Among global oil majors, BP (BP) stands out for the wrong reasons. Over the past decade, BP has delivered returns (not taking into account dividends) of just 7%, dramatically lagging peers that have compounded value through a very challenging macro environment for the oil & gas industry. This persistent underperformance is not the result of a single bad year or an isolated operational failure. It reflects years of strategic drift, repeated CEO turnover, and inconsistent capital allocation, all unfolding while competitors steadily improved margins and returns.

Now, BP finds itself at a potential inflection point. Activist pressure from Elliott Management, a new CEO mandate, and the potential of the oil & gas industry approaching a cyclical low have converged. At the same time, BP offers a dividend yield of 5.7%, providing tangible income while investors wait for change.

The core question this holiday season is whether Santa will deliver a lump of coal to BP investors or is the company going to deliver (black) gold? In other words, is BP finally positioned to close the profitability and valuation gap with peers, or is it destined to remain a value trap?

Key Insights

Company Profile

BP is a global integrated energy company with operations spanning oil & gas production, refining, trading, and fuel marketing. The business is organized into Gas & Low Carbon Energy, Oil Production & Operations, and Customers & Products, covering everything from natural gas and crude oil to fuels, lubricants, and energy trading. Alongside its core hydrocarbon operations, BP has been building exposure to renewables, including solar, wind, hydrogen, bioenergy, and EV charging. Founded in 1908, BP is headquartered in London and operates across markets worldwide.

Business Segments

BP operates through three core business segments:

Fourth CEO in the last Six Years

Over the past six years, BP has cycled through multiple CEOs and interim leadership arrangements, each ushering in a different strategic tone, capital allocation philosophy, and narrative for investors. The result has been a company in near-constant reset mode, never quite executing long enough on any single strategy to deliver sustained returns.

Bob Dudley: Stabilizer, Not a Builder (2010 – 2020)

Bob Dudley led BP through one of the most difficult chapters in its history following the Deepwater Horizon disaster. His tenure was defined by risk management, balance-sheet repair, and legal cleanup, rather than growth or bold reinvention. Dudley successfully stabilized BP, reduced liabilities, and restored operational credibility.

However, by the end of his tenure, BP was widely viewed as strategically cautious compared with peers. Dudley stepped down in early 2020 as part of a planned succession, with the board seeking a leader who could reposition BP for a decarbonizing world and re-energize the company’s long-term narrative. His exit was orderly but it also marked the end of a defensive era without having laid a clear foundation for the next phase.

Bernard Looney The Energy Transition Bet (2020 – 2023)

Bernard Looney took over in 2020 and pursued one of the most aggressive energy-transition strategies among global oil majors, repositioning BP as an “integrated energy company” through reduced hydrocarbon output targets and accelerated investment in renewables, EV charging, hydrogen, and bioenergy.

While initially welcomed by ESG-focused investors and policymakers, the strategy delivered weaker financial results. Returns from transition assets lagged, margins compressed, and BP fell further behind peers that prioritized capital discipline. Looney exited abruptly in 2023 following governance and disclosure issues related to personal conduct, leading BP to dismiss him without notice and he had to forfeit up to $40.6 million in potential compensation. His departure halted the transition strategy mid-execution and reinforced concerns around leadership stability, ushering in an interim period marked by defensive capital allocation and limited strategic clarity.

Murray Auchincloss (2024 – 2025) A Return to Financial Pragmatism Under Activist Scrutiny

The appointment of Murray Auchincloss in 2024 signaled a shift at BP plc away from narrative-led strategy toward financial discipline. A long-tenured BP executive with deep finance and operational experience, Auchincloss was charged with improving margins and free cash flow, tightening capital allocation and cost control, simplifying the portfolio, and restoring investor confidence. Under pressure from Elliott Management, BP reversed elements of the prior energy-transition strategy and refocused on core oil and gas operations.

The appointment of Murray Auchincloss in 2024 signaled a shift at BP plc away from narrative-led strategy toward financial discipline. A long-tenured BP executive with deep finance and operational experience, Auchincloss was charged with improving margins and free cash flow, tightening capital allocation and cost control, simplifying the portfolio, and restoring investor confidence. Under pressure from Elliott Management, BP reversed elements of the prior energy-transition strategy and refocused on core oil and gas operations.

Auchincloss’s tenure coincided with heightened activist scrutiny and a narrower tolerance for weak execution following the appointment of Albert Manifold as Chair, which triggered a strategic review and renewed engagement with major shareholders. However, his time in the role proved brief. He resigned with immediate effect, an exit not linked to a single operational setback but emblematic of a deeper challenge: BP’s issue had shifted from strategic direction to execution credibility. The abrupt departure reinforced investor frustration with continued leadership churn and underscored the market’s limited patience for further resets at the top.

Elliott’s Activism

Activist hedge fund Elliott Management emerged as a significant shareholder in BP plc in early 2025, building a stake of just over 5%, making it one of the company’s largest investors alongside BlackRock and Vanguard.

Elliott’s involvement intensified pressure on BP’s board and management to address what it views as chronic underperformance, strategic drift, and weak capital discipline relative to oil major peers. Rather than a narrow operational critique, Elliott’s demands have targeted BP’s capital allocation framework, cost structure, and portfolio focus.

1. Sharpen Capital Allocation and Boost Free Cash Flow

Elliott has urged BP to materially increase its free cash flow, with one reported target of $20 billion annually by 2027, up roughly 40% from the company’s prior outlook. Achieving this would require significant spending reductions and tighter capital discipline.

2. Deeper Cost and Spending Cuts

The activist is pushing for annual CapEx reductions to around $12 billion (from a planned $13–$15 billion range). They are also asking for further cost savings, including potential incremental cuts beyond existing targets. These measures are intended to align BP’s cost base more closely with higher-return peers and improve margins.

3. Portfolio Simplification and Asset Divestments

Elliott has argued that BP’s portfolio remains burdened by non-core and lower-return assets, including parts of its renewables exposure, which dilute focus and capital efficiency. Under this pressure, BP agreed to sell a 65% controlling stake in its Castrol lubricants business to Stonepeak, valuing the unit at $10.1 billion. BP will retain a 35% minority stake, while Canada Pension Plan Investment Board will invest up to $1.05 billion for an indirect interest.

The transaction is expected to deliver about $6 billion in cash proceeds to BP and represents a material step in its broader $20 billion divestment program. Early discussions in November 2025 had implied valuations closer to $8 billion, but BP confirmed the $10 billion enterprise value for the deal even as we were writing this article.

4. Strategic and Governance Changes

Beyond financial targets, Elliott has advocated for broader structural changes, including discussion around management and board adjustments to accelerate execution and accountability. At least one report indicated its engagement with other major BP investors about potential board and management changes.

Who is Meg O’Neill?

It is against this backdrop of heightened activist scrutiny and a narrower tolerance for execution risk that BP moved to appoint Meg O’Neill, CEO of Woodside Energy and a former ExxonMobil executive, as Auchincloss’s successor, effective April 1, 2026. Carol Howle, BP’s head of trading, will serve as interim CEO. O’Neill will become BP’s fourth chief executive in just over six years, a period marked by an unsuccessful and value-destructive attempt to transform BP into a green energy champion.

It is against this backdrop of heightened activist scrutiny and a narrower tolerance for execution risk that BP moved to appoint Meg O’Neill, CEO of Woodside Energy and a former ExxonMobil executive, as Auchincloss’s successor, effective April 1, 2026. Carol Howle, BP’s head of trading, will serve as interim CEO. O’Neill will become BP’s fourth chief executive in just over six years, a period marked by an unsuccessful and value-destructive attempt to transform BP into a green energy champion.

O’Neill’s appointment was viewed positively by Elliott Management, which interpreted the move as evidence that BP is executing its turnaround plan under Manifold’s leadership. O’Neill will be the first external CEO in BP’s 116-year history. At Woodside, O’Neill oversaw the company’s expansion in the U.S., including the $1.2 billion acquisition of LNG developer Tellurian in 2024 and a $17.5 billion final investment decision on the Louisiana LNG project. She later secured funding support from private equity firm Stonepeak to help finance the Gulf Coast development.

O’Neill inherits a company with significant U.S. exposure. BP invested more than 40% of its $16.2 billion capital budget in the United States last year, and has ambitions to lift U.S. output to 1 million barrels of oil equivalent per day (boed) by the end of the decade, while keeping overall production broadly flat at around 2.4 million boed. Her challenge will be to translate scale and capital intensity into sustained margin improvement and shareholder returns under heightened investor scrutiny.

Industry Overview: Oil & Gas at a Cyclical Inflection – Why Timing Matters for BP

The global oil and gas industry is potentially approaching a cyclical inflection after more than a decade of underinvestment that followed the 2014–2016 downturn and the 2020 pandemic shock. Even as global oil demand reached record highs in 2024–2025, upstream capital spending has remained well below prior-cycle peaks, tightening spare capacity and increasing sensitivity to geopolitical disruptions. OPEC+ has reinforced this late-cycle setup by prioritizing price stability over volume growth, while demand from emerging markets, aviation, petrochemicals, and LNG has proven more resilient than many energy-transition forecasts anticipated.

Against this backdrop, the sector is re-centering on fundamentals. U.S. oil majors that emphasized capital discipline, balance-sheet strength, and shareholder returns have outperformed, while European peers, including BP, are retreating from lower-return green energy transition investments and refocusing on cash flow and capital efficiency. If the cycle turns, restrained investment could support tighter markets and stronger profitability. For BP, however, industry tailwinds alone will not be sufficient: any sustained upside depends on execution, margin repair, and disciplined capital allocation.

BP’s asset base remains globally competitive but lacks the scale advantage of its largest peers. The company reports approximately 6.25 billion barrels of oil equivalent in proven reserves and production of about 2.4 million boed, trailing Exxon Mobil, Chevron, and peers such as Shell and TotalEnergies. Larger, lower-cost reserve positions provide those companies with greater flexibility and cash-flow resilience across commodity cycles.

The implication is clear. BP’s valuation discount reflects execution risk rather than resource scarcity. Until margins, capital efficiency, and returns move meaningfully closer to peer levels, the stock is likely to remain structurally discounted – even in a supportive industry environment.

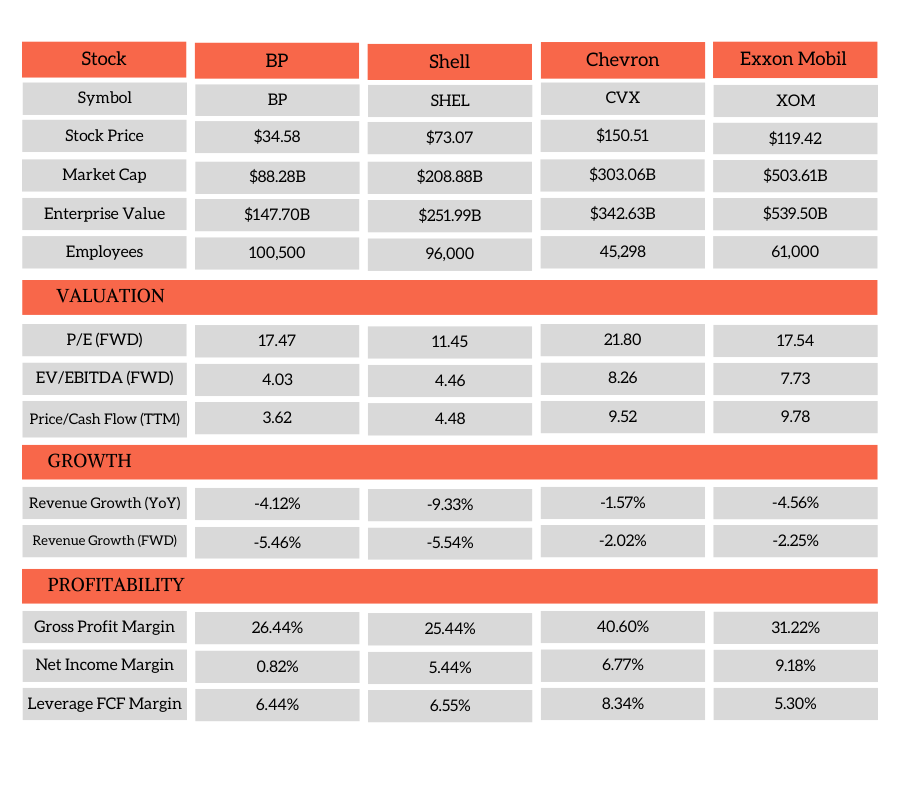

Peers

BP lags across key performance metrics relative to Shell (SHEL), Chevron (CVX), and Exxon Mobil (XOM), especially when it comes to profitability, as seen by its minuscule net income margin. While BP offers a compelling dividend yield and strong cash flow potential, its lower margins and weaker returns on capital illustrate why it trades at a discount to peers and remains out of alignment with top-tier energy majors.

BP’s Core Risks

What Needs to Change for BP

Valuation

Despite an attractive dividend yield of around 5.7%, BP continues to trade at valuation levels that reflect investor caution around profitability and execution. The shares trade at approximately 17.5 times forward earnings, a level that suggests limited confidence in earnings durability rather than a clear recovery premium. In contrast, BP’s EV/EBITDA multiple of about 4.0 times implies relative cheapness on an enterprise-value and cash-flow basis, highlighting a disconnect between headline earnings valuation and underlying cash-generation capacity.

Profitability remains the primary constraint. BP’s net margin of roughly 0.8% and operating margin of about 6%–7% lag those of major peers, pointing to weaker earnings conversion and subdued returns on capital. While the company continues to generate solid operating and free cash flow supporting dividends and balance-sheet repair, valuation support remains anchored to yield and cash flow until margins and returns show sustained improvement.

BP Third Quarter 2025 Results (Press Release) (Presentation)

Q4 2025 Outlook:

Bull Case

BP’s decade-long underperformance reflects mismanagement missteps rather than a lack of asset quality, creating scope for improvement. The appointment of a new external CEO, combined with Elliott Management’s activist pressure, raises accountability around capital discipline, cost control, and portfolio simplification. We are already starting to see this in play with the Castrol divestiture.

Even partial normalization of BP’s net margins toward peer levels (Shell, Chevron, Exxon) could drive outsized earnings leverage and a valuation re-rating. The 5.7% dividend yield provides income support while changes take time to play out. A potential cyclical upturn in the oil & gas industry could further amplify cash flow as execution improves. BP’s reserve base and production scale remain globally competitive, supporting turnaround optionality.

Bear Case

BP’s challenges may be structural rather than managerial, as repeated CEO changes have failed to deliver sustained margin or return improvement. Profitability and ROIC remain well below peers, and asset sales risk shrinking the earnings base without fixing execution issues. Activist involvement does not guarantee success, particularly in a complex, capital-intensive business. The high dividend yield may reflect investor skepticism and could come under pressure in a weaker oil price environment. A deeper analysis of BP’s proven reserves compared to peers is essential in determining if the core issues at BP are the quality of those reserves.

Conclusion

BP is best understood as a governance-driven turnaround, not a conventional oil-major investment. The company has the scale, reserve base, and cash-generation capacity to compete, but its long-term underperformance underscores that assets alone are insufficient. The combination of new leadership, board-level strategic review, and activist oversight creates a window for an execution-led turnaround that at any point in the past decade. Whether BP can use this window to restore credibility will determine if the valuation discount narrows or persists.

If BP manages to engineer a turnaround and that turnaround coincides with a cyclical rebound in the oil & gas industry, the stock might finally achieve escape velocity. Key milestones to watch include progress on cost reduction, asset divestments, debt trajectory, and early execution signals under the new CEO.

CEO

CFO

General Counsel/Chief Legal Officer

Others

Appointments

1. Fastenal Company (FAST): $41.83

On December 19, 2025, the Board appointed Jeffery M. Watts, Fastenal’s current President and Chief Sales Officer, as the next CEO of Fastenal, effective July 16, 2026.

| MarketCap: $48.02B | Avg. Daily Volume (30 days): 7,054,250 | Revenue (TTM): $8B |

| Net Income Margin (TTM): 15.34% | ROE (TTM): 32.74% | Net Debt: $229.20M |

| P/E: 39.46 | Forward P/E: 35.23 | EV/EBIDTA (TTM): 26.81 |

| P/S (TTM): 6.00 | P/B (TTM): 14.45 | 52 Week Range: $35.31 – $50.63 |

2. Marathon Petroleum Corp (MPC): $165.73

On December 18, 2025, Marathon Petroleum Corporation announced the appointment of Maria A. Khoury to serve as Chief Financial Officer effective January 19, 2026.

| MarketCap: $49.82B | Avg. Daily Volume (30 days): 2,047,341 | Revenue (TTM): $133.58B |

| Net Income Margin (TTM): 2.16% | ROE (TTM): 18.89% | Net Debt: $31.5B |

| P/E: 17.65 | Forward P/E: 10.46 | EV/EBIDTA (TTM): 7.98 |

| P/S (TTM): 0.37 | P/B (TTM): 3.43 | 52 Week Range: $115.10 – $202.30 |

3. BP p.l.c. (BP): $34.58

On December 17, 2025, BP p.l.c. announced that the bp Board has appointed Meg O’Neill as bp’s next chief executive officer, effective April 1, 2026.

| MarketCap: $88.28B | Avg. Daily Volume (30 days): 7,010,959 | Revenue (TTM): $185.93B |

| Net Income Margin (TTM): 0.82% | ROE (TTM): 3.55% | Net Debt: $39.77B |

| P/E: 56.25 | Forward P/E: 12.69 | EV/EBIDTA (TTM): 4.47 |

| P/S (TTM): 0.47 | P/B (TTM): 1.33 | 52 Week Range: $25.22 – $37.64 |

4. Kraft Heinz Company (KHC): $24.02

On December 16, 2025, Kraft Heinz Company announced that it has appointed Steve Cahillane as Chief Executive Officer, effective January 1, 2026.

| MarketCap: $28.43B | Avg. Daily Volume (30 days): 15,273,850 | Revenue (TTM): $25.16B |

| Net Income Margin (TTM): -17.35% | ROE (TTM): -9.69% | Net Debt: $18.06B |

| P/E: -6.47 | Forward P/E: 9.72 | EV/EBIDTA (TTM): -10.18 |

| P/S (TTM): 1.13 | P/B (TTM): 0.74 | 52 Week Range: $23.60 – $33.35 |

5. Lululemon Athletica (LULU): $210.4

On December 11, 2025, Lululemon’s board appointed Meghan Frank, CFO, and Andre Maestrini, President and Chief Commercial Officer, as Interim Co-CEOs, effective January 31, 2026.

| MarketCap: $24.68B | Avg. Daily Volume (30 days): 4,464,962 | Revenue (TTM): $11.07B |

| Net Income Margin (TTM): 15.72% | ROE (TTM): 41.02% | Net Debt: $726.93M |

| P/E: 14.63 | Forward P/E: 17.83 | EV/EBIDTA (TTM): 8.63 |

| P/S (TTM): 2.13 | P/B (TTM): 4.13 | 52 Week Range: $159.25 – $423.32 |

Departures

1. Fastenal Company (FAST): $41.83

On December 19, 2025, Daniel L. Florness, Chief Executive Officer and director of Fastenal Company, notified the Board of his decision to step down as CEO and resign from the Board effective July 16, 2026.

| MarketCap: $48.02B | Avg. Daily Volume (30 days): | Revenue (TTM): $8B |

| Net Income Margin (TTM): 15.34% | ROE (TTM): 32.74% | Net Debt: $229.20M |

| P/E: 39.46 | Forward P/E: 35.23 | EV/EBIDTA (TTM): 26.81 |

| P/S (TTM): 6.00 | P/B (TTM): 14.45 | 52 Week Range: $35.31 – $50.63 |

2. Marathon Petroleum Corp (MPC): $165.73

On December 18, 2025, Marathon Petroleum Corporation announced Khoury will succeed John J. Quaid, who will cease to serve as Executive Vice President and Chief Financial Officer of the Company effective January 19, 2026.

| MarketCap: $49.82B | Avg. Daily Volume (30 days): 2,047,341 | Revenue (TTM): $133.58B |

| Net Income Margin (TTM): 2.16% | ROE (TTM): 18.89% | Net Debt: $31.5B |

| P/E: 17.65 | Forward P/E: 10.46 | EV/EBIDTA (TTM): 7.98 |

| P/S (TTM): 0.37 | P/B (TTM): 3.43 | 52 Week Range: $115.10 – $202.30 |

3. BP p.l.c. (BP): $34.58

On December 17, 2025, BP p.l.c. announces that Murray Auchincloss has decided to step down from his position as CEO and director of the Board, effective 18 December.

| MarketCap: $88.28B | Avg. Daily Volume (30 days): 7,010,959 | Revenue (TTM): $185.93B |

| Net Income Margin (TTM): 0.82% | ROE (TTM): 3.55% | Net Debt: $39.77B |

| P/E: 56.25 | Forward P/E: 12.69 | EV/EBIDTA (TTM): 4.47 |

| P/S (TTM): 0.47 | P/B (TTM): 1.33 | 52 Week Range: $25.22 – $37.64 |

4. Kraft Heinz Company (KHC): $24.02

On December 16, 2025, Kraft Heinz Company announced that current CEO Carlos Abrams-Rivera will step down on January 1, 2026, and will remain with the company as an advisor through March 6, 2026.

| MarketCap: $28.43B | Avg. Daily Volume (30 days): 15,273,850 | Revenue (TTM): $25.16B |

| Net Income Margin (TTM): -17.35% | ROE (TTM): -9.69% | Net Debt: $18.06B |

| P/E: -6.47 | Forward P/E: 9.72 | EV/EBIDTA (TTM): -10.18 |

| P/S (TTM): 1.13 | P/B (TTM): 0.74 | 52 Week Range: $23.60 – $33.35 |

5. Lululemon Athletica (LULU): $210.4

On December 11, 2025, the board of directors of Lululemon and Calvin McDonald mutually agreed that McDonald will step down from his position as Chief Executive Officer, effective January 31, 2026.

| MarketCap: $24.68B | Avg. Daily Volume (30 days): 4,464,962 | Revenue (TTM): $11.07B |

| Net Income Margin (TTM): 15.72% | ROE (TTM): 41.02% | Net Debt: $726.93M |

| P/E: 14.63 | Forward P/E: 17.83 | EV/EBIDTA (TTM): 8.63 |

| P/S (TTM): 2.13 | P/B (TTM): 4.13 | 52 Week Range: $159.25 – $423.32 |

If you are reading this article and have not signed up to receive such articles by email, please sign up either for our free, IA Plus or IA Premium service here. If you are an existing subscriber, you can login to the InsideArbitrage.com website to adjust the kinds of articles you receive by email by turning on or off specific categories of articles.

Disclaimer: Please do your own due diligence before buying or selling any securities mentioned in this article. We do not warrant the completeness or accuracy of the content or data provided in this article.