I had lunch with a couple of investor friends this week, and one of them was discussing his experience taking Waymos while we ordered food in a restaurant by scanning a QR code with minimal interaction with staff. In an age of AI that requires a wholesale reimagining of what labor will look like in the future, the need for career-focused education is back in the spotlight. For-profit education companies have long promised to bridge that gap – offering adults and students a path to employment through skill-based training. But behind this mission lies a troubled history.

The Obama administration launched a sweeping crackdown on the sector in 2011, citing widespread fraud, inflated job placement claims, and crippling student debt. Major players like Corinthian Colleges and ITT Technical Institute collapsed under regulatory pressure. Apollo Education (the parent of University of Phoenix) was consumed by the PE firm Apollo Global Management (APO) and I remember participating in the wide arbitrage spread that merger presented nearly nine years ago.

DeVry University, once a key player in this industry, didn’t escape scrutiny. It faced major lawsuits and settlements, including a $100 million FTC settlement for misleading advertising. But unlike its peers, DeVry didn’t fold. It pivoted.

Rebranding as Adtalem Global Education in 2017, the company sold off its university brand and turned its focus toward healthcare education. Today, Adtalem is back in the headlines. This time, not for controversy, but on account of a huge share repurchase announcement. Given its rocky past and strategic overhaul, it’s worth taking a closer look at how this company has evolved and what its future holds.

Adtalem Global Education Inc. (ATGE): $103.62

Market Cap: $3.73B

Enterprise Value: $4.24B

Key Insights

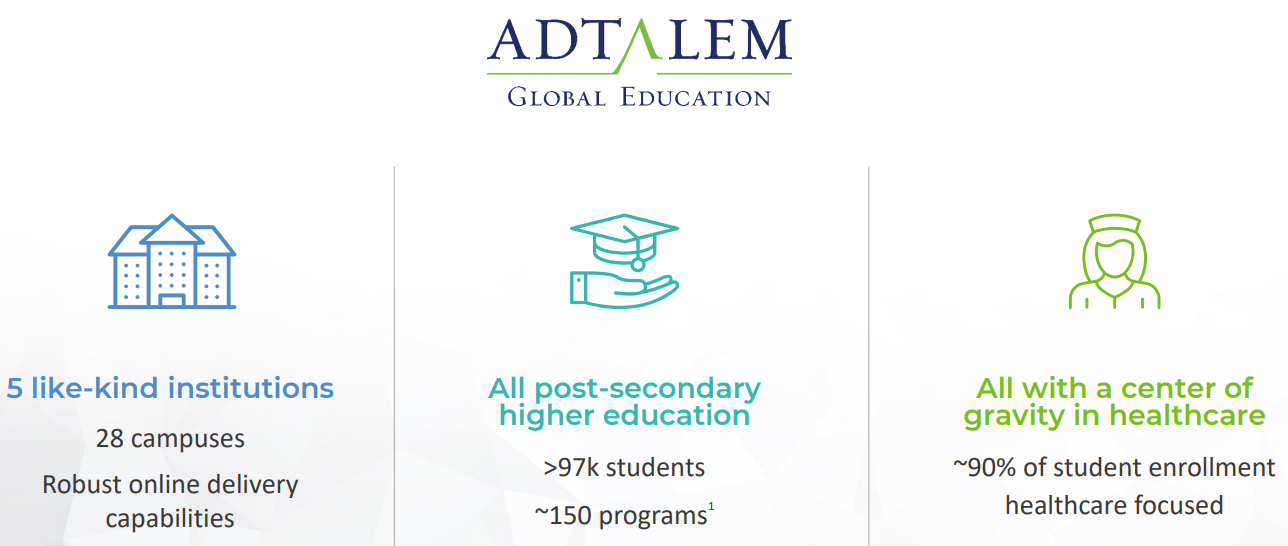

Adtalem Global Education (ATGE) is a healthcare education provider focused on addressing the growing shortage of medical professionals in the U.S. The company has strategically exited non-core businesses, including DeVry University, to concentrate on high-demand fields such as nursing, medicine, public health, and psychology.

Through its five institutions: Chamberlain University, Walden University, Ross University Schools of Medicine and Veterinary Medicine (RUSM & RUSVM), and American University of the Caribbean (AUC), Adtalem serves over 90,000 students via both physical campuses and online platforms, expanding access and geographic reach.

Segments Overview

Adtalem Global Education reports results across three key segments, each showing strong momentum in FY25:

Chamberlain and Walden University were recognized as “Opportunity Colleges and Universities” in the 2025 Student Access and Earnings Classification by the Carnegie Foundation and American Council on Education.

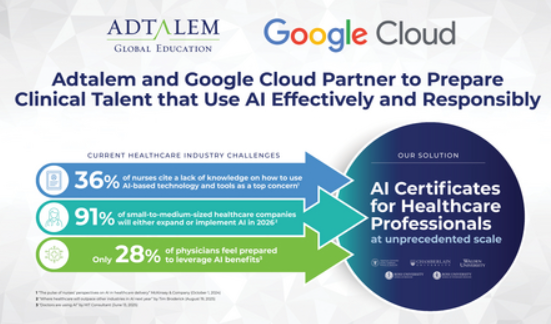

Adtalem is accelerating its use of AI through a partnership with Google Cloud to co‑develop a comprehensive AI credentials program, designed specifically for healthcare students and practicing clinicians. It is deploying AI‑powered learning tools that deliver real‑time tutoring, adaptive study plans, and personalized feedback, helping students master complex clinical concepts and skills. The goal is to ensure graduates are not only academically prepared but practice‑ready from day one as they enter hospitals, clinics, and other healthcare settings.

Strong Execution of Growth with Purpose Strategy

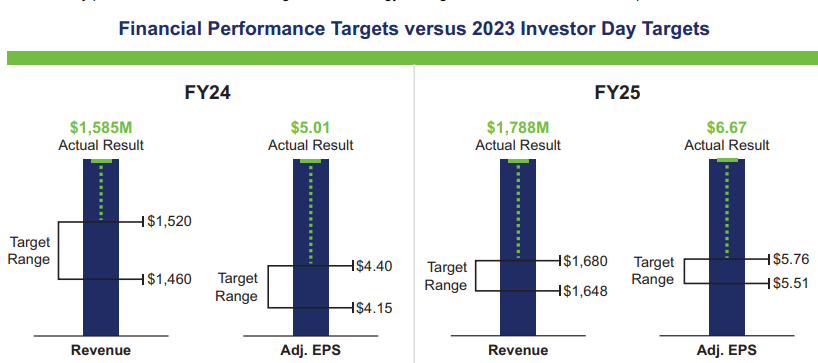

Adtalem has effectively executed its three-year “Growth with Purpose” strategy, with FY25 results underscoring this success. As mentioned earlier, the company saw robust enrollment growth across all three segments, averaging over 10% quarterly. Revenue climbed 12.9% to $1.79 billion, more than double the company’s 2023 investor day growth targets. Adtalem also graduated over 29,000 students in FY25. This strong performance validates the company’s model of delivering accessible, career-focused healthcare education through modern, tech-enabled platforms.

Source: Adtalem (Annual Report)

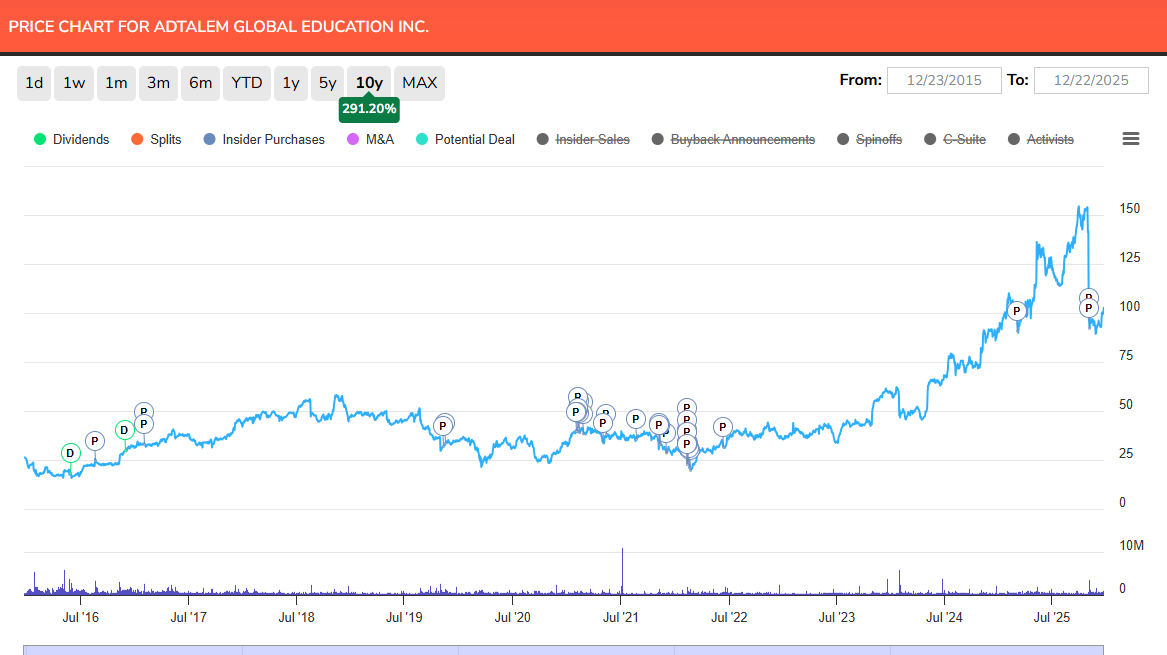

Building on its strong operational performance, Adtalem’s stock has surged up to 200% in the past five years, more than doubling the S&P 500’s 84% gain over the same period.

Financial Performance

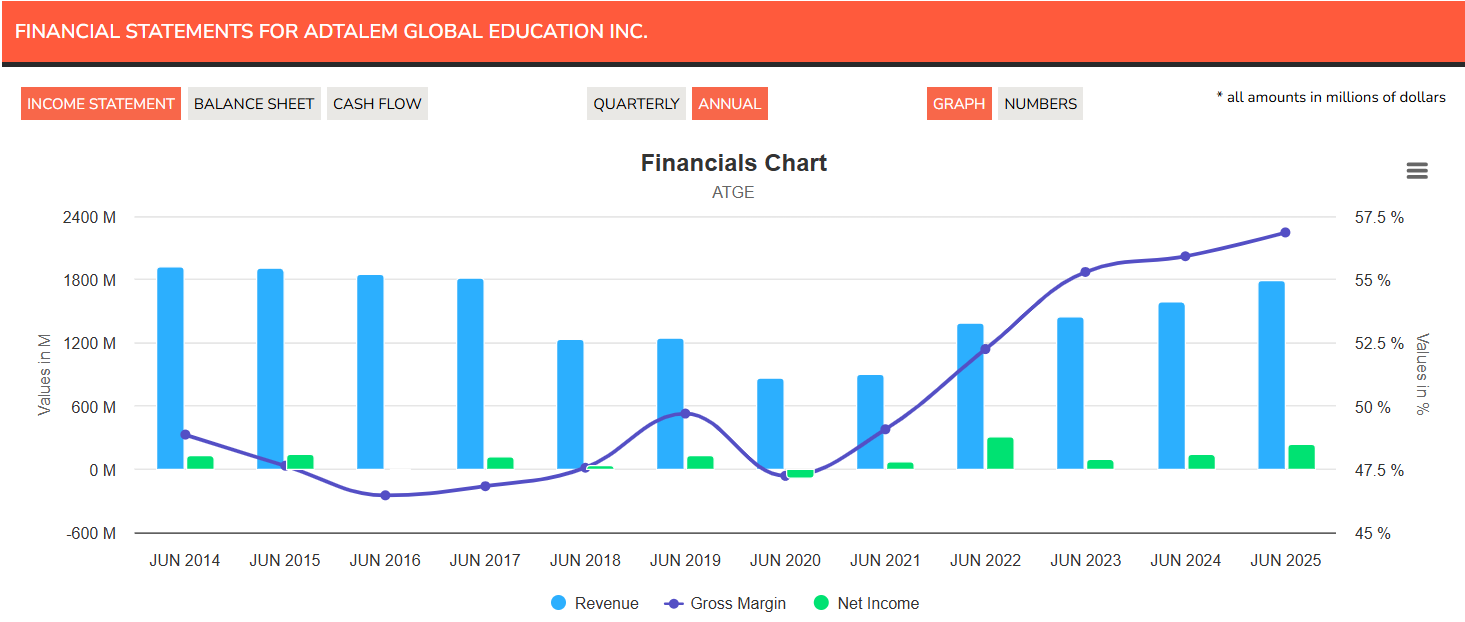

Adtalem has shown consistent financial strength, nearly doubling revenue from $866 million in FY20 to $1.78 billion in FY25, driven by sustained student enrollment growth across all segments. Margins have improved as well over these years, with gross margin increasing from around 47% to 57%. Earnings increased as well, with adjusted EPS increasing by 33.1% to $6.67, well above the 10–15% target range. Free cash flow is also strong, exceeding earnings in most quarters.

Source: InsideArbitrage

On the balance sheet front, the company improved its financial position by periodically paying down debt. It has reduced its debt by $1.1 billion since the Walden acquisition, bringing net debt down to $508.4 million as of the end of FY2025. Regulatory standing improved as well, with Title IV letters of credit reduced from 20% to 10% of receipts – a shift that signifies a heightened “financial responsibility” rating from the Department of Education, which doubles the company’s available cash by freeing up capital that was previously held as collateral.

Valuation

Despite its strong growth and expanding margins, Adtalem’s stock remains attractively valued, trading at 12.2x forward P/E and 12.86x EV/FCF. These modest multiples suggest that the market is either taking a cautious stance on its earnings quality or has yet to fully price in the company’s recent acceleration in profitability. In that context, management’s decision to authorize a buyback appears well-timed, reflecting their view that the stock remains undervalued.

Insider Activity

Insider purchases at Adtalem have occurred selectively rather than consistently over time. Notable buying activity was seen during 2016–2017, followed by a more concentrated wave in 2021–2022 when multiple insiders bought shares in the $25–$40 range – periods that aligned with attractive valuation levels.

Recently, in 2025, a few directors resumed buying, with well-timed purchases in November following a 31% stock drop post-earnings, signaling confidence in the company’s long-term fundamentals despite short-term market pessimism.

Source: InsideArbitrage

Peer Comparison

Adtalem trades at a discount compared to most of its education peers, except a few like Lincoln Educational Services (LINC) and American Public Education (APEI), which trade at even lower valuations. As you can see from the table below, its revenue growth is solid – roughly in line with or slightly trailing that of peers like Lincoln, Universal Technical Institute (UTI), and Stride (LRN). On the profitability front, Adtalem ranks near the top with strong gross and net margins, placing it second among the group.

| Company | ATGE | UTI | LINC | LOPE | LRN | APEI | STRA |

|---|---|---|---|---|---|---|---|

| Valuation | |||||||

| P/E | 15.36 | 23.27 | 53.19 | 22.24 | 10.42 | 29.55 | 16.73 |

| Forward P/E | 12.2 | 34.67 | 41.53 | 21.55 | 9.20 | 36.03 | 12.95 |

| Profitability | |||||||

| Gross Margin | 57.11% | 56.38% | 60.26% | 53.02% | 39.20% | 54.22% | 47.95% |

| Net Margin | 13.79% | 7.54% | 2.86% | 19.38% | 12.76% | 4.87% | 9.08% |

| Performance | |||||||

| 1 Year | 13.79% | 3.42% | 54.20% | 1.66% | -37.71% | 81.76% | -15.42% |

| 3 Year | 178.59% | 317.30% | 341.48% | 58.28% | 109.98% | 202.60% | 2.72% |

| 5 Year | 196.49% | 309.50% | 234.83% | 76.03% | 189.44% | 9.63% | -17.59% |

Source: Author with data from Seeking Alpha

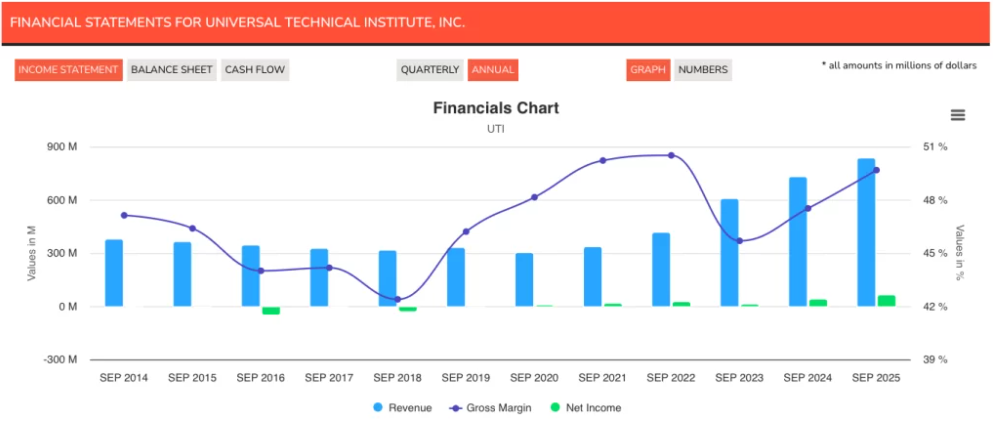

One of the most relevant peers to compare Adtalem with is UTI, especially given UTI’s increasing focus on healthcare education. We recently highlighted UTI in an Insider Weekends article after Christopher Shackelton, Co-Founder of Coliseum Capital and longtime UTI board member, purchased stock.

UTI acquired Concorde Career Colleges in FY2023, expanding into high-demand healthcare verticals such as nursing and dental/medical assistant training. The acquisition not only accelerated revenue growth but also improved profitability, as shown in the chart below.

For FY2026, UTI expects $905–$915 million in revenue (around 9% growth), but net income is projected to fall 33% to $40–$45 million. This led to a 26% drop in stock price, prompting insiders to step up and buy shares, just like we saw at Adtalem. While Adtalem is guiding to slightly lower revenue growth than UTI, it stands out with projected earnings growth of 14–18.5%, offering a stronger bottom-line trajectory. Moreover, UTI has a high valuation, trading at a forward P/E of 34.67, almost three times that of Adtalem.

Source: Insidearbitrage

Healthcare Shortage as a Tailwind for Adtalem

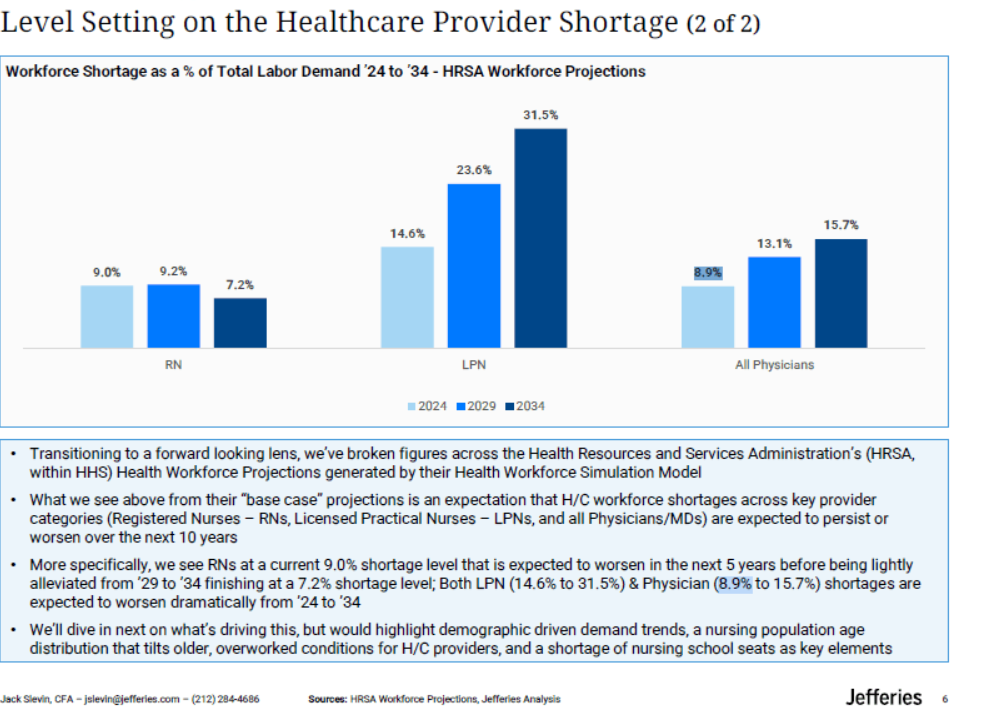

The U.S. healthcare sector is facing a severe labor shortage, with over 1.2 million registered nurses needed by 2030 to replace retirees and meet growing demand. Mental health professionals are also in short supply, and Jefferies estimates that across all major provider categories: Registered Nurses (RNs), Licensed Practical Nurses (LPNs), and Physicians, workforce shortages are expected to either persist or worsen through 2034 (as seen from the graph below).

Adtalem is structurally well-positioned to benefit from this demand. Its graduates directly feed into critical areas like nursing and medicine. Unlike elite institutions where medical tuition exceeds $95,000 per year, Adtalem’s universities offer a more accessible path at around $60,000 to $70,000.

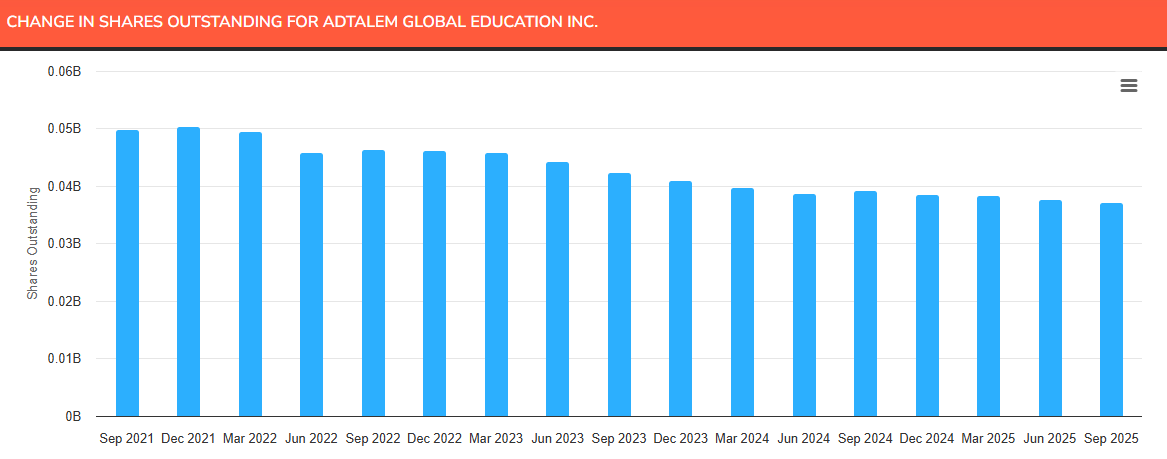

Adtalem has consistently prioritized share repurchases as a key method of returning capital to shareholders. Since its inception, the company has authorized nearly 15 buyback programs and has followed through on them with conviction. Between February 2022 and late 2025, Adtalem repurchased 17.2 million shares, about 30% of its shares outstanding, at an average price of $52.94, returning $913 million to shareholders. This substantial reduction in share count not only reflects disciplined capital allocation but also boosts per-share metrics for investors.

Source: Insidearbitrage

The trend has continued into FY2026 (fiscal year ends in June). In Q1 FY26, $8 million worth of shares were bought back, with $142 million remaining under the prior program as of October 2025. In November 2025, Adtalem decided to accelerate the final leg of its $150 million program, completing it in December with the repurchase of 1.6 million shares. At the same time, the Board approved a new $750 million repurchase authorization, equivalent to ~21% of its market cap at announcement, valid through December 2028.

While the company currently does not pay dividends, its strong free cash flow profile opens the door for dividends in the future. This deliberate and consistent approach to buybacks signals management’s confidence in the company’s intrinsic value and long-term growth trajectory.

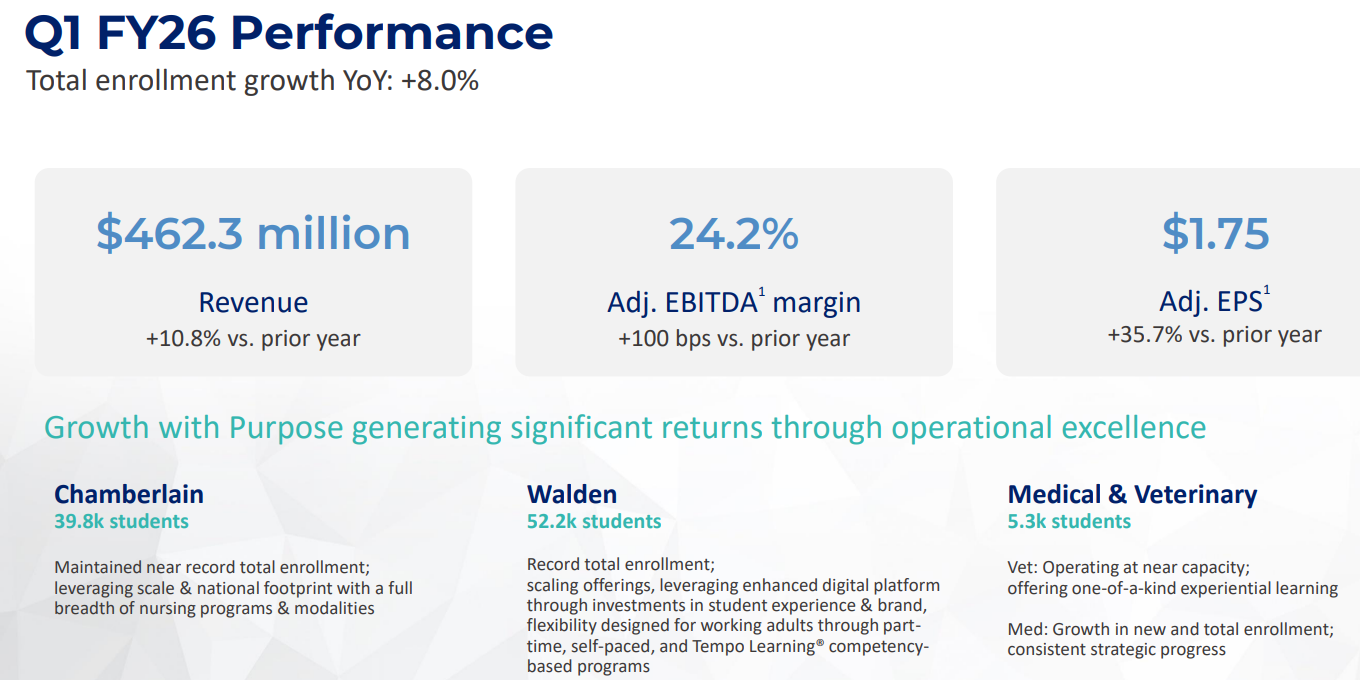

Strong Start to FY2026, But Market Reacts to Cautious Guidance

Adtalem delivered robust Q1 FY2026 results, continuing its multi-quarter streak of outperformance.

Source: Adtalem (Investor Presentation)

Despite the beat, Adtalem maintained its full-year FY2026 guidance of $1.90 to $1.94 billion in revenue and $7.60 to $7.90 in adjusted EPS, without an upward revision. Investors interpreted this conservatism as a sign of possible growth moderation ahead, especially since the guidance implies 6-8.5% revenue growth over the next year, which is much below FY2025’s revenue growth of nearly 13%. The market response was sharp, and shares fell nearly 31% on October 31.

Still, it’s worth noting Adtalem has been very consistent in surpassing top and bottom line estimates, having beaten both for 15 consecutive quarters. A more detailed strategic roadmap is expected at the company’s upcoming Investor Day on February 24, 2026.

Source: Adtalem (Investor Presentation)

Risks

Bottom Line

With labor markets tight and demand for skilled professionals rising, career-focused education, especially in healthcare, is seeing strong momentum. Adtalem is well-positioned to benefit, given its direct role in training nurses, physicians, and allied health professionals. Backed by strong margins, solid cash flow, and a shareholder-friendly capital return strategy, it stands out as a compelling long-term investment candidate tied to real-world workforce demand.

That said, my only concern is the company’s conservative full-year outlook. Projected revenue growth of 6–8.5%, while decent, is a slowdown from the prior year’s 11% growth and less compelling in the context of broader investor expectations. Additionally, four analysts have lowered their EPS estimates, and three have cut revenue projections over the past 90 days. I’ll be closely watching the February Investor Day for any signs of reacceleration or updated guidance.

Welcome to edition 108 of Buyback Wednesdays, a monthly series that tracks the top stock buyback announcements during the prior month. The companies in the list below are the ones that announced the most significant buybacks as a percentage of their market caps. They are not the largest buybacks in absolute dollar terms. A word of caution. Some of these companies could be low-volume small-cap or micro-cap stocks with a market cap below $2 billion.

As most companies reported their third-quarter earnings, the number of companies announcing share buybacks in November has gone up significantly to 143, compared to 86 in the previous month.

1. Infinity Natural Resources, Inc. (INR): $14.79

On November 10, 2025, the Board of Directors of this upstream energy company announced that it had approved a new $75 million stock repurchase agreement, equal to around 42% of its market cap at announcement.

| Market Cap: $889.42M | Avg. Daily Volume (30 days): 411,149 | Revenue (TTM): $308.48M |

| Net Income Margin (TTM): -0.58% | ROE (TTM): -0.94% | Net Debt: $71.98M |

| P/E: -16.79 | Forward P/E: 5.69 | EV/EBITDA (TTM): 4.46 |

2. Capri Holdings Limited (CPRI): $24.9

On November 4, 2025, the Board of Directors of this retailer announced that it had approved a new $1 billion stock repurchase agreement, equal to around 40.5% of its market cap at announcement.

| Market Cap: $3.01B | Avg. Daily Volume (30 days): 2,487,622 | Revenue (TTM): $4.37B |

| Net Income Margin (TTM): -29.63% | ROE (TTM): -347.96% | Net Debt: $2.93B |

| P/E: N/A | Forward P/E: 21.09 | EV/EBITDA (TTM): 25.76 |

3. ZOOZ Strategy Ltd. (ZOOZ): $0.43

On November 3, 2025, the Board of Directors of this electric vehicle charging company announced that it had approved a new $50 million share repurchase agreement. This represents around 34% of its market cap at announcement.

| Market Cap: $68.40M | Avg. Daily Volume (30 days): 1,091,255 | Revenue (TTM): $745.00K |

| Net Income Margin (TTM): N/A | ROE (TTM): -217.88% | Net Debt: $1.47M |

| P/E: N/A | Forward P/E: N/A | EV/EBITDA (TTM): -0.83 |

4. Amber International Holding Limited (AMBR): $1.81

On November 26, 2025, the Board of Directors of this real estate developer and investor authorized a new $50 million share repurchase program, equal to around 33.8% of its market cap at announcement.

| Market Cap: $165.82M | Avg. Daily Volume (30 days): 1,647,658 | Revenue (TTM): $5.04M |

| Net Income Margin (TTM): -296.23% | ROE (TTM): N/A | Net Cash: $39.92M |

| P/E: N/A | Forward P/E: N/A | EV/EBITDA (TTM): -7.12 |

5. ON Semiconductor Corporation (ON): $55.69

On November 18, 2025, the Board of Directors of this semiconductor company authorized a new $6 billion share repurchase program, equal to around 31.5% of its market cap at announcement.

| Market Cap: $22.68B | Avg. Daily Volume (30 days): 9,460,601 | Revenue (TTM): $6.19B |

| Net Income Margin (TTM): 5.16% | ROE (TTM): 3.91% | Net Debt: $760.30M |

| P/E: 74.67 | Forward P/E: 22.34 | EV/EBITDA (TTM): 12.58 |

If you are reading this article and have not signed up to receive such articles by email, please sign up for our free, IA Plus or IA Premium service here. If you are an existing subscriber, you can login to the InsideArbitrage.com website to adjust the kinds of articles you receive by email by turning on or turning off specific categories of articles.

Disclaimer: Please do your own due diligence before buying or selling any securities mentioned in this article. We do not warrant the completeness or accuracy of the content or data provided in this article.