- Subscribe

- Premium

- C-Suite

- Insiders

- M&A

- Gurus

- Spinoffs

- Buybacks

- More

What did companies like Walmart (WMT), Bank of America (BAC), Walt Disney (DIS), Dow (DOW) and Procter & Gamble (PG) that operate in disparate industries all have in common back in the 1990s and 2000s? Potential answers to this question could be:

The actual answer is: “dead peasant insurance”.

Dead peasant insurance was a kind of Corporate-Owned Life Insurance (COLI) where companies were buying life insurance policies on their employees without the employee being aware of the existence of these policies. To make matters worse, when the employee passed away, it was the corporation that received a payout related to the employee’s death instead of the family. Yikes!

At one point in the 1990s, Walmart had such a large COLI program that it covered 350,000 employees.

Why did companies engage in such unsavory (to the general public) practices? They did it for the tax advantages these payouts received since these payouts were not classified as regular income. In addition, the companies also borrowed money against the value of some of these policies to pay insurance premiums. Not all of these policies were put in place to maximize corporate profits, and many of them were done to either fund pension plans or to pay for employee benefits.

Upset Families and Lawsuits

Clearly families were very upset when they found out about these policies, there were multiple lawsuits filed against the companies and these policies received a lot of media attention.

The Pension Protection Act of 2006

According to Perplexity:

“Congressional concern over COLI abuses led to significant regulatory reform through the Pension Protection Act of 2006. This legislation imposed three critical requirements for companies to maintain tax advantages on employee life insurance policies. First, employees must receive written notification that their employer intends to insure their lives, including the maximum face amount of coverage. Second, employees must provide written consent both to being insured and to continuation of coverage after employment termination. Third, employees must be notified in writing that their employer will be the beneficiary of death proceeds.

The Act also restricted COLI eligibility to the highest-paid 35 percent of employees, significantly limiting the scope of permissible coverage compared to previous practices”

A Secondary Market for Life Insurance?

Why am I bringing up dead peasant insurance nearly two decades after the passage of the Pension Protection Act of 2006? When company insiders buy or sell company stock, the SEC requires them to file something called a form 4 within two business days after the transaction. The filing covers everything from gifting stock to a grandchild, to exercising options or RSUs when they vest.

We look at these form 4 filings every night. Each weekend, we compile a list of the top five insider purchases and sales from the prior week and pick one company to write about briefly in articles we call Insider Weekends.

The whole process, while it might appear tedious, has been one of my favorite research activities over the last fifteen years. Once you get the hang of reading these filings, it doesn’t take more than a few minutes to review the few dozen filings that meet our internal criteria each night.

During earnings seasons, when company insiders are restricted from buying or selling stock, these filings dwindle to a handful. At other times, and especially during market downturns, they swell and keep us very busy. To help investors understand how to read form 4 filings, I wrote an article called Deconstructing Form 4 Filings Filed By Company Insiders a few years ago. This article in many ways formed the backbone of the chapter focused on insiders in my book The Event-Driven Edge in Investing.

Getting back to life insurance, in our last insider weekends article, I found not one but three fascinating special situations and ended up writing briefly about all three.

Reviewing insider transactions every night and then again every weekend has a treasure hunt quality to it. We constantly discover new companies that we might not have otherwise encountered. Last week was special. Beyond the three fascinating special situations I wrote about, there was a fourth company that was equally fascinating but since I had just discovered the company, I was not ready to write about it as a potential investment.

It is what prompted me to write this article and reminded me about the dead peasant insurance controversy that was swimming somewhere in the deep recesses of my memory.

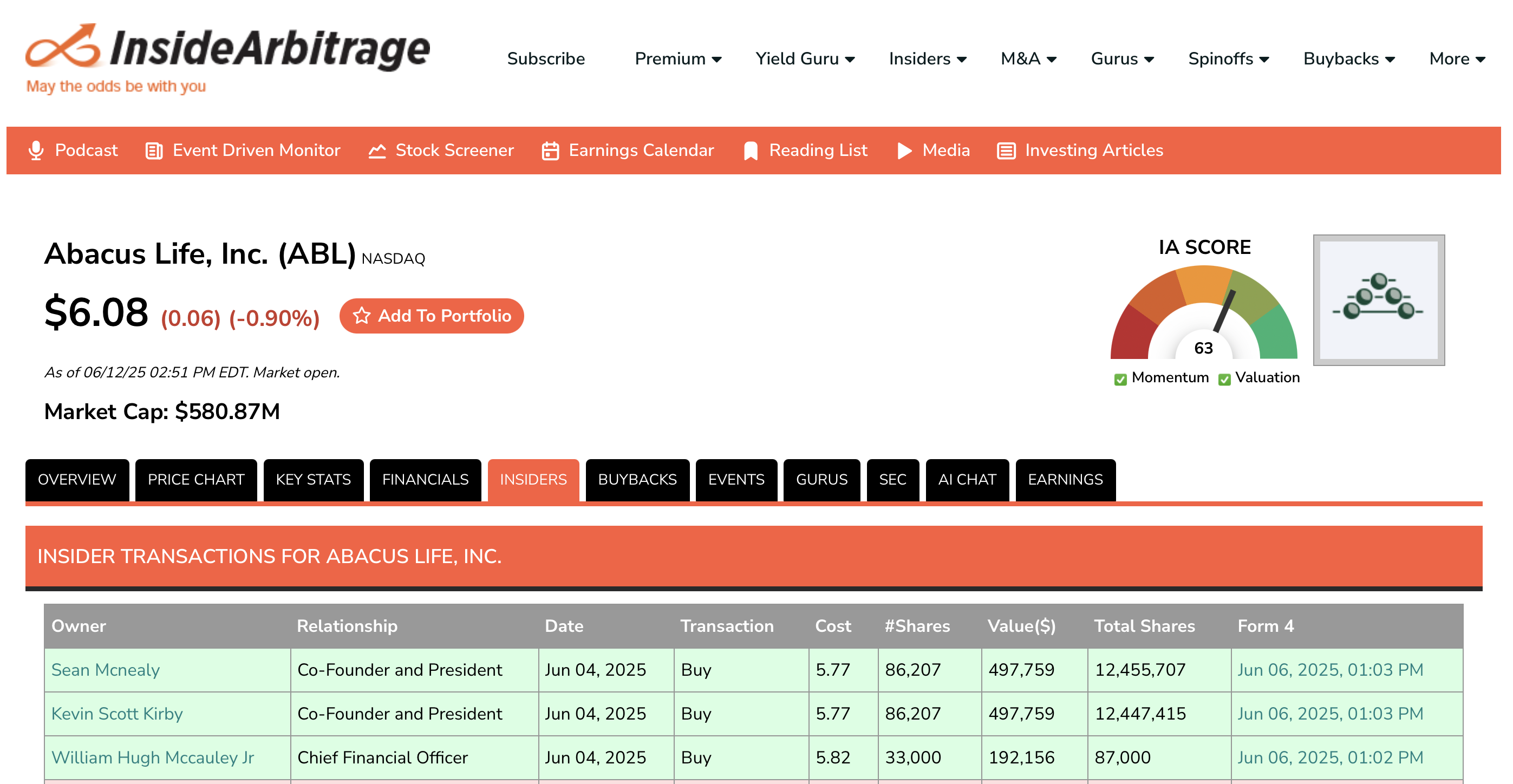

Abacus Life Inc (ABL): $5.84

Abacus Life describes itself as an alternative asset manager and the company engages in providing a secondary market for life insurance policies. In other words, it provides payouts to consumers that want to cash out their policies. Imagine someone who purchased a 30 year life insurance policy at the age of 40, paid for the policy for 20 years and now at age 60, no longer has the same circumstances that caused them to purchase the policy. They could either stop paying for the policy and let it lapse, or sell it to someone like Abacus Life.

The part that is really interesting in this situation is that things can change a lot in 20 years. A young married man who had a steady job and healthy habits when he purchased a 40 year life insurance policy at the age of 30 could be living a very different life at the age of 50. If he suddenly picked up the habit of betting on horse races every weekend and is no longer able to hold down a job or run a business, the mortality risk profile has likely changed considerably from what the life insurance company had underwritten 20 years ago.

If Abacus Life’s underwriting policies are strong and nuanced, they could potentially arbitrage this opportunity.

There are multiple things going on with Abacus Life that would make me want to put this company on my watchlist for further research. Beyond the interesting business model and insider purchases by the CFO as well as the Co-founders of the company, the company also announced a small $20 million stock buyback last week that represented 3.58% of its market cap at announcement.

When I was looking into why company insiders were buying stock even as the company decided to buy back its own stock, I came across a short report by Morpheus Research that claims:

“This $740 million SPAC is yet another life settlements accounting scheme manufacturing fake revenue by systematically underestimating when people will die”

I have no familiarity with Morpheus Research or its claims, but the company responded briefly to the allegations in the short report through a press release claiming:

“Abacus has been buying and selling life insurance policies for over two decades with long-standing and trusted counter-party relationships. If Abacus used flawed data causing over-valuation of the underlying insurance product assets, the Company would be going out of business, not consistently producing positive realized returns. As highlighted in the first quarter 10-Q Abacus filed on May 8, 2025, Abacus realized gains of nearly 40% while deploying capital of 126 million. These realized gains were within a margin of error of 2% of the mark from the prior quarter.”

The fact that the company went public through a SPAC instead of a traditional IPO is a red flag in my book. I do not know whether Morpheus Research or Abacus Life is right but I find the whole situation fascinating and I would not have discovered it if it had not been for the insider purchases. While the treasure hunt part of reviewing insider transactions is well and good, it is also important to remember the dark side of this approach.

I wrote the following about the dark side of insider transactions in my book:

“Insiders are aware that market participants pay attention to insider transactions and sometimes you see insiders purchase stock just to signal the market. This is an example of George Soros’s theory of reflexivity in action.

In a few cases, the company may go so far as to issue a press release to draw attention to the insider transaction, which under normal circumstances should be a big red flag for you.”

Despite this drawback, fishing in this pond long enough helps you identify patterns that reduce the noise and improve the signal for idea generation.

Disclaimer: I have no positions in any of the stocks mentioned in this article. Please do your own due diligence before buying or selling any securities mentioned in this article. We do not warrant the completeness or accuracy of the content or data provided in this article.