiger, GEICO and the watchmaker IWC taking the cake.

IWC is owned by Compagnie Financière Richemont, a Swiss luxury goods holding company listed on the SIX Swiss Exchange under the stock symbol CFR. Tommy Hilfiger, along with Calvin Klein, is owned by PVH Corp (PVH). We were recently taking a look at PVH on account of a $1 million insider purchase by its CEO Stefan Larsson and realized that the company had shed its legacy brands like Van Heusen, Arrow, IZOD and Geoffrey Beene in 2021 to Authentic Brands Group. GEICO was the crown jewel of Berkshire Hathaway for decades.

Oracle (ORCL) and its rival Workday (WDAY) also made appearances.

A Comparison of Expensify and SharkNinja

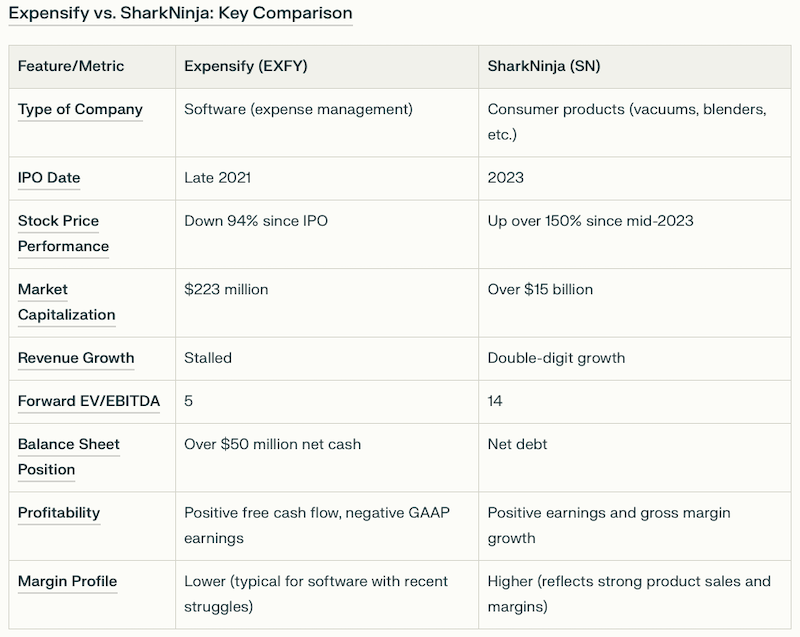

I decided to take a closer look at both Expensify (EXFY) and SharkNinja (SN) because both companies have had relatively short stints as public companies with Expensify going public in late 2021 and SharkNinja in 2023. The similarities end there. One is a software company that makes it easy for you to file your expenses, which is a real pain for corporate warriors that spend a lot of time out of the office. The other is a consumer products company that positions itself somewhere between Hamilton Beach Brands (HBB) and Dyson with its vacuum cleaners, blenders, air purifiers, ice cream makers and more.

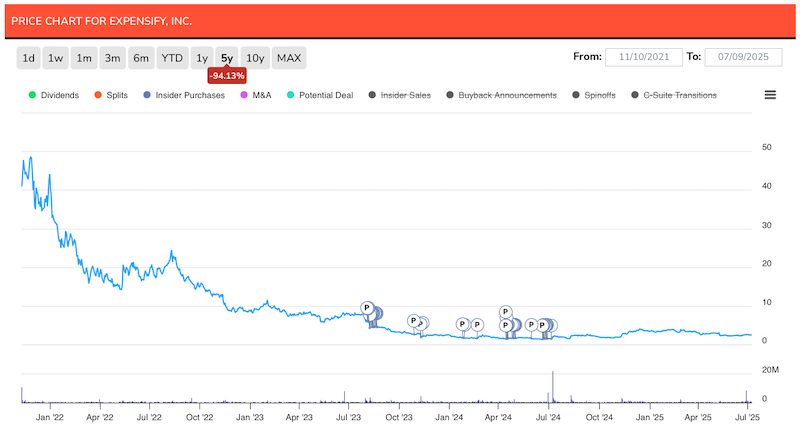

The differences don’t end there. Expensify has seen its stock price drop an astounding 94% and has a market cap of just $223 million. In contrast, SharkNinja has seen its stock jump up more than 150% since mid-2023 and has a market cap of over $15 billion.

While Expensify has seen its revenue growth stall and valuation drop to a forward EV/EBITDA of just 5, SharkNinja is growing sales by double digits and has a forward EV/EBITDA of 14. Expensify has over $50 million of net cash on its balance sheet, while SharkNinja has net debt. Considering one is a software company and the other a consumer products company, the margin profiles are also very different. Unfortunately for Expensify, while free cash flow is positive, GAAP earnings are absconding. SharkNinja’s stock price growth reflects its earnings and gross margin growth.

Stock Buyback and Bold Marketing Bet

Management teams of companies that are cash rich and are adding additional cash to the balance sheet through free cash flow, often resort to stock buybacks to take advantage of low valuations and bring down shares outstanding. Expensify was no different. The company announced a $50 million buyback in February that represented a whopping 17% of its market cap at announcement.

More than the buyback, I am impressed by the company’s decision to spend an estimated $40 million to advertise in the F1 movie. If the movie does turn out to be as big of a hit as it is expected to be (F1 has already raked in $300 million worldwide in the first 11 days), this gamble could pay off for Expensify.

Beyond this potential near-term boost to the company (I am not sure how inspired corporate purchasers would be to sign up for Expensify after watching the movie), what Expensify really needs is to get back to sustainable revenue growth and manage expenses to start reporting GAAP earnings. The company’s gross margin of 52% is well below what you would expect from a software company (usually between 70% and 90%) and as is often the case, stock-based compensation is larger than it needs to be ($34 million over the last twelve months).

If software-focused private equity firms like Thoma Bravo or potential strategic acquirers were not already paying attention to Expensify (EXFY), this big advertising bet might do the trick.